Once upon a time in the land of infinite liquidity

A fairy tale

A subscriber responded to a previous article with an observation about passive investing. That triggered me to unpack passive investing - and ETFs more specifically. He saw the systemic damage. The inevitable pop when enough smart money decides to exit.

And he’s absolutely right. But the full picture is even messier than most people realize.

Once upon a time, in a kingdom called Wall Street, the wise elders made a remarkable discovery. They found they could create magic mirrors - enchanted objects that would show you the entire kingdom’s wealth, updating thousands of times each day. You could buy these mirrors. You could sell these mirrors. And the mirrors promised to always, always show the true value of what lay beneath.

They called these magic mirrors ETFs.

The villagers loved them. Why toil away studying individual companies when you could simply gaze into a mirror and own everything? The mirror-makers grew rich and powerful, and soon three great wizard families - BlackRock, Vanguard, and State Street - controlled most of the magic mirrors in the realm. This seemed like a good idea at the time.

The magic mirrors worked through an elegant spell called arbitrage. Special creatures - let’s call them arbitrage fairies (ie: Authorized Participants) - would flutter between the mirrors and the real world beneath. If the mirror’s reflection showed a price different from reality, the fairies would buy the cheap one and sell the expensive one, pocketing the difference and keeping everything aligned.

“The fairies will always be there,” the wizards promised. “They make free money by keeping our mirrors honest.”

And for many years, this was true. The mirrors became more and more popular. By 2024, more than half the kingdom’s wealth was stored in magic mirrors rather than actual holdings. Villagers who once studied balance sheets now simply bought mirrors. Easier. Cheaper. More diversified.

The word “diversified” was very popular in the kingdom. But there’s this thing about fairy magic. It only works when you believe in it.

One terrible spring in 2020, a plague swept across the land.

Panic gripped the kingdom.

Everyone rushed to sell their magic mirrors at once.

This is when the villagers discovered something disturbing.

The arbitrage fairies... just stopped working.

Investment-grade bond mirrors traded at huge discounts to reality. High-yield mirrors showed even bigger gaps. Even Treasury mirrors - supposedly the safest magic in the kingdom - showed massive dislocations. These weren’t rounding errors. These were people selling $100 of bonds for $94 because the fairy magic had broken.

Why didn’t the fairies arbitrage these massive profits? The answer was delightfully mundane. Their balance sheets were full. They’d already bought too much of the same stuff everyone was selling. The regulators had told them they couldn’t take on more risk. The magic profits just... sat there. Uncollected.

“This is fine,” uttered the wizards nervously.

It was not fine.

The top few arbitrage fairies handled most of the bond mirror business. When they refused to work, the entire system seized up. Alternative fairies didn’t have big enough wings to carry the load. The mirrors kept failing. The villagers kept panicking. The panic made the mirrors fall more. A perfect spiral into the abyss.

But then! The Great Wizard of the Federal Reserve - the most powerful wizard in all the land - stepped forward. He raised his staff and proclaimed: “I will buy the magic mirrors myself, using money I can create from thin air!”

The mere announcement stopped the panic instantly.

The mirrors recovered.

The fairies cautiously returned to work.

Order was restored.

The Great Wizard only bought a small amount of mirrors, but the promise - the unlimited backstop - was enough. Crisis averted.

The kingdom held a great council. “We must learn from this,” said the elders solemnly. “We were too reliant on fairy magic. We let too many people crowd into the theater. We must be more careful.”

Everyone nodded gravely. Regulations were discussed. Risk committees were formed. Reports were written. The arbitrage fairies promised to keep bigger balance sheets. The mirror-makers promised to monitor concentration risks. The villagers promised to understand what they were buying.

And they all agreed to be more careful next time.

The actors take their bows.

The curtain drops.

Or is it?

Let me tell you a secret: it didn’t finish. It only got bigger.

Strip away the fairy tale and here’s the reality: ETFs are just baskets of stocks wrapped in a tradeable wrapper. You want to own the S&P 500? Buy one share of SPY and you own a proportional slice of all 500 companies. Simple. Elegant.

The magic happens through something called the creation/redemption mechanism. Authorized Participants - typically large investment banks like JPMorgan, Goldman Sachs, Citigroup - can create new ETF shares by delivering a basket of the underlying stocks to the ETF sponsor. Or they can redeem ETF shares by receiving those stocks back. This process keeps ETF prices aligned with the net asset value of the underlying holdings.

