Nearly right

Annualisation anxiety: when an annual number apparently needs another twelve

The whole silver internet lost the plot this week, and I’ll be honest with you. I felt the pull. Every silverbug knows the little dopamine hit of a number that confirms the thing you already believed at breakfast.

I was starting to write the piece you’d expect me to write. Which went something like this:

It opens the way it always opens, with a crash.

Silver fell to $73.88 on Tuesday. A 4.6% gut-punch in a single session, the worst of it inside a five-minute window where the bid simply vanished. And if all you watched was the candle, you missed the whole story. The crash wasn't silver failing. Someone walked the price down to flush weak hands before the real move.

Look at what lit up the instant the price cracked. “Asian Guy” on YouTube has the lease rate at 8%. KingKong’s chart puts it at 6.8% annualised, thirteen times normal, the cost to borrow physical metal gone vertical. You pay 6.8% to borrow when the shelves are bare. London is bone dry and the lease rate is screaming it.

And while New York paper got hammered to $73, Shanghai closed the same session north of $85. A twelve-dollar gap. Sixteen percent. The East paying up for the exact ounce the West is dumping.

And then there is the customs data: 600 tonnes into Britain from America in March, straight back out to Hong Kong and India. Western vaults emptied into Chinese hands, through London, in broad daylight. The paper crash is but the cover story. The physical drain is the real transaction.

Sixth straight year of deficit. Lease rates vertical. Shanghai at a record premium. Vaults going out the door by the tonne. This is not a drill. This is the resumption of the squeeze that left stackers hanging end of last year.

But something irked me. I still don’t know what. Call it a gut feeling of watching way too many graphs. So I dug in…

Watch out. Here be dragons. The next few paragraphs are technical and use the words “annualised” and “convention” more than is strictly polite. If you don’t care how the sausage is made and you just want to know whether the world is ending, skip to the next section break. [But short version? It isn’t. Not today at least.]

First we have the long term Bloomberg lease rate (per KarelMercx):

And if you’ve been following me, you should recognise this genuine shortsqueeze:

Nope. I’m not obsessed.

Then we have the shorter term lease rates (again per KarelMercx):

And we have much-much-much-much more data from KarelMercx:

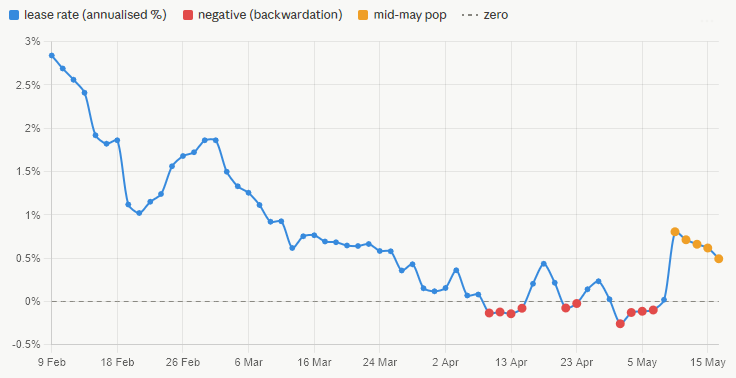

All fine and good, but if you’re like me and want a visual clue:

