Clearing member 991

The buyer of last resort

There’s a report that came out that should be front page news.

It won’t be.

The world’s all too busy watching missiles redesign Gulf state architecture and oil prices give risk managers early retirement. But buried in a PDF that maybe twelve people downloaded, something happened that I think matters more than any of that other stuff.

The exchange stepped onto the field and started playing for one of the teams.

Yesterday I wrote about why precious metals are getting crushed while the world burns. GCC liquidation, dollar squeeze, margin calls - three theories, all probably true simultaneously.

This morning I woke up to a Bloomberg reporting about Chinese customs data: 790 tons of silver imported in the first two months of 2026. February alone was 470 tons.

The highest monthly import volume ever recorded.

While paper silver keeps heading down, China was vacuuming physical metal off every available shelf on the planet at a pace never seen before.

The SGE/SHFE daily report from today adds some more colour: SHFE vaults holding at 362T, SGE vaults down nearly 100T in a single week.

Price down. Metal leaving. Both at the same time. Totally makes sense!

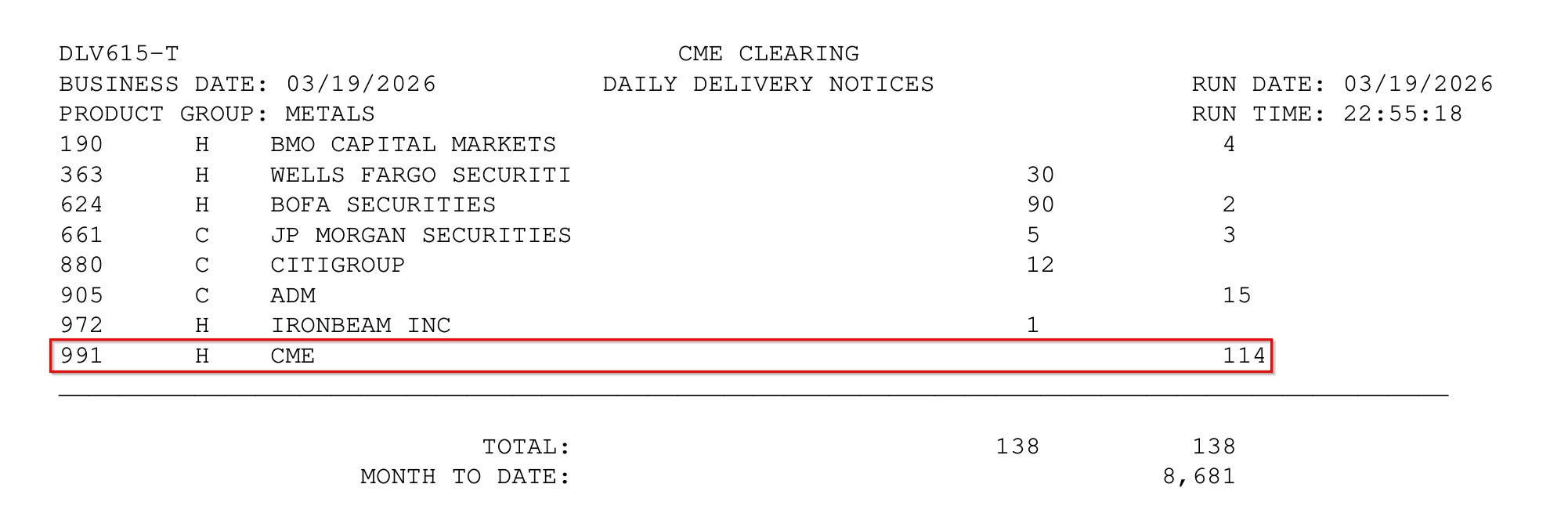

The CME publishes a daily delivery report. It lists who delivered silver (the shorts) and who received it (the longs). Almost nobody reads it. Most days you wouldn’t bother.

March 19, 2026 was not most days.

138 contracts delivered. On the issue side, the banks showed up like it was bonus season. BofA pushed out 90 contracts. Wells Fargo, 30. Citigroup, 12. JP Morgan, 5. If this were a garage sale, there’d be an “everything must go” sign.

They were all short, had the metal and wanted it gone.

Now. Who was on the other end to receive?

BMO: 4. BofA: 2. JP Morgan: 3. ADM: 15.

