Everything, Everywhere, All at Once

Everything's fine. Truly. Nothing to see here.

A quick word before we get into it.

Some of you have been here with me since before the war. You came for the silver thesis, the COMEX mechanics, the petrodollar erosion - the slow-motion financial story I’ve been tracing for years and started to share recently with the world. Lately however, all you’ve gotten from me is daily missile counts and geopolitical play-by-plays.

I heard you. And I owe you this piece.

The war had absorbed me completely. I make no apologies for that - it’s THE biggest thing happening on the planet, and pretending otherwise would be dishonest. But I do feel it’s coming to some kind of focal point. Not an end, necessarily. More a kind of crystallisation. The kind of inflection point where the consequences of the last two weeks start showing up in places that have nothing to do with Iran.

The Stoics had a word for it. Sympatheia - the idea that all things are mutually woven together, that a tremor in one corner of the cosmos moves through everything else. They meant it cosmologically. I believe in this with my whole heart, mind and soul. Everything is connected.

And maybe that’s why I write these things down. Rupert Sheldrake once observed that crossword puzzles get easier to solve as the day goes on - not because the puzzles change, but because more minds have worked through them. The solutions accumulate somewhere. Call it the Aether, call it morphic resonance, call it whatever you like. The more people who see clearly what’s happening, the more that clarity spreads to people who haven’t looked yet.

So. Consider this my contribution to the Aether.

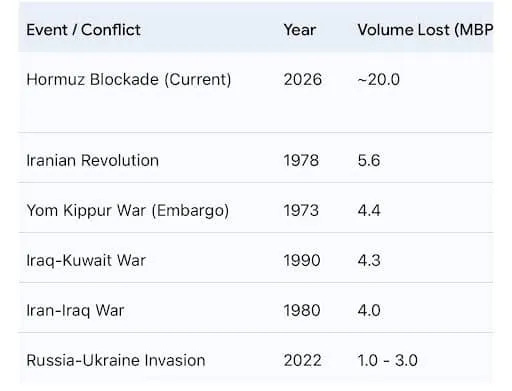

Let me start with a number. In 1980, when the Iran-Iraq war disrupted global oil supply, the volume lost was around 4 million barrels per day. Painful. The world went into recession. Volcker raised rates to 20% to kill inflation. It nearly killed the economy in the process. We called it a crisis and we meant it.

The current Hormuz blockade is running at roughly 20 million barrels per day.

The futures market, in its infinite wisdom, is pricing a quick resolution.

Trump says the war is “basically over”. His Defence Secretary says it’s “only just the beginning”. One of them presumably has read the intelligence reports. The other has a golf course booked.

That’s the pin.

But that’s not the bubble.

Even in the most optimistic scenario - ceasefire tomorrow, everybody shakes hands - the Maersk CEO noted it takes at least ten days after a ceasefire for tanker insurance to clear. Then mine-clearing: Iran has been laying mines in the Strait, and removing them will take weeks to months. Then tankers reposition, loads getting secured, and finally the flow resumes. The oil futures curve is pricing step five as if it follows step one with a 48-hour lag.

It cannot physically happen on that timeline.

And Iran isn’t just shooting wildly at targets. Yesterday, Fujairah - the world-class bunkering hub sitting outside the Strait, the bypass everyone assumed would soften the blow - has been deliberately targeted. Tehran isn’t just closing Hormuz. It’s also closing the workarounds. One by one. Iran got fed up and decided to take down the imposed sanctions one way or another. And USrael just gave them the ultimate excuse.

If you’ve been reading my silver papers, you know there is a gap. A gap I call “PvP”… No not the gaming term. The Paper vs Physical.

And oh boy. Is it screaming!! Brent futures in New York closed Friday at $104. Elevated but ok-ish. Dubai crude - you know, the real physical oil, real barrels, real buyers - was trading around $127-140. Normally Brent commands a premium over Dubai. Now Dubai is $37 above the paper. And that’s just crude. Bunker fuel in Singapore hit $140 per barrel this week. In Fujairah, $160. High-grade marine fuel, $175. Ships burning fuel right now are paying those prices regardless of what the futures strip says in New York.