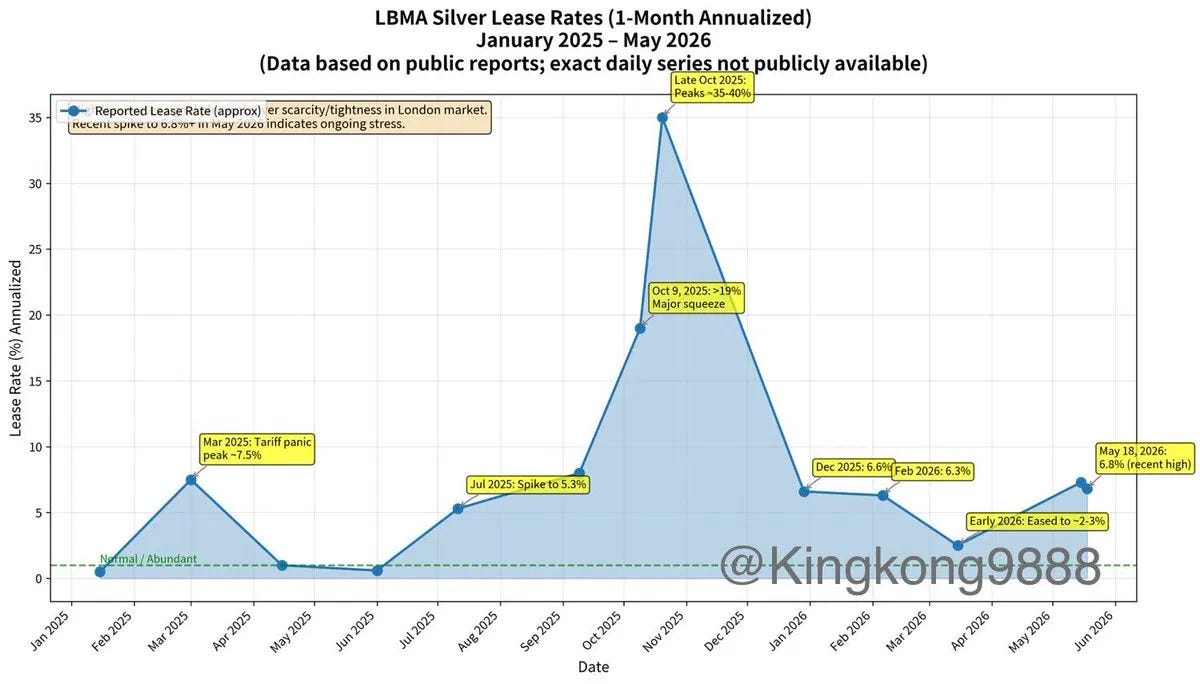

So what I did. I went back to last October, the real squeeze, the one nobody disputes, to use as a yardstick.

And all that panic, once you open the hood, comes down to this: It’s not even that the Silver Twitter crowd is watching the wrong gauge. The gauge is fine. They’re just reading it wrong, by a factor of twelve.

A lease rate is the cost to borrow physical metal, and like every interest rate on earth it’s quoted annualised. As in “per year”. The one-month silver lease rate is a one-month tenor expressed as an annual percentage. That’s the convention. It comes out of the oven already cooked.

So when the Bloomberg series reads 0.5%, that’s 0.5% a year. When it read 35% last October, that was 35% a year, which is exactly what every desk on the planet reported during the squeeze, because 35 was the annual number.

Now take Kingkong9888’s lease rate (May 18: 6.8%) versus KarelMercx’s 0.494. If you multiply KM’s by twelve, you get 5.93. Which is close to his 6.8…

Also read the caveat “Reported Lease Rate (approx)”.

Don’t take my word for it, check it against October, it’s the cleanest test there is. Everyone agrees the squeeze peaked around 35. If that 35 still needed annualising, the real annual rate would have been 35 times twelve. Four hundred and twenty percent. Which would’ve been memorable for reasons beyond securities lending. The 35 was already the annual figure. Which means the 0.5 sitting on the very same chart today should be too. Same column, same units, top to bottom.

Very likely what happened here is that people saw the 0.5 monthly lease rate, and thought it was monthly, so multiply it and *poof*, you get suddenly a scary number.

Anyway.

The honest version is quieter, and a lot more interesting. The rate did move.

Through April the rate was pinned at zero, mostly negative, minus a quarter point on the 30th, which is backwardation (the lender paying to lend). Quite normal actually.

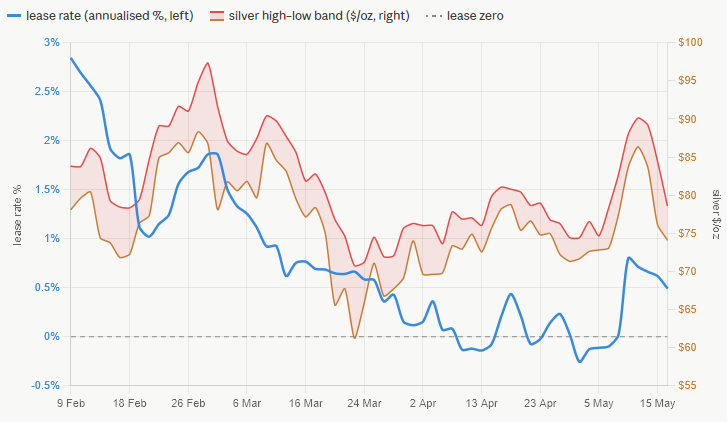

Then silver ran 6% on the 11th on the tariff-truce headlines, $80 to $87 by midweek, and the borrow cost popped along with it to 0.80. Bars wanted, shorts scrambling, arbitrage to the East lighting up. Standard stuff, you know?

Then it gave it all back, and out the other side. $73 by Tuesday, below where the pop even started.

One of the YouTube videos I saw had a culprit ready: the 30-year Treasury yield. ((insert triumphant trumpet sound)) It hit 5.19%, an 18y high.

Neat.

Except a yield that’s grinding higher over weeks doesn’t really crater anything inside a five-minute window. It’s a tide, not a wave.

The wave to me was an ordinary risk-off day with everything red at once.