And clearing member 991 - CME, house account - stopped 114.

The exchange itself absorbed 82.6% of the day’s deliveries. 570,000 ounces caught by the referee. At what point does the referee scoring most of the goals make it a totally different game altogether?

Month-to-date running total: 8,681 contracts. 43.4 million ounces.

The banks are throwing silver across the counter as fast as they can. And on the other side... tumbleweeds. ADM took 15 because they’re industrial and actually need the stuff. A few banks grabbed token amounts. Everyone else? Crickets…

So the clearing house became the buyer of last resort. Because the alternative is a failed delivery, and failed deliveries in major contract months tend to attract the kind of regulatory attention that makes people suddenly want to spend more time with their families.

This is flying completely under the radar. The financial world is consumed by $111 Brent, by debt crossing $39 trillion (or is that $40T now?), QUAE. No1 is pulling delivery reports after close and counting which clearing members stopped how many contracts.

Which is exactly how structural breaks happen. Not with a bang. With a PDF that nobody reads.

Today was a pile-up. Again. Of course it was… Monthly ETF options expiry AND the rebalancing day for GDX, GDXJ, SIL, SILJ, SGDM, and SGDJ. On the same day.

For the uninitiated: the people who sold those option calls have a strong financial incentive to make sure they expire worthless. Every call that finishes out of the money is pure profit for the writer. So they lean on the price into expiry. Hard.

When ETFs rebalance, you get mechanical selling.

And the algos frontrun all of it because the schedule is public.

Three layers of selling stacked on top of each other.

It’s the most predictable mugging in finance. They even publish the schedule.

So if you ever want a discount: make sure you raise cash a few weeks before OPEX days. Monthly is the big one. Weekly plays too, but less so.

Now if nobody on COMEX wanted silver, and China is buying it at a record pace... that doesn’t actually make sense. Unless you stop conflating “COMEX paper longs” with “silver demand”.

The people who got wiped out weren’t silver buyers. They were leveraged futures traders who wanted exposure to silver’s price movement. When margin calls came, they vanished like my portfolio did in January. China’s buying happens through completely different channels - direct imports, OTC deals, refiner contracts. Those buyers never touch a COMEX delivery report. They don’t have to. They just show up with a ship.

That still doesn’t explain though why the CME house account is catching 82.6% of what does come through. If the longs are gone, delivery notices should have dried up entirely too. Yet 138 still went through. Someone is receiving. And that someone is overwhelmingly... the exchange itself.

So what is the house account actually doing with 570,000 ounces a day?

Possibility one: just keeping the lights on. When shorts deliver and there’s no matching long, the clearing house steps in as counterparty. Normal clearing function. Except at 82% of volume it’s less “function” and more “the function”.

Possibility two, and this one’s interesting. Think about the flow mechanically. CME house stops 114 contracts. CME now holds warehouse receipts. Those receipts can be used to withdraw metal from COMEX vaults. That metal gets shipped to London. London backfills SLV or the LBMA free float.

This would explain the house stops AND the persistent vault outflows with zero deposits. All leaving, nothing in.

And it would explain something pmbug flagged this week: SLV vault stock is bleeding while lease rates are dropping. The LBMA is being fed metal from somewhere. That somewhere might be COMEX, with the clearing house acting as the pipeline.

Now. If metal was lent out of SLV - which has been alleged for years, the custodian being JP Morgan, the same JP Morgan that’s issuing delivery notices on the other side of this trade - and now needs to be returned to match outstanding shares... this would be one way to do it quietly. Buy through the house account (no name attached), withdraw from vault, ship to London, file as ETF deposit. Clean. Tidy. The kind of operation that would make a forensic accountant’s eye twitch.

(I am not making an accusation. I am merely describing a purely hypothetical mechanism that would or could potentially, in theory, under certain circumstances, possibly be consistent with what the data might suggest if interpreted in a certain way. There’s a difference. My lawyer made me say that.)

(I don’t have a lawyer.)

Possibility three: someone big is buying through the house account to stay anonymous. A sovereign wealth fund, a central bank, a large industrial user who doesn’t want their name showing up under a clearing member. At 570,000 ounces per day you could stack serious tonnage without appearing in any public report.

Possibility four: the CME is a for-profit corporation that sees every delivery report, every vault flow, every inventory number before anyone else. At $70 silver with this structural backdrop, I would be buying too. Just saying.