Silver at a $12 premium to Shanghai? pffff Silver… Amateur hour compared to oil!

If you’ve read Strait to Brrrrr, none of this is surprising. Paper price is massaged. The New York futures desk is clearly on something the physical buyers aren't.

However this started, this isn’t a military confrontation anymore. I’m even starting to doubt it ever was. The Strait stays closed, oil stays elevated. Oil stays elevated, inflation stays elevated. Inflation stays elevated, the Fed cannot cut. The Fed cannot cut, and $36 trillion in federal debt - already costing $880 billion a year in interest before the war added a billion dollars a day to the tab - gets rolled over at rates that make it progressively less serviceable. The dollar weakens under that strain. A weaker dollar makes the next barrel of imported oil more expensive in dollar terms. Which feeds back into inflation. Which keeps the Fed pinned.

It’s a loop. Iran just needs to keep the strait closed long enough for it to complete a few rotations. The bond market has noticed. Treasury yields are rising in the middle of a geopolitical crisis - not falling. Capital isn’t fleeing to bonds. It’s fleeing to gold. That is a verdict on the US fiscal position.

Trump knows the physical reality, which is why last week he called Putin. The country America has been sanctioning for four years. The one it branded an aggressor, a pariah, an enemy of the liberal world order. He called to ask for help. Then he went further and lifted Russian oil sanctions outright. A Democratic Senator responded with perhaps the best summary of the year: “Looks like we fought Iran and Russia won”.

What else? The IEA approved a record 400 million barrel reserve release. Bessent telegraphed futures market intervention to cap prices. Russian sanctions lifted. Each one a gesture. On my feed someone quoted: “The oil market is massively short of supply. The other options the administration has, other than ending the war, are actually pretty limited”. Woops.

That’s the pin. But actually, the pin in itself doesn’t matter. Really truly doesn’t matter. What does matter greatly however, is WHAT it pricked…

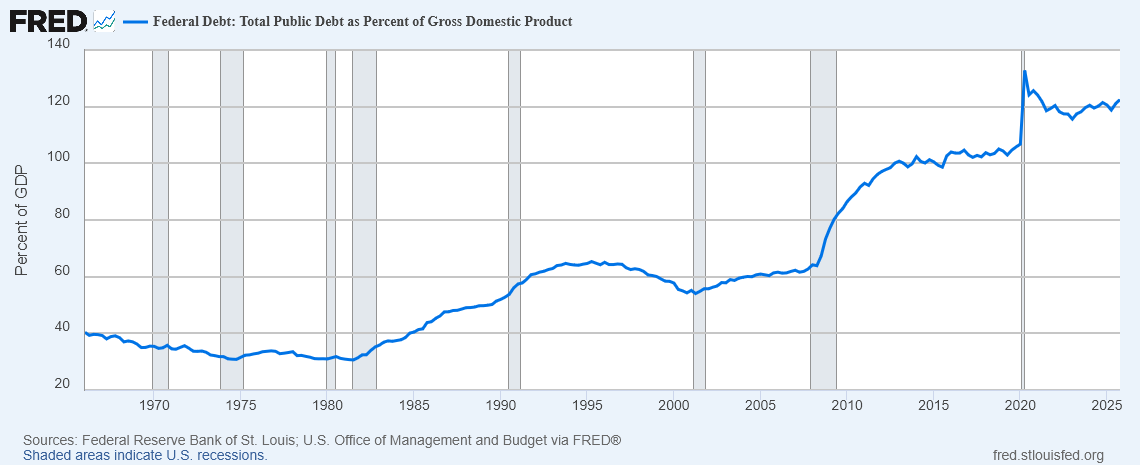

In 1980, US federal debt stood at 26% of GDP. Today it’s 120%. That’s the difference between the same shock hitting a healthy patient and hitting someone already on oxygen. The Volcker treatment that worked then is structurally unavailable now. But don’t worry! These are the same people who called inflation transitory. I'm sure they've got it. This time.