Korea’s entire stock market, having narrowed itself to two AI stocks and a heroic quantity of margin debt, is now falling over with the sort of dignity usually associated with shopping carts as foreigners stampede for the exits, the Trump-Xi summit underwhelms, CPI runs hot, and a 75% rally suddenly remembers it was built on leverage and instant noodles.

Don’t misunderstand me, the yield thing is real (and I’m not talking about the US yield here alone). It’s a slow weight under the whole market. I just find it hard to believe that it pulled this particular trigger.

So back to the lease rate: it jumped from below 0% to nearly 1% in under a week. An unprecedented move, that’s for sure (just not 7%). Right now it’s easing back downwards, though still slightly elevated.

That’s actually the part that I want to draw your attention to. The price round-tripped and then some, it’s lower now than before the pop. But the borrow cost didn’t. It reset half a point above the negative floor it climbed off. Price net down, borrow cost net up.

The tightness outlasted the spike.

It’s still drifting lower, smooth, every session, 0.80 to 0.49 in four days. Could be it simply hasn’t finished retracing and floors back at zero next week, in which case it was a lagging echo and I’ve made too much of it. The tell is where it lands. Holds near 0.5 with the price in the 70s, something’s keeping a bid under the borrow cost. As of now it sits above its floor while the price sits below its floor, and that asymmetry is the only honest tightness signal in the mess. A tenth the size of the one going viral.

And whilst everyone is watching the lease rates, the actual story is weighed in tonnes. And it’s quietly disappearing.

COMEX silver inventories are down roughly 30% on the year. Sixteen and a half thousand tonnes last autumn, under ten now. Registered, the stuff that’s actually pledged for delivery, scraped down to 2,517 tonnes, about 81 million ounces, which keeps the coverage ratio under the 15% line it has been below for seven straight months.

I love a good murder mystery. Where did the metal go to?

Next up: UK

Follow it. In March (the latest data I could find because - as pmbug says - the LBMA is run by dinosaurs) the UK imported 601 tonnes of silver from the US, two-thirds of everything it brought in. And then London shipped 473 tonnes to Hong Kong and 89 to India, three-quarters of everything it sent out.

US → London → Shanghai’s front door, with a layover in a Heathrow bonded warehouse. London reads like the destination on the label, but it’s really just the hallway the metal walks down on its way East.

Take India. The same March data put 89 tonnes on its doorstep, and India spent this week trying to slam that door shut. Imports reclassified from free to restricted on Saturday, a licence now required on more than ninety percent of them, the second tightening in a fortnight, and all that to keep its own citizens from swapping a record-low rupee for metal.

A record twelve billion dollars of silver went in last year, two and a half times the year before, almost none of it for industry.

But restricting Asians from getting their precious metals fix is less a policy than a challenge issued directly to several thousand years of cultural habit.

Case in point: Thumbnail Green commented a few days ago about a queue forming outside a Melbourne bullion dealer. No1 needs to guess their nationality.

And on Friday, the metal gets a new place in the east to go.

Abaxx Exchange in Singapore opens a physically-deliverable silver futures contract. Thousand ounces, 99.99% fine, real bars only, settled into Singapore vaults.

A purpose-built venue for physical silver, in the precise corner of the world the physical silver has spent the entire year travelling toward.

They’ll start trading on the Toronto exchange the day before, then flip the switch on the metal Friday.

It won’t dethrone anything. It’ll clear a handful of lots and the volume will look like a typo next to New York. The difference is Singapore's contract settles in metal that physically exists. Call it a niche requirement.

All of this is why the lease rate stays relatively calm while the vault empties. A scramble spikes the borrowing cost. Like in October, everyone was reaching for the same bar in the same second, rate to 35.

But a migration doesn’t.

London still has plenty of float to lend at half a percent while it quietly loads the back of the warehouse, forklift by forklift, onto eastbound freight.

Nobody’s panicking (yet). They’re just leaving…

Calm is exactly what an orderly drain looks like from the lending desk.

That’s the whimper I keep writing about. Not a bang. Not a 6.8% klaxon. Just customs forms.

For now it’s slow and steady and it does not show up in the lease rate, which is the entire thing the 8%-on-YouTube crowd is missing while they stare at a figure they multiplied by twelve.

It’ll wake up eventually.

Push the price high enough and the shorts who sold paper they can’t cover have to go find real metal to deliver.

June’s first notice lands at the end of the month, and then we might get a scramble - unless they force to cover again, and the borrow cost goes vertical.

That’s the spike I’ll be watching for.

It just hasn’t come yet.

Earlier on this thread:

Won’t the comex just force cash closeout of the contracts it can’t settle? Isn’t that what happened in the January crash?

Kilo bar 2 streets away at current rate for sale cash. You may have tipped me over and into underhanded dealings No1