Technical Issues™

COMEX-edition

Last November, the CME shut down for ten hours and blamed a broken air conditioner:

An air conditioner. At a data center built with N+1 redundancy, triple backups, and enough failover architecture to survive a small meteor strike. Engineers called it impossible. HVAC technicians called it impossible. The internet called it ridiculous.

So this time, they dropped the excuse entirely. Just “technical issues”. No details. Clean. Vague. Professionally non-committal. You have to respect the evolution - they got roasted so hard for the cooling excuse that they upgraded to pure corporate haiku. Something happened. We are fixing it. Thank you for your patience.

Yesterday’s forecast for Aurora: 35°F (2°C), partly sunny. Opening the door remains an option to cool things down.

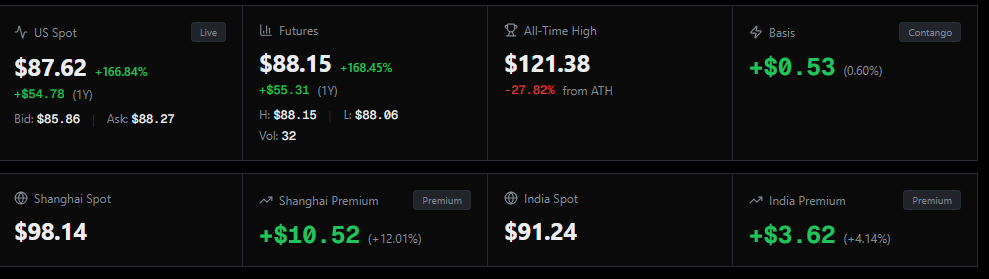

Silver opened at $89.4 yesterday and spent the entire morning doing what silver does when nobody’s actively sitting on it: going up. $89. $90. $91. Which is uncomfortably close to the level where the margin calls on short sellers stop being a nuisance and start being a near-death experience. The price where “bad quarter” becomes “I should call my lawyer”.

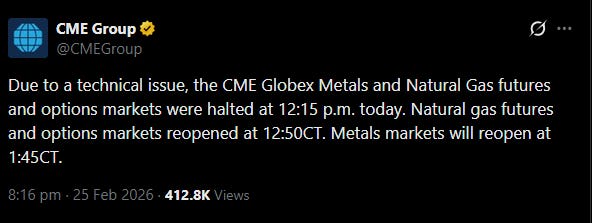

Guess what happened… The CME halted. Metals and natural gas? Gone. Existing orders - cancelled. Just wiped.

Equities? Fine. Bonds? Fine. FX? Fine. Just the exact markets experiencing the exact squeeze the exact people needed stopped. Coincidence, obviously. You’ve got to love that word… (COMEX FAQ link)

Shanghai kept trading. Dubai kept trading. London kept trading. The servers in Aurora, Illinois had issues. Everyone else’s servers were absolutely fine.

Funny thing though. When silver crashed 30% on January 30th - which I covered in “(Pet) rock, paper, scissors” - the circuit breakers didn’t trigger. No halts. No “technical issues”. The machine handled a 30% collapse in a single session without breaking a sweat. It’s apparently only upward price discovery that stresses the infrastructure.

Five years without a single outage. Then two in six months. Coinciding both times with silver squeezing toward levels that would cause serious institutional pain. You’d almost think there was a pattern.

Now, “halted” is such an interesting word. It implies nothing is happening. A pause. A quiet 90 minutes while the engineers figure out which wire came loose.

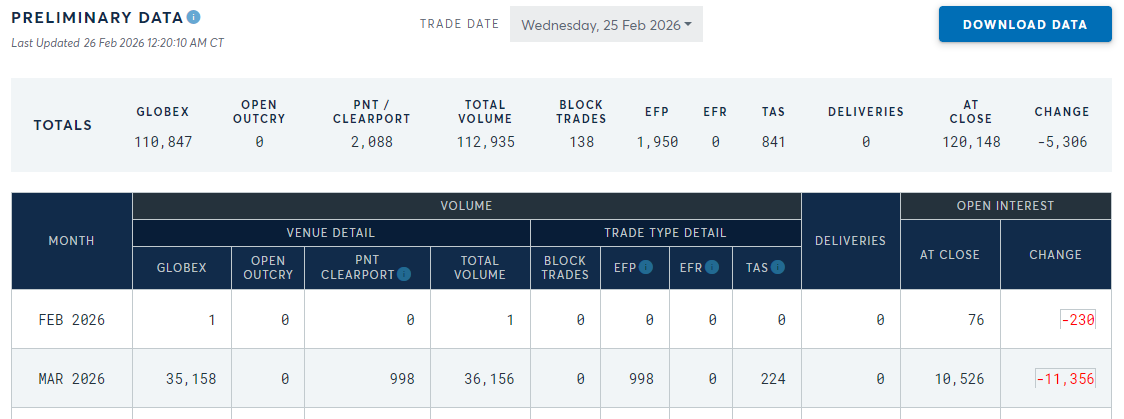

Except 31,828 contracts changed hands at exactly 12:45 PM. During the halt. One candle. $90.988. One hundred and fifty-nine million ounces of silver, in fifteen minutes, at a single price, traded on an exchange supposedly down by “technical issues”.

