Sidelined

The repricing No1's reporting on

People keep asking me when a real repricing of gold and silver is going to happen. And more importantly… what will it look like?

They want a $300 print - preferably by tomorrow, a margin call cascade, a CNBC chyron in red 72-point font, a screen-printing-error moment…

And I keep telling them: ain’t gonna happen! TPTB won’t let it…

COMEX and LBMA won’t go out with a bang, but with a whimper. The whimper will sound like export data and customs forms being pushed around - digitally of course.

Yawn.

But that’s EXACTLY the point.

The repricing I’m envisioning is already happening. Has been for the past year or so. It’s in those documents No1 reads. And by the time it shows up on a Bloomberg terminal it will already be over. We’ll be looking at a steadily 100-150$ silver price and all the postmortems will explain how it was - of course - obvious in retrospect. And the people writing these postmortems will be the same people who called everything resilient a year back.

Anyway. Silver hit $87.88 on Wednesday, a two-month high. Tuesday it was $84.20. Today $83.5. Monday it ran 7.2% on the US-China tariff truce. A week before that, $80. Three months before that, $121.67. Ten weeks of intercepted missiles, destroyers in Hormuz, “love taps” between US and Iranian boats, a one-page memorandum mediated through Pakistan, and the chart looks like me trying to draw some mountains.

The “official” story is that silver tracks oil which tracks Hormuz which tracks whatever Trump posts before breakfast. And when oil ran, silver bled because rates would stay higher for longer. And then when the surrender document leaked through Axios - erhm, I mean the MOU, silver popped 6% on the day.

Then Goolsbee reminded everyone that inflation has not actually cooled toward 2% and has accelerated since the war began. Apparently that was kind of inconvenient because everyone nodded politely and promptly ignored him.

The April jobs print came in at 115k against expectations of 62k. Bloomberg called it resilience. Well, I have other words. None to be spoken in polite company. (The trick to beating expectations is “massaging” them.)

Tuesday’s CPI then came in at 3.8%, the highest reading since May 2023. Core at 2.8%. Both above forecasts. Suddenly everyone thinks the Fed won’t cut for the rest of the year or even hike into April next year.

Bloomberg is frantically searching for a way to re-define “resilience”, I guess.

Something else that has nothing to do with Iran is happening behind (vault) door number one…

Look at what the US actually exported across February and March. Around 500 metric tons more silver left the country than was withdrawn from COMEX vaults. Roughly 17.3 million ounces. If exports exceed COMEX outflows by that much, the metal is coming from somewhere else. And it ain’t thin air I can tell ya!

Probably it’s just refiners that are selling direct to customers... Or it’s shadow inventory from the bullion banks that was stocked during easier times and which they are now quietly draining. Or both at once.

The exchange that purports to be the main venue for trading, is increasingly being sidelined.

Remember I told you it’d be a whimper? This is whimpering in real time…

Nothing as dramatic as with nickel and the LME.

Just months of customs data indicating that the people who need bars have stopped queueing at the COMEX window and started calling the refiners directly.

And it won’t turn up on Bloomberg terminals because it’s all OTC.

Another major shift is that UAE exports fell off a cliff in March, which is - for a lack of a better word - astonishing. What could have happened there?? (insert surprised face).

HK went the other way. You can take 3 guesses where UAE’s silver went instead.

UAE was the warehouse. The metal parked there to be moved later. But it got too hot there. The tailfin-through-the-roof kinda hot.

But Hong Kong is the SGE’s front door. That metal there is no longer being staged for some hypothetical buyer. It’s being straight gobbled up by the insatiable Chinese demand.

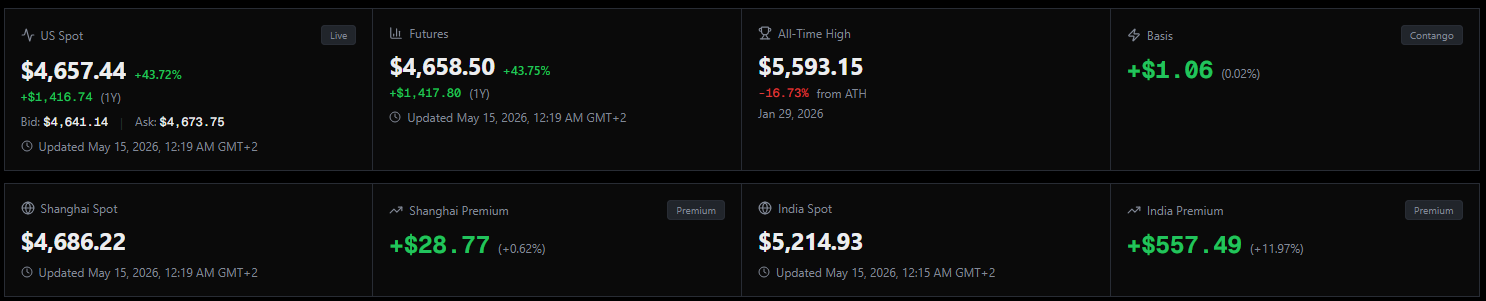

Now combine that with the persistent Shanghai premium (last I checked still 12-13% above LBMA spot), which is a very polite way of saying LBMA has stopped representing the price of silver. China’s January 1 export licensing rules ring-fenced roughly 65% of refined supply, which is their polite way of saying ‘we need this’. And Turkey pulled 20.34 million ounces in sixty days through the Swiss LBMA refiners, which is impolite any way you cut it.