When an ETF trades above its NAV, APs create new shares (delivering stocks, receiving ETF shares, selling them at the premium). When it trades below NAV, APs redeem shares (buying cheap ETF shares, redeeming them for stocks, selling stocks at higher prices). The arbitrage profit is small - maybe 5-10 basis points - but essentially free money as long as the mechanism works.

During normal times, this is flawless. The secondary market (regular stock exchange trading) absorbs 85-90% of all ETF volume. Only 10-15% touches the creation/redemption mechanism. Spreads stay tight. Prices track NAVs within basis points. Everyone’s happy.

Then March 2020 happened and revealed what happens when the machine breaks.

Let’s get specific about March 2020 because the data is stunning.

LQD, the largest investment-grade corporate bond ETF, traded at discounts exceeding 6% to NAV between March 16-20. That 6% gap represented roughly 25% of the total 20% price decline during the crisis. High-yield bond ETF HYG hit 8% discounts. Municipal bond ETFs showed 5% gaps.

Most shocking: TLT, the Treasury bond ETF tracking “the most liquid market in the world,” also gapped 5%. U.S. Treasury bonds, the ultimate safe asset, couldn’t maintain arbitrage alignment in their own ETF wrapper.

Why? The top 5 Authorized Participants handle 91% of fixed-income ETF creation/redemption volume, with the single largest AP controlling 51%. When these few institutions simultaneously hit balance sheet capacity limits, the entire arbitrage mechanism failed.

The mechanics of failure followed a predictable pattern.

Mutual funds experienced $250 billion in outflows during March - five times larger than the 2013 Taper Tantrum. They sold their most liquid holdings first: investment-grade corporate bonds and Treasuries. This flooded the market with exactly the bonds present in ETF redemption baskets. APs, already holding massive inventories of these same securities, refused to warehouse more despite huge arbitrage profits.

Transaction costs exploded. Investment-grade bond trading costs tripled from 30 basis points in February to 90 basis points by mid-March. High-yield bonds became nearly untradeable. Fixed-income ETF trading volume surged 245% for municipals and 67% for corporates, yet 92% of underlying bonds didn’t trade at all on the worst days.

By March 20, the investment-grade CDS-bond basis reached 280 basis points - meaning credit default swaps indicated far less default risk than bond prices implied. Three-quarters of total spread widening came from basis dislocations rather than actual credit deterioration. Alphabet, a AA-rated company with $120 billion in cash, saw bond spreads spike to 150 basis points while CDS spreads barely moved from 25 basis points. The market was pricing technical liquidation, not fundamentals.

Only Federal Reserve intervention broke the death spiral. On March 23, the Fed announced it would purchase corporate bond ETFs under emergency Section 13(3) powers. Investment-grade bond ETFs gained 7% immediately - before significant actual purchases. The Fed ultimately bought just $8.56 billion across LQD, HYG, and other fixed-income ETFs, never exceeding 5% ownership in any single fund. The backstop commitment mattered more than actual intervention.

But what changed since March 2020? Everything just got more concentrated.

Passive investing officially crossed 50% of U.S. equity mutual fund assets in 2024 - $16+ trillion versus $14.1 trillion in active strategies. This marked the first time in American history passive surpassed active. From 2014-2023, passive attracted $5.1 trillion in net inflows while active suffered $1.9 trillion in outflows.

The Big 3 asset managers - BlackRock, Vanguard, State Street - collectively control 71% of the entire ETF market and over 90% of passive equity funds. Their combined $11 trillion in passive equity assets exceeds all sovereign wealth funds combined. They are the largest shareholder in 88% of S&P 500 companies (438 of 500), holding approximately 23% of total voting power.

Within indices themselves, the top 10 companies now represent 40% of the S&P 500 - the highest concentration in over 50 years. The Magnificent 7 tech giants (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Tesla) alone account for 32%, up from 14% a decade ago. Some ETFs show even more extreme concentration: Vanguard Mega Cap Growth ETF carries 55% in just the Mag 7.

Investors often unknowingly amplify this concentration. Someone holding VTI (total market), SPY (S&P 500), and QQQ (Nasdaq 100) believes they own three different portfolios but actually has 40%+ allocated to the same 10 mega-cap stocks. Major broad-market ETFs have 50-70% overlap - far less diversification than appears on the surface.

Passive investing creates a self-reinforcing cycle on the way up. When money flows into index funds, those funds must buy constituent stocks in proportion to their index weights. Market cap weighting means the biggest companies receive the most buying pressure.

This creates momentum effects. Stock prices rise → market cap increases → index weight increases → more buying required → prices rise further. The cycle feeds itself. Companies in major indices receive valuation support purely from mechanical buying, regardless of fundamentals.