I genuinely sat with that number for a while. The market was closed. For everyone. Except for whoever printed 159 million ounces in a single tick while retail traders were staring at an error message (if you could read it that is).

When the market reopened, it came back $2 lower. The momentum was gone. Longs who’d been pressing through $91 had their day orders cancelled and had to re-enter manually. The banks’ limit orders - the big institutional GTC orders sitting below the market to absorb selling pressure - those stayed put. They never get cancelled. Different category.

So when trading resumed: retail, manually re-entering. Banks, already positioned. The chessboard got flipped and reset with one side’s pieces already back in place.

Technical issue.

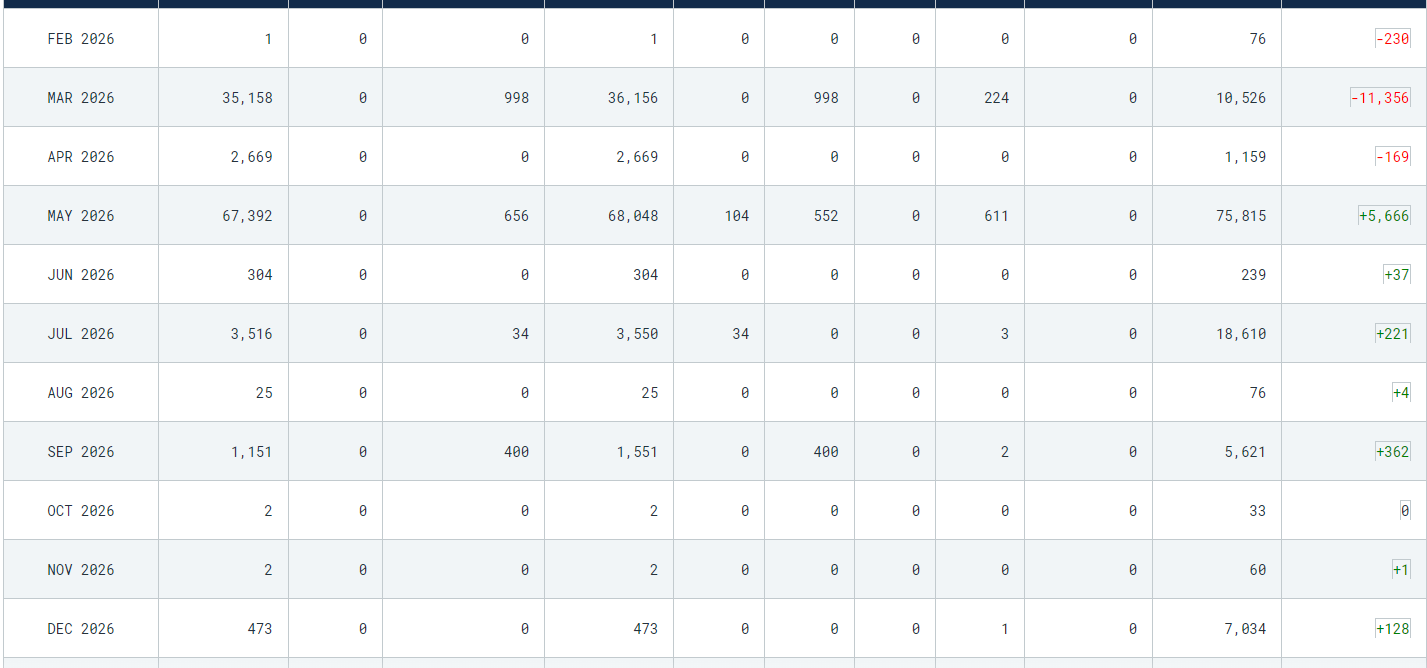

By end of day, March open interest had collapsed by 11,356 contracts in a single session. Cut in half. Which sounds like good news if you squint - pressure released, crisis averted, everyone goes home.

Except March is a delivery month. This isn’t a procedural detail - delivery months are when the rubber meets the road, when paper claims are supposed to convert into actual metal leaving actual vaults. At current open interest levels, March deliveries will come in lower than January’s. January was a non-delivery month.

This is not normal. Well, it has never been normal. But what this looks like is a lot of longs who were planning to stand for delivery suddenly decided - sometime during a 90-minute window when the exchange was technically dark but millions of ounces were changing hands - that rolling their contracts forward was actually a very attractive option. Handsomely attractive, one can imagine. People don’t abandon delivery positions in a physically tight market out of the goodness of their hearts.

