I was composing another article (which will be published soon) when this popped up in my newsfeed. As many of you know, I’m kinda liking silver and gold, and have a disdain for Bitcoin.

Now this is something that most BTC HODLers will lose a lot of sleep over.

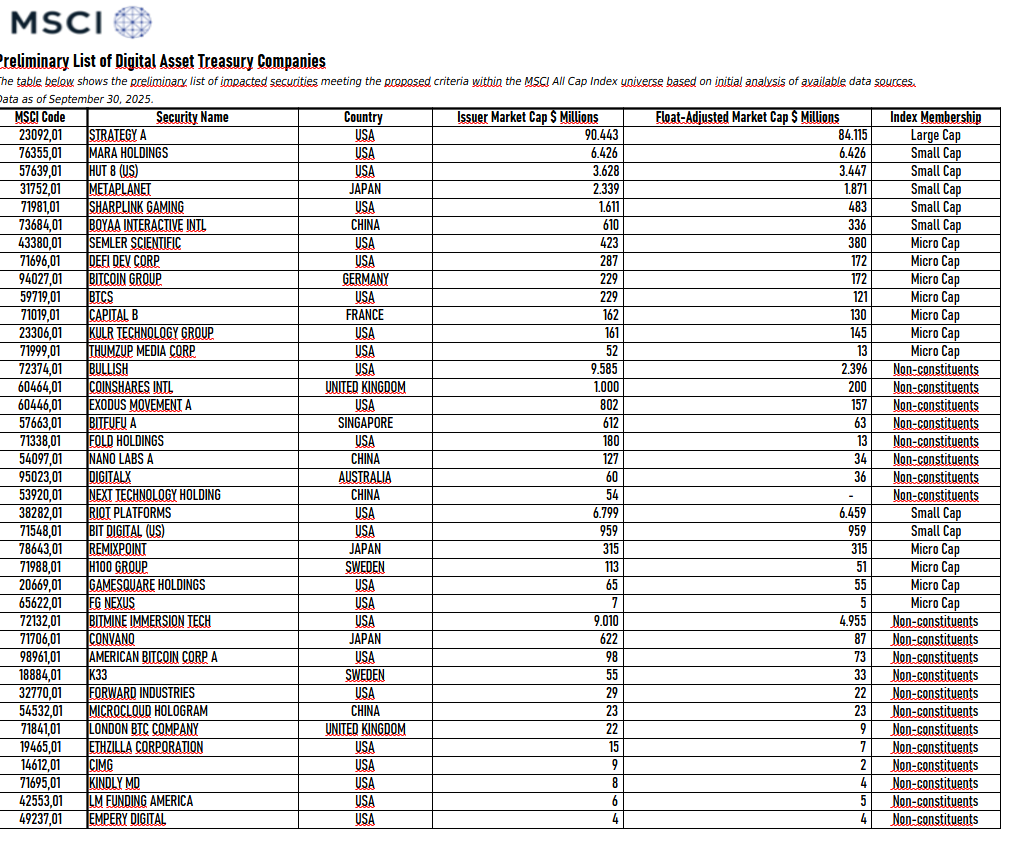

You know MSCI right? Those people who decide what belongs in equity indexes and what doesn’t. Well, they launched a consultation in October about “digital asset treasury companies.” Nobody noticed because consultations are boring. Index methodology documents don’t make headlines.

Then JPMorgan published a note that put actual numbers on the carnage.

The proposal is brutally simple. If your balance sheet is more than 50% Bitcoin, you’re not an operating company. You’re an investment fund. And investment funds don’t belong in equity indexes.

MicroStrategy sits at 77-81% Bitcoin holdings.

The consultation ends December 31. The ruling drops January 15.

JPMorgan estimates $2.8 billion in forced selling from MSCI exclusion alone. Potentially $8.8 billion if other index providers follow. The company’s market cap is $59 billion with about $9 billion held by passive index funds that must mechanically replicate whatever the indexes say.

Here’s where it gets brutal for anyone who believed the story.

The reflexivity loop is already dead. MicroStrategy’s premium to net asset value collapsed from 2.5x to 1.11x a few days ago. (premium is now 1.20 due to BTC’s continued crash) Markets front-run these things. The stock now trades barely above the value of the Bitcoin it holds.

Remember when I wrote about Saylor’s leveraged perpetual motion machine? Issue equity at premium valuations, buy Bitcoin, watch premium expand, issue more equity at even higher premiums. That cycle extracted $15-20 billion in excess capital that wouldn’t have existed if the stock traded at net asset value.

If this passes, it’s over.

At the current premiums you can’t generate meaningful accretion through additional equity issuance. The mathematics don’t work. Issue new shares to buy Bitcoin and you neither create nor destroy value for existing shareholders.