Academic research documents that a 1% increase in ETF ownership corresponds to a 21% reduction in how much prices respond to earnings announcements. The signal from actual business performance gets drowned out by the noise from index flows. Stocks with high passive ownership show rising betas (increasing correlation with the market) while actively-held stocks show declining betas. Diversification benefits erode as everything moves together.

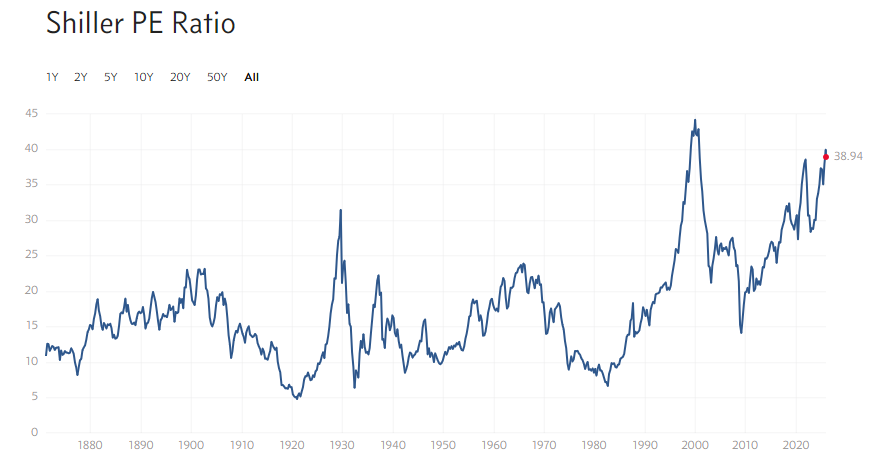

The valuation backdrop supporting this positive feedback has reached historic extremes.

The Shiller PE ratio sits at 38 versus a historical average of 17. Market cap-to-GDP (the Buffett Indicator) remains significantly elevated. The earnings yield of 2.6% compares unfavorably to 4.5% available on Treasury bonds.

Bank of America warned in February 2025 that passive investing had hit “critical mass” at 54% market share: “Passive disregard for valuations & fundamentals means big upside from innovations... but big risk in a bust cycle.” The momentum machine works perfectly as long as flows continue in one direction.

The same mechanics that amplify gains on the way up amplify losses on the way down - except worse, because liquidity disappears during stress.

When investors redeem ETF shares, the ETF must sell underlying holdings to raise cash. Unlike active managers who can choose which positions to sell or hold cash buffers, passive funds must maintain exact index weightings. Every dollar redeemed requires proportional selling across all holdings. This is price-insensitive, mechanical selling at precisely the worst time.

The math is straightforward: ETF selling → stock prices fall → more ETF redemptions → forced selling → prices fall further → repeat until intervention. Each step in the cycle is deterministic. There’s no discretion, no judgment, no ability to wait for better prices. The algorithms execute regardless of valuation.

Leverage amplifies these dynamics. Leveraged ETFs must maintain constant leverage ratios through daily rebalancing. A 2X leveraged ETF experiencing a 10% decline in underlying holdings must sell an additional 20% worth of positions to restore 2X leverage. This forced selling happens every day at market close - predictable, mechanical, and front-runnable.

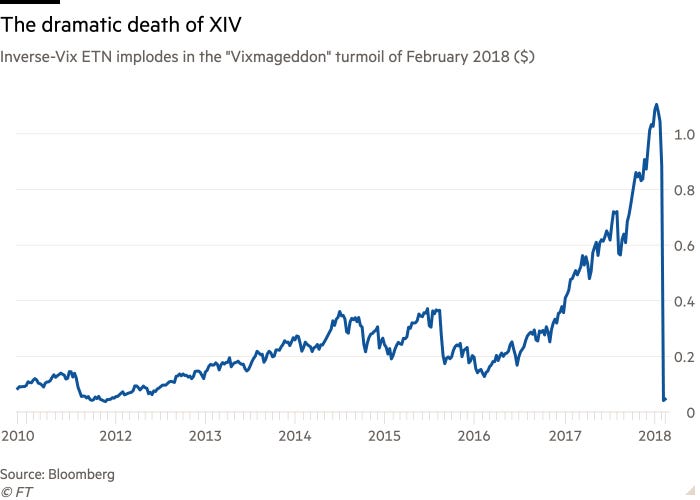

The February 5, 2018 “Volmageddon” demonstrated this perfectly. Inverse VIX products lost 97% of value when VIX spiked 115% in a single session. The products had to buy approximately $4 billion of VIX futures at 4:15 PM regardless of price to maintain their daily leverage targets. Sophisticated traders front-ran this predictable buying, pushing prices higher, forcing even more buying. Credit Suisse’s XIV collapsed from $1.9 billion AUM to $63 million overnight and was permanently liquidated.