The interest bill on existing debt is already $880 billion a year, more than defence, more than Medicare. Rates at 20% on $37 trillion would cost more than the entire federal budget in interest payments alone. That lever doesn’t exist anymore.

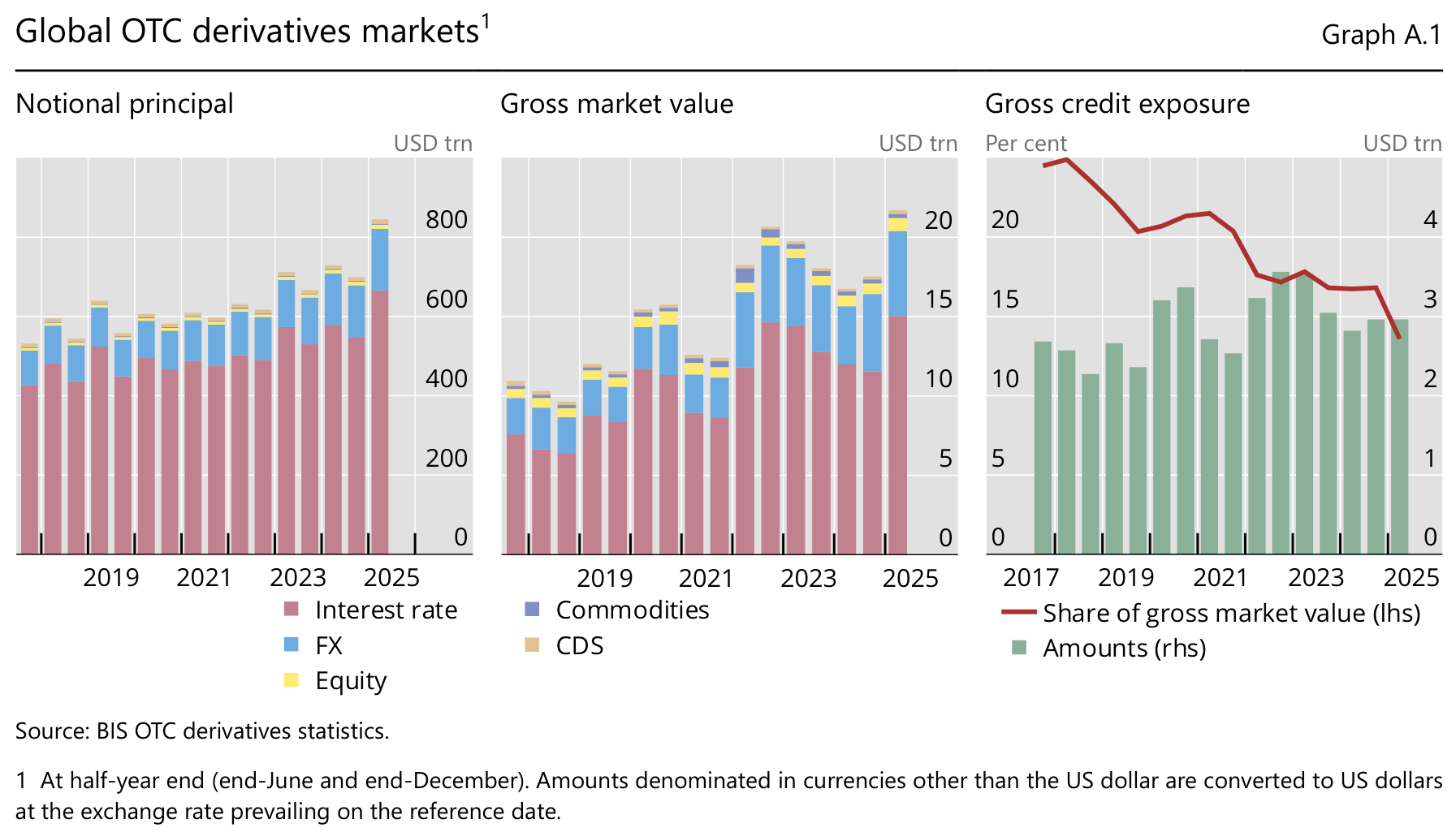

What exists instead is $846 trillion in notional OTC derivatives. Up from $108 trillion in 2000. An eightfold expansion in 25 years, and mid ‘24 → ’25 was the largest growth rate at 16% since 2008.