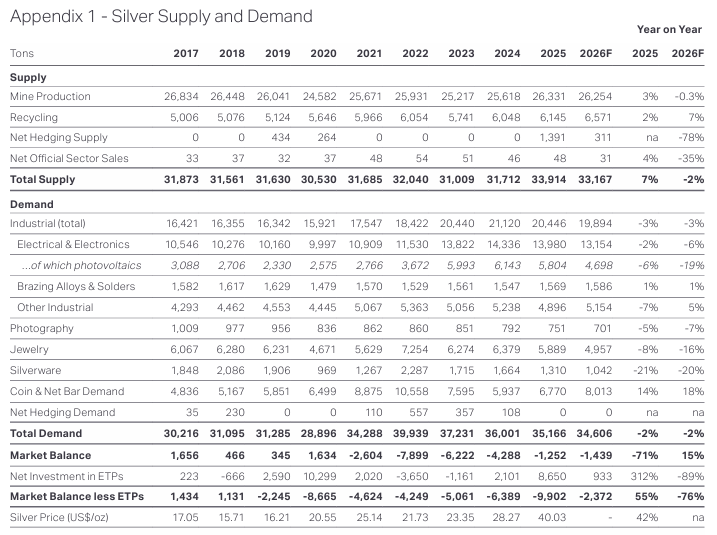

The Silver Institute’s official 43 (or 76) Moz deficit projection for 2026 does not yet include any of this.

Their annual model runs annually. The drain on COMEX runs daily. Reconciling those two facts is somebody else’s problem. I’ve got my physical.

Then there’s the sovereign layer: China imported a record 528 tonnes of silver in March. Highest monthly print on record.

India is going in the opposite direction, at state direction.

Modi started by publicly asking Indians to stop buying gold for a year to preserve foreign exchange reserves.

Then he doubled gold and silver import tariffs from 6% to 15%, in case the asking hadn’t landed.

Then, last week, he asked Indians to work from home and refrain from foreign travel to save fuel.

Basically the same thing. Oil and gold.

As you know, Indians have a fixation with gold. Something to do with not trusting their government to keep the currency stable. Or so I heard.

So what would the gov do? Pretty pretty please don’t buy gold.

That’s going to work. Yup.

So… We got more exports from the US than before, UAE taken out of the picture (quite literally), China via Shanghai & HK gobbling just about anything that’s not fixed, and India (trying to) block any imports.

Where does that leave us?

My take is that the low is in.

Probably no new all-time high this year. That $121.67 print on January 29 burned a lot of weak hands on the long side, and that kind of leverage needs time to forget.

What I expect instead - and I’ve been saying this since Jan 1 - is a chop between $70 and $100 for the rest of the year, working through the immense rise of 2025 the way digestion works through a large meal. Slowly. Occasionally uncomfortably. But productively.

That range is structurally different from anything the miners have lived through.

A stable floor above $70 is the thing they have been waiting for.

AISC for about ANY miner suddenly looks comfortable. Free cash flow modelling stops requiring three asterisks and a footnote about silver volatility. Hedge books, capex, dividend policy, all of it gets planned against a price that actually finances growth instead of one that might revisit $30 next quarter on a paper flush.

The miners have spent years drawing up business plans against a number that might not exist next week. Now that number is the floor.

They’ve been the ugly cousin of the entire rally. Beta didn’t show up because silver was moving too fast and too violently for equity markets to underwrite. You can’t price a producer when the underlying does $40 round trips on a Tuesday.

The stable floor changes the calculus entirely.

The producers that have been trading as if the rally might reverse tomorrow gets to be re-rated as the market starts to consider it won’t.

The refiner-direct flows don’t need new highs to keep grinding. Industrial users who got locked out at $120 learned their lesson and are now buying every dip below $80. Solar and EV manufacturers came back as strong buyers as soon as the price broke down.

The slower bid doesn’t show up as fireworks. It shows up as a floor that quietly stops moving down.

The risk to this thesis is a fresh physical accident. Another Diwali-style drain. An actual COMEX delivery fail. An SGE move that triggers a global scramble. Or hell, even a stock market crash where everyone needs liquidity. AGAIN.

Any of those would break the range upward before the miners get the stable backdrop they need.

Anyway. The structure of the market is shifting.

The exchange that used to set the price is being quietly bypassed by the people who actually need the metal.

And as of today, the JPMI physical premium has tightened to roughly 20%, one of the lowest divergences in months.

Not because physical fell. Well, maybe a little. But mostly I feel COMEX is finally catching up to the real price.

The repricing everyone’s asking about is already happening.

Not with a bang but a whimper.

The value of silver is a function of demand.

You know #1 - supply and demand.

Simple economics - and silver is both most conductive out of all the metals and most reflective - there must be high demand for that nowadays - so fair to deduce the price of silver based on that.

As for gold - that is a whole nether topic - but one wonders how much gold is actually in Fort Knox?

A slow build is always more sustainable than a huge spike, and it’s good not to make waves but cruise under the radar lest you attract attention