Cross-asset contagion spreads through multiple channels. Synthetic ETFs using total return swaps present particularly dangerous vectors. BIS research documented ETFs tracking emerging market equities that were collateralized with Japanese stocks, German bonds, and U.S. corporate bonds - zero overlap with the EM index being tracked. When EM stress forces synthetic ETF liquidations, selling pressure hits Japanese equities and U.S. corporate bonds, creating contagion in completely unrelated markets.

March 2020 showed unprecedented correlation breakdowns. Stocks fell 34%, investment-grade bonds dropped 18.9%, high-yield lost 20% - all three declining simultaneously with similar magnitude. This historically anomalous behavior reflected ETF-driven contagion: stock ETF selling triggered risk-parity fund deleveraging, forcing bond sales, which triggered bond ETF redemptions, requiring more stock sales to rebalance portfolios.

The concentration of arbitrage providers transforms individual firm risk into systemic risk. With the top 3 APs handling 82% of fixed-income ETF creation/redemption, a single firm’s balance sheet problems cascade across the entire ETF ecosystem.

During March 2020, APs faced 5-27% arbitrage profit opportunities yet refused to engage because:

Regulatory capital constraints were binding. Basel III requirements limit leverage and dictate minimum capital ratios. During stress, these ratios bind, preventing additional positions regardless of profitability.

Balance sheet capacity was exhausted. Large banks had already warehoused massive inventories of the same securities everyone was dumping. They physically couldn’t take on more.

Inventory imbalances created directional risk. Bonds delivered in redemption baskets lost their most natural buyers as the institutions supposed to provide arbitrage became the most reluctant purchasers.

Research by Pan and Zeng modeled this “dual role conflict” mathematically. When large banks serve simultaneously as authorized participants, market makers in ETFs, and dealers in underlying securities, they face impossible choices during stress. Providing liquidity to the ETF market requires balance sheet capacity. Providing liquidity to the underlying bond market requires the same capacity. The optimal strategy during severe stress is to withdraw from both markets simultaneously - exactly what happened.

The same large banks that serve as APs also provide derivatives for synthetic ETFs and make markets in underlying securities. This creates network effects where stress propagates through multiple channels simultaneously: primary markets, secondary markets, and derivatives markets all failing in sync.

August 24, 2015 provided a preview of how cascading failures multiply. That morning, 1,278 stocks halted at the open following overnight volatility. ETFs continued trading without knowing underlying values. Market makers withdrew liquidity to avoid getting run over.

The result: 302 ETFs (19.2% of all ETFs) experienced trading halts. Large liquid funds like the Guggenheim S&P 500 Equal Weight ETF dropped 42% intraday - from $71 fair value to below $50. The iShares Select Dividend ETF plunged 35%. These crashes occurred in funds with billions in assets and five-star ratings.

Circuit breakers, designed to calm markets, often make ETF problems worse. When underlying stocks halt, ETFs can’t calculate accurate NAVs but continue trading anyway. Market makers face impossible choices: provide liquidity without knowing true values (risking catastrophic losses) or withdraw completely (allowing prices to gap arbitrarily). MIT research found that circuit breakers create a “magnet effect” where fear of imminent halts triggers aggressive preemptive selling.

The European Systemic Risk Board identified four main channels through which ETFs could contribute to systemic risk:

Increased volatility and co-movement in underlying securities

Decoupling of ETF prices from constituents that destabilizes institutions

Large correlated exposures causing contagion during sharp drops

Operational risk where single provider failure triggers system-wide fire sales

The Bank for International Settlements warned that ETF “capacity to bear risk while providing liquidity when there is sudden and large investor withdrawals is untested” and that funding liquidity risk “could reinforce funding stresses for financial system as a whole.”

The Federal Reserve’s March 2020 intervention was historic precisely because it represented explicit recognition that ETF markets are now systemically important infrastructure requiring central bank backstops. But Section 13(3) emergency powers are politically controversial and may not be available in future crises.

Here’s the fundamental problem: ETFs promise continuous liquidity by transforming illiquid underlying assets into tradeable shares. In normal times, this works flawlessly. But this is liquidity borrowed from the future - it works only as long as most investors don’t demand it simultaneously.