To put that number in some kind of human context: $846 trillion is roughly eight times the entire global GDP. With 1% of it you could buy every company in the S&P 500 twice over. With 0.01% you could buy Warren Buffett. With a rounding error - 0.0001% - a superyacht, a sports franchise, and a small Caribbean island, and you’d still have 99.9999% left. Nobody has this money, of course. Nobody owns $846 trillion. It’s the notional value of bets stacked on top of bets - leverage and hedges and derivatives daisy-chained to other derivatives. It nets out in normal conditions. In abnormal conditions, “nets out” becomes “finds out”.

Buffett called them ‘weapons of mass financial destruction’ in 2003. The book was $85 trillion then.

The bulk of the current book - around $548 trillion - is interest rate derivatives. All of it priced on a world where oil is $70 and rates are roughly stable. Guess what just happened? Oil exploding (quite literally at times) make counterparties not being able to meet margin calls (guess why gold and silver are trembling so much) and that failure cascades through the chain.

The private credit system was already the weakest link before the war. I covered the gating wave in my previous article so I’m not going to repeat it here, but the language from people who are in the know got pretty alarming. Mohamed El-Erian reached for Bear Stearns 2007 as his reference point. Dimon started talking about cockroaches. Dimon… Talking about cockroaches… The Treasury Secretary himself said he was ‘concerned’ about private credit. When the man responsible for placing a trillion dollars per quarter in new debt publicly expresses concern about the credit system he depends on to function, well… I’ll leave it at that.

Think the gating’s bad? Let me reassure you *evil grin*. One in five companies in the Russell 3000 cannot service their debt from current income. Over half of all investment grade paper is a single downgrade from junk. $5 trillion in corporate debt rolls over in the next four years at current rates, into a war-driven inflationary environment the Fed cannot cut its way out of. The losses are in there. Just not visible yet. When they surface, the institutions holding private credit will face redemption pressure at exactly the moment public markets are offering their best entry points since 2022 /s. Nah, just kidding. They dump whatever they can. Anything, just about anything unrelated with their illiquid portfolio will be hit. You've seen this movie before. Gold fell when Iran struck. Silver fell. Same mechanics, a tad larger. Think ‘08 or ‘00 on steroids.

Now picture what happens when the equity markets start to move. The S&P 500 closed up 1% on Sunday night. The Dow gained 388 points. Meanwhile, fertiliser benchmarks are up 25-44% in seventeen days. Think food. Helium has doubled. Think chips - not the edible ones. Pharmaceutical feedstock pipelines are depleting. The wall between the financial “economy” and the real one is still holding. Walls do that, right until they don’t.

When people need cash fast, they sell what’s liquid. ETFs are the most liquid thing in the world. They sell indiscriminately - tech, gold miners, silver, and just about anything else. You don’t sell what you want to sell. You sell what has a bid. And passive investment? Volume wise, ETFs are like 60% of US equity markets (2024). In 1996 that was only 6%. Which means that when selling starts it’s mechanical. No analysis. No discrimination. Every ETF holder hitting the same exit through the same small door at the same time.

Think of “Liberation Day” as a test run. First-ever simultaneous crash in stocks, bonds, and the dollar - the thing that was supposed to go up when everything else went down.

Tie into that the 401k withdrawals that hit a record high this week. The passive investment machine is leaking from the bottom while demographics drain it from the top.