But what breaks my heart about this whole situation is the retail investors who bought into this story. They were sold a narrative that sounded reasonable: institutional adoption, ETF legitimacy, Bitcoin as corporate treasury strategy, Michael Saylor as visionary. The pitch made sense if you didn’t look too closely at the mechanics underneath.

Read the link above about the deleveraging spiral that is hitting Bitcoin. The Fed reversed course on rates. Real yields stayed above 5%. Japan’s interest rate makes the carry trade unwind. Institutions exited through those shiny new ETFs everyone celebrated. Long-term holders took profits. Leverage cascaded. Billions in borrowed money evaporated.

The MSCI consultation just became another accelerant on that fire.

Because now you’ve got a specific date - January 15 - where MicroStrategy faces potential forced selling of up to $8.8 billion. That’s not theoretical anymore. That’s mechanical. Passive funds don’t have a choice. When MSCI says sell, they sell.

The thesis I laid out about Bitcoin’s collapse just got more likely. You’ve got macro working against it (see above), you’ve got leverage unwinding, you’ve got long-term holders distributing, and now you’ve got index exclusion triggering institutional forced selling.

Each piece amplifies the others.

MSCI isn’t being punitive here. They’re being accurate.

When 77% of your assets are Bitcoin and your software business generates $116 million in quarterly revenue while your Bitcoin holdings swing by $8.4 billion in the same period, you’re not a software company. You’re a leveraged Bitcoin vehicle cosplaying as an operating business.

The consultation document specifically mentions the 50% threshold. Cross that line and you get reclassified. Tesla holds $800 million in Bitcoin. Block holds $300 million. They’re fine. Under the threshold. Actually operating companies that happen to hold some Bitcoin.

MicroStrategy is a Bitcoin holding that happen to operate some software on the side.

Charlie Sherry from BTC Markets told Cointelegraph the odds of MSCI excluding these companies are “solidly in favour of it” because “they only put changes like this into consultation when they’re already leaning that way.”

Translation: The consultation is theater. The decision is made. They’re just checking procedural boxes.

38 companies are on MSCI’s preliminary list. Strategy, MARA Holdings, Metaplanet, Riot Platforms, Marathon Digital. Every company that thought they could build a business model around accumulating Bitcoin and calling it an operating company.

The five-year experiment ends not with regulatory prohibition or technological failure, but with index methodology. The most boring document in finance.

The most powerful.

They launched this consultation right as Bitcoin started cracking from $126k in October. MicroStrategy’s stock fell harder than the underlying asset. Same reflexivity loop that powered five years of gains, just running in reverse. Premium collapses, forced selling hits, liquidity dries up.

And we know when the next wave will hit. January 15. Not theoretical anymore. Mechanical. Passive funds don’t choose. When MSCI says sell, they sell.

You know what MSCI is really saying? “We’re not going to help you pretend anymore.”

That’s what this was. Pretending that buying Bitcoin is the same as running a business. Pretending that balance sheet speculation deserves the same treatment as companies that make things, sell things, employ people, generate cash flow.

The software business MicroStrategy still technically operates? Down 10% year-over-year. 2,000 enterprise customers. Stable but stagnant. CEO Michael Saylor explicitly stated in investor presentations that the software business exists primarily to provide cash flow to service debt and regulatory legitimacy for public market access.

When management tells you the operating business is secondary to treasury management, why should index providers pretend otherwise?

And look, I get it. If you’re holding MicroStrategy right now, you’re watching your investment implode in real-time. The premium you paid for “exposure to Bitcoin with institutional legitimacy” is evaporating. The whole thesis about Bitcoin going to $1 million per coin and Saylor being a genius is collapsing under the weight of actual market mechanics.

This is what happens when you build a strategy on perpetual asset appreciation. It works until it doesn’t. And when it stops working, it doesn’t just plateau - it reverses violently.

The MSCI ruling is not creating this crisis. It’s just another drop in the already overflowing bucket.

MicroStrategy’s average cost basis is $74,433 across 650k Bitcoin. A 15% decline from here pushes the entire position underwater. Not just recent purchases.

Everything.

If you’re holding this right now, I’m not here to mock you. The story was compelling. Institutional adoption, ETF legitimacy, Bitcoin as corporate treasury strategy. It made sense if you didn’t look too closely at the mechanics underneath.

But markets don’t care about narratives. They care about cash flows and valuations. And leverage is a multiplier - it amplifies gains on the way up, amplifies losses on the way down. Right now we’re on the way down in a macro environment where real yields are above 5%, the Fed isn’t cutting, and $2.8-8.8 billion in forced selling is about to hit.

The bottom comes when leverage clears and price discovery happens at levels that make value buyers interested again. That might be $60k Bitcoin. Might be $40k. Might be lower.

disclaimer: I’m holding long term MSTR PUT options (= a bet that this company will go down)

If you wrote seven essays a day I would read every single one of them. Thanks !!!

Excellent forensic analysis. I noted the Jan. 15 deadline.