I don’t know which one it is. Probably some combination. But regardless of which explanation you prefer, the metal is still leaving. The vault data doesn’t care about interpretations.

So here’s the picture. China is importing at record pace while draining its own exchanges. Chinese export restrictions have choked off the world’s largest refiner. The COMEX is bleeding inventory with zero inflows. The CME house account is absorbing 82.6% of delivery notices. And the paper price sits at around $70.

Efficient markets, ladies and gentlemen. (yeah, I’ll keep repeating it)

The price says nobody wants silver.

Every vault on the planet says otherwise.

All of this is temporary. The GCC liquidations, the margin calls, the forced unwinding - all of it has an expiration date. Either the Gulf states stabilise (unlikely while infrastructure is being remodelled by Iranian missiles) or they impose capital controls. Either way, the fire-sale selling will eventually stop.

But the physical shortage doesn’t go away. It’s structural. Years of consecutive global deficits. China’s export controls aren’t going away. Solar panel demand isn’t going away. The war, if anything, turbocharges the pivot to energy independence.

London’s free float has already been cannibalised. COMEX is next.

I bought more SILJ calls today. I didn’t feel good about it. The price was dropping way too fast to my liking. But I know that nothing structurally has been solved.

No idea if this was thé bottom.

I still have ~12% cash left to deploy.

Tales From the Financial Crypt.

For some reason I feel compelled to share my story and here seems like the right place. Hope No1 doesn’t mind.

Way back in 1989 (in the Before Time, in the long long ago) I opened my first trading account with a Canadian broker whose initials are RG. I was a small potato and the commissions were killing me - $100 on a round trade. In addition I realized what passed for advice was merely them scaring up buyers for their larger accounts who were selling. So much for the Chinese Wall. About that time the first discount brokers appeared in the USA, so I opened an account with Waterhouse Seattle. They were great. Always picked up on the 2nd or 3rd ring, great execution, and I could even chat with their people on a slow day. So that went well for a while until they were bought out by TD Bank, at which point I was told they couldn’t service me anymore and I’d have to switch to the Canadian side where the fees were almost 50% higher.

Now I had every right to be there under GATT and NAFTA rules, but they wouldn’t budge, so I moved to a boutique broker down in Florida. That was ok for a while, but then I got a message saying they had no choice but to terminate our relationship. Seems the Canadian discount brokers had leaned on the Canadian govt. who leaned on the US govt. who leaned on Finserv to chase us out of there using some obscure rule about disclosure! All in complete violation of GATT. So then I shopped around for a self-clearing broker and wound up with MANN in Chicago who scoffed at the mere mention of Finserv.

That was even better in a way because they were also CME brokers and I was ready to step into that world, having been coached by an actual CME floor trader. Next thing I know they bought out some failed Canadian operation whose name I forget and I was back to square one! I considered moving to London, but I was only a slightly larger potato by then and the time and currency differences made it not worthwhile. So, back to TD Canada as the cleanest shirt in the prison laundry where I remained until I hung it up for good in 2008. If you’re up big, take some off. That was Jim Cramer who said that (LOL) so I did him one better and took it ALL off and never looked back. Ironically, somewhere towards the end of my relationship with TD I received a settlement for something like 31 cents. Seems I was part of some class suit over bid rigging or something. Never did learn the details.

So there's my sad story of what it’s like to try and catch a break in this world. I came into the market post the 87 crash, made my fortune (such as it is) in the tech bubble and subsequent gold rush, gave a good chunk of it back in 2008 but left with enough to last my declining days and leave the wife not hating me should I happen to go first (which is very likely given the kind of life I’ve led). I honestly don’t envy any of you at this point because it’s only gotten worse since then, so the best I can do is wish you good luck because I’m pretty sure you’re going to need it:)

Oh, and here’s some more irony for you. Way back at the beginning I was a subscriber to James Davidson’s Strategic Investor. That was at a time when interest rates were pushing 20% and he was pounding the table to buy USG 30Y zero coupon bonds. Had I taken his advice and just sat on them to maturity I’d have been in almost as good a shape as when I bailed, and with far less stress. Lesson here is if a golden opportunity presents itself, grab it with both hands.

I wish I didn't live in such interesting times!