Feeling comfortable yet? *super evil grin*

Underneath all of this, slower than any war and more permanent than any crisis, is something the financial press doesn’t really mention:

People aren’t having any children.

US fertility hit an all-time low in 2024. The general fertility rate is still falling. IMPLAN puts 1.4 million fewer Americans contributing to housing demand, retail spending, and service consumption in 2025 than trends would have predicted. To put that in numbers: $104 billion in GDP. Not exactly gone, not really disappeared. It just never existed in the first place.

It’s a vicious circle: housing is too expensive, so young people delay children. Fewer children means less future housing demand. Which should eventually reduce prices, except the lag is 20-30 years, and in the meantime housing stays expensive, so the people who couldn’t afford a house still can’t, still don’t have children, and the loop tightens at its own pace regardless of what the Fed does or what happens somewhere in the narrow waterways in exotic places.

Added: the boomers are saying bye sayonara.

The generation that inflated every asset class for 40 years through automatic 401k contributions is, somewhere around now, flipping from net buyers to net sellers. Of course it’s impossible to say like “March, 17: boomers start to cash out their 401ks”… Nope, the tide just turns. The same passive machine that provided an inexorable, automatic bid for equities and bonds and real estate - every payday, every year, for four decades - begins to redeem. Quietly. Continuously. For the next twenty-some years. Every asset they inflated on the way up faces a headwind on the way out. Not a crash. A long, grinding, demographically-inevitable ratchet.

Another angle I want to cover is the petrodollar. I covered this already in “The Bretton Whoops”. But the short version is: oil was priced in dollars, dollars were recycled into Treasuries, and the US military keeps the Gulf safe. It required two things - a reliable dollar and a credible security guarantee. The dollar’s reliability cracked in 2022 when Washington froze Russia’s reserves. The security guarantee cracked when the US started a war they cannot finish.

The dollar’s share of global FX reserves has since fallen to around 45%, the lowest since the 1990s. Gold’s share has quadrupled in twelve years. Gulf states are reportedly discussing pulling investment commitments from the US.

And now Iran has done something structurally interesting. It didn’t just close the Strait - it converted it into a tollgate. The toll isn’t money - yet. It’s alignment. Ten countries have been offered safe passage: China, India, Pakistan, Turkey, and others. The US isn’t on the list. This isn’t a military tactic. It’s economical.

Lots of people have the wrong framing. They think “petrodollar is dead, long live the yuandollar”. Right? Wrong frame entirely. China doesn’t want a reserve status. Couldn’t stomach it if it tried. Because a reserve currency means running a permanent trade deficits to pump your currency into the global system - America has been doing this for 50 years and the reward is a rust belt, a $37 trillion debt tab, and a bond market that needs foreigners to keep showing up or the whole thing seizes. China watched that happen and said: 不用了,谢谢. And opening the capital account enough to make yuan genuinely reserve-worthy would mean letting money flow freely across the border - ending the CCP’s ability to direct credit and control the financial system on Beijing’s terms. They’d sooner eat the wallpaper.

What the yuan-for-oil arrangement being implemented actually is, is an industrial policy dressed as currency diplomacy. You sell your oil into the permitted lane. You receive yuan. Now you’re sitting on yuan in a system with capital controls - you can’t just convert it and park it wherever you like. Your options are: buy Chinese goods, buy Chinese infrastructure contracts, invest in Chinese assets. That flow cycles straight back into Chinese factories and Chinese employment. China doesn’t have to stimulate its domestic consumption anymore. It exports the demand problem onto its trading partners and invoices it as a geopolitical arrangement. Three hundred million jobs - and unlike the US - no helicopter money required.

Those dollars that used to flow into Treasuries don’t just suddenly rush home. They just stop showing up at the next auction. Treasury needs to place roughly a trillion dollars every hundred days. Fewer buyers means higher yields. Higher yields mean the Fed is cornered. A cornered Fed means the printer runs. Same mechanism as demographics, same mechanism as the derivatives book, same direction.