The secondary market (exchange trading) provides an illusion of infinite liquidity. You can buy or sell SPY instantly, any time markets are open, in huge size with tight spreads. This makes SPY appear more liquid than the 500 individual stocks it holds. But that liquidity is a mirage created by the assumption that the creation/redemption mechanism will arbitrage any gaps.

When institutional investors holding 50-80% of ETF assets rush for exits together, the “theater exit door” becomes a bottleneck. Market makers step away. APs refuse arbitrage despite huge profits. The promised transformation of illiquid into liquid reverses catastrophically into amplified illiquidity.

Academic research documents systematic increases in volatility, reduced diversification, degraded price discovery, and heightened tail risks associated with passive ownership concentration. These effects become dramatically stronger during crisis periods.

The crash scenarios range from gradual mean-reversion to violent liquidation to rolling crisis. March 2020 provided a preview: bond ETFs at 6-8% discounts, requiring unprecedented Fed intervention. Without that backstop, research suggests discounts would have reached 40-50% with cascading institutional failures.

Let’s be clear about what we know:

The passive revolution has created a fundamentally different market structure. One that functions efficiently during calm periods but contains powerful destabilizing mechanisms during stress. The concentration is worse now than in March 2020: over 50% passive share, Big 3 dominance at 71-90%, top 10 stocks at 40% of S&P 500.

The arbitrage mechanism that maintains ETF pricing is fragile, dependent on a handful of authorized participants with limited balance sheets and conflicting roles. March 2020 demonstrated this wasn’t theoretical - despite 5-27% arbitrage profits, APs refused to engage. Only Federal Reserve intervention prevented complete collapse.

The feedback loops amplify rather than dampen volatility. Selling begets more selling in an inescapable spiral until external intervention breaks the cycle. Leveraged products mechanically amplify moves. Cross-asset contagion spreads through synthetic ETF collateral and correlation spikes.

The mechanics of breakdown are well-understood and documented. What remains uncertain is only timing - when those mechanics activate, and how devastating the spiral becomes before external forces intervene.

Bank of America’s February 2025 assessment detailed that at a 54% market share, passive has reached “critical mass” where “passive disregard for valuations & fundamentals” creates “big risk in a bust cycle.”

My fairy tale had a happy ending.

Everyone learned their lesson.

Everyone agreed to be more careful.

Reality however is a LOT messier.

The machine got bigger. The concentration increased. The structural fragilities remain.

And the next time everyone rushes for the exit simultaneously, the arbitrage fairies might not come back - no matter what the Federal Reserve promises.

Great breakdown on passive investing—especially the ETF angle. And thank you for the shoutout; I'm glad our exchange prompted you to explore it further.

I first started paying close attention to the passive-investment paradox through Michael Green. Here’s a short CNBC clip for anyone who hasn’t come across his work: https://youtu.be/iRf5l8S6UII

He barely scratches the surface there, but his longer interviews are well worth digging into.

The real issue goes far beyond ETF mechanics (helpful as the arbitrage mechanism is) and gets into the enormous, automatic flows pouring into retirement accounts. Most retirement plans direct contributions into qualified index funds or benchmark-matching mutual funds—essentially accomplishing the same thing ETFs do, but on a much larger, more institutional scale.

Years ago, the market had a healthier balance. Sell-side analysts and short-biased hedge funds helped check excesses the same way ETF arbitrage was designed to support price discovery. But as Michael Burry’s experience illustrates, anyone trying to flag distortions—in individual stocks, sectors, or even entire indices—gets run over by the relentless, calendar-driven wave of passive inflows. Fundamentals take a back seat to flows, and even correct positions become career-risking.

As more of those players step aside, the dynamics shift. Forced selling becomes more violent because there are fewer active buyers ready to absorb it. And when markets bounce from oversold conditions, there are far fewer shorts to cover and drive the rebound.

Once you widen the lens to include automatic retirement flows, the picture looks far more consequential than focusing on ETFs alone. ETFs matter, but the retirement-system plumbing dwarfs them in both scale and impact. Just when you thought it couldn't get any worse. :-)

Another masterful article, NO1.

Everything you put out is solid gold or equivalent in silver. 😂

The inevitable deliberate economic implosion will lay the foundation for the great economic reset. The multi-pronged social, political, economical, and health assault on humanity is well underway. Oddly, I envisioned and started preparing for such a calamity just after 9/11. It all ties in, orchestrated and planned. Sure, I digress, but the vision is so clear to me, the nefarious design of the few who hide behind the wall, fostering confluenced events leading up to the great taking. Prepare accordingly.