Someone got paid to go away. The question is only how much.

Over half of those Wednesday contracts didn’t roll! They took cash and left. Full stop.

Normal roll behavior would see longs kick the can forward - take their position into the next delivery month, stay in the game. That’s not what happened. Traders cashed out and walked. Total open interest is collapsing, not rotating. The gamblers aren’t switching tables. They’re leaving the casino.

Which tells you something about what they think of the house.

The SIVL - silver implied volatility - spiked to 130 during the session and then “normalized” back to 90 by close. Still historically elevated. Options market makers pricing in “something insane could happen at any moment” because they read the tea leaves. When the session ended without a visible explosion, they walked the fear gauge back down. Slightly.

Until tomorrow. Rinse and repeat.

Now look, maybe I’m being uncharitable. Maybe the CME’s matching engine genuinely just fell over under the algorithmic pressure of a silver squeeze. Maybe those ounces really did trade themselves during a system failure with no human intervention. Maybe the fault hit specifically metals and gas and nothing else because that’s how distributed systems fail sometimes - very selectively, in the exact products under the most short-side stress, at the exact price level that triggers institutional margin calls.

Could happen.

Computers are weird.

Or - and I’m just spitballing here - when the machine starts losing, you break the machine. You cancel the attacking side’s orders. You give the defending side 90 minutes to breathe, make calls, secure margin, and print their exit trade on a dark venue. Then you reopen with the score reset and a $2 head start.

The CME will always hide behind “system architecture failure” because proving otherwise in court is nearly impossible. They know this. That’s the beauty of it. The outcome is identical to deliberate manipulation, but the defense is always “we had a bad server day”.

Meanwhile, across the world: the Shanghai Futures Exchange suspends accounts for fraudulent trading activity. The CFTC, which is supposed to be doing exactly this job for American markets, has been collecting their paychecks and hasn’t managed to find ANY reason to act. Not even one.

At some point the CFTC has to decide whether it’s a regulator or a spectator. The CME’s credibility is evaporating in real time - the comments under their announcement read like a public trial - and every halt, every cancelled order, every million-ounce candle printed during a “dark” session makes the next halt easier to call and harder to defend. Trust, once gone, does not come back.

This isn’t even unprecedented, just to really drive home how deep this tradition goes. The LBMA - London’s gold and silver market - had no trading for an hour on Oct 10 last year. Not a system outage. Not a technical issue. Just... no trading. The market was open. Participants were at their desks. And nothing happened for about 60 minutes while the price was under stress. No explanation was ever satisfying. The market just took a little break. Gathered its thoughts.

These things happen.

The real punchline is that the backroom deals apparently worked. March OI at the lowest since October 2023. Delivery pressure “resolved”. Crisis averted. For now.

Except the structural deficit didn’t close. Shanghai is still at a $10+ premium. What happened yesterday was a pressure release - not a fix. They let enough air out of the balloon that it won’t pop today.

I wrote about this in November. After that halt, silver went from $50 to $120 to $90. The “cooling issue” bought them three months then. This one will buy them what? A few weeks? The inventory math keeps getting worse month by month. The premium between Shanghai and New York gets wider every halt.

At some point, breaking the machine will actually break the machinations.

You can flip the chessboard all you want.

But players don’t have to stay in a rigged room.

Especially not when another table is available down the hall…

Just in: India's markets regulator SEBI quietly directed mutual funds to stop using LBMA prices for valuing physical gold and silver holdings, switching to domestic exchange prices from April 1st. One of the world's largest gold-consuming nations just decided London's price is no longer the relevant price.

Great article, as usual. You dig deep for data and information, which fuel important insights that one doesn’t find elsewhere. Thank you.

You know how there’s the National Debt Clock off of Times Square in NYC? It’s a Wonder of the [Un]Natural World. A “wonder” in the sense that it hasn’t exploded by now from its out of control acceleration, and buried the city underneath its particles.

Well, there should be a companion Precious Metals Markets Looting Clock that tracks the constantly escalating amount of plunder the corrupt, thieving, insider, non-prosecutable “bankers” have looted from the honest participants in the PM markets. In terms of velocity and acceleration, it would be right up there with the National Debt Clock.

Which should be re-named the National Looting Clock. Because the notion of debt implies the willingness, ability and intention of repayment. Absolutely none of that now applies to any federal, state, county or municipal debt. At this point, it is outright theft. Print and Steal. Nice work if you can get it, and the plundering issuers prove again and again that they can.

"You have to respect the evolution - they got roasted so hard for the cooling excuse that they upgraded to pure corporate haiku."

Nice one!