My long-running conviction - and I’ve been saying this long enough that it stopped sounding contrarian and started sounding obvious - is that the world ends up back on a gold standard. Not the romanticised version where you rattle coins in your pocket. Though honestly, with modern payment rails, a gold-backed account is functionally identical to a dollar account. You’d never touch the metal. You’d just change the ticker from USD to XAU and carry on. The technology exists right now. The obstacle isn’t infrastructure. It’s that the people running the current system would rather light themselves on fire.

What happens first, before any grand declaration, is narrower: gold becomes the settlement layer between sovereigns who no longer trust each other’s paper. The US is apparently net-settling its trade deficit with China in gold - if that data holds up. In three of the last four months it seems that gold is flowing East. No Bretton Woods conference. No announcement. Just two countries quietly deciding that when the paper gets complicated, the metal clears the table. That’s how monetary systems actually change - not by proclamation but by practice, one bilateral settlement at a time, until enough of them are doing it that someone calls a conference to ratify what’s already happened. The Bretton Woods conference didn’t create the dollar system. It formalised what the war had already decided.

The next conference is coming. It just hasn’t been scheduled yet.

Silver. Because I can’t write a piece about systemic fragility without it, and because this week’s data is worth your attention even if the price chart isn’t.

The paper price looks terrible. Miners are trading like silver is heading back to $40. Silver Santa - one of the accounts I follow on Twitter (yeah, I’m old) - moved 40% to cash, describing “a strong pre-COVID feeling”. The technical picture is ugly.

But the crucial part: the physical reality didn’t get that memo.

The COMEX “run rate to zero” ticked down to 89 days as of Friday, from 93 days on Thursday. Four days burned in one. The SGE briefly stopped publishing silver inventory data mid-week, then quietly resumed. Shanghai is still paying a 13-17% premium over London. The same paper/physical divergence playing out in oil is running in silver at a slower pace with a much longer fuse.

But what does a draining vault have to do with your savings account?

More than most people think. The COMEX sets the global silver price. But if the COMEX increasingly doesn’t have the physical metal - and the run rate suggests it won’t for long - then the price it sets is a fiction. An unallocated silver account at your bank is a claim on that fiction. An ETF share is a claim on that fiction. When the fiction and the physical reality eventually converge, it won’t be because the paper comes up to meet the physical. It’ll be because the paper can no longer pretend.

Same mechanism as Dubai crude. Same mechanism as the derivatives book. Just a slower fuse.

When $68 trillion in US equity markets eventually moves - and it will - and the indiscriminate ETF selling hits everything, and the margin calls cascade through a derivatives book built on assumptions that no longer hold, and zombie companies start defaulting, and the boomer redemptions add their steady mechanical pressure, and 401k hardship withdrawals accelerate - the question of where capital goes becomes very concrete. Bonds? Already struggling to absorb a trillion per quarter. Cash? In which currency? Real estate? In a demographically challenged market with rising yields?

Gold has a structural bid from central banks who drew their conclusions in 2022 and have been buying ever since. Silver has vaults on an 89-day countdown and a paper price that hasn’t caught up yet.

I’m buying the dips. Have been. Will continue.

(A small aside: I’m considering opening a dedicated Substack to document my trades in real time - with a ten-minute lag - for those who want to follow the positions, not just the analysis. The analysis stays here, free.)

None of this is hidden. None of it requires a security clearance or even a Bloomberg terminal. It’s all there, in the vault data, the yield curves, the fertility statistics, the derivatives book, the bunker fuel prices. The information exists. The pattern is legible.

The question was never whether this would happen.

The question was always who would be holding paper when it did.

Tomorrow, Powell walks to the podium. He’ll probably have a new acronym handy. They always do. TALF, TARP, BTFP, BTFD, YOLO, CTRLP. Each crisis gets a fresh name but the same printer.

Maybe a new suggestion: EEAO

"the people running the current system would rather light themselves on fire"

The terms are acceptable

discovered this place about a week ago. so glad I did. Such an infinite difference between technical skill and wisdom