Weekend thoughts

No penny for my thoughts

This is a weekly digest of unassociated pictures (graphs mostly) I saw during the week. Not much context is given.

For daily digests: https://no1sdailydigest.substack.com/archive

Gold overtakes Treasuries as a share of central-bank reserves (~$5T):

Central banks bought 15x more gold than reported — 244t vs 16t official:

Gold +25% vs 'digital gold' bitcoin -43% over 12 months:

Gold ETF outflows: $12B since February, biggest 4-month exit in 13 years 📉

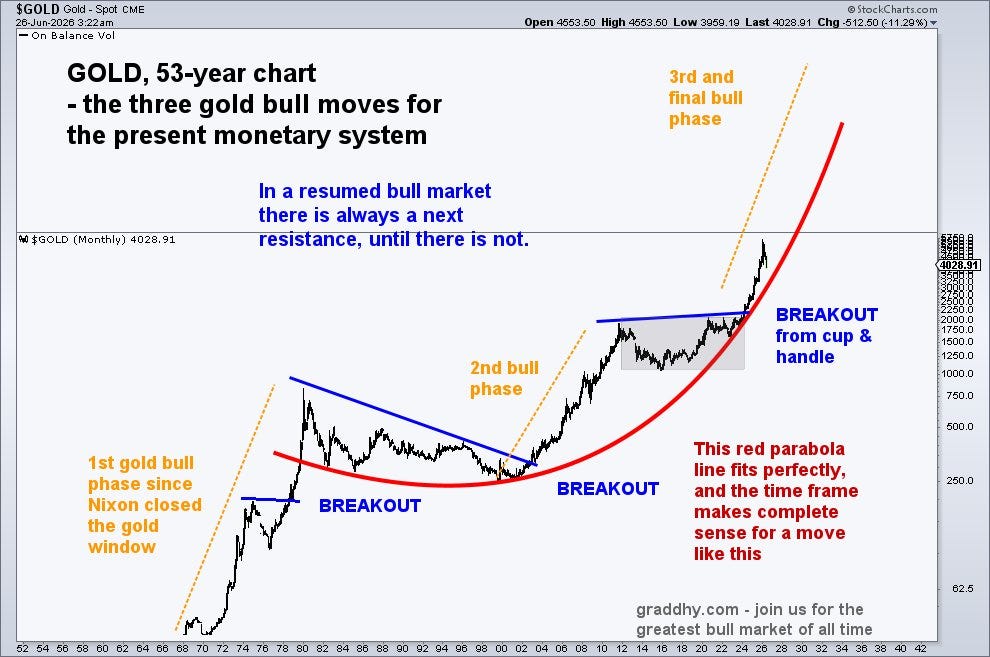

Gold's 53-year chart: three bull phases since Nixon shut the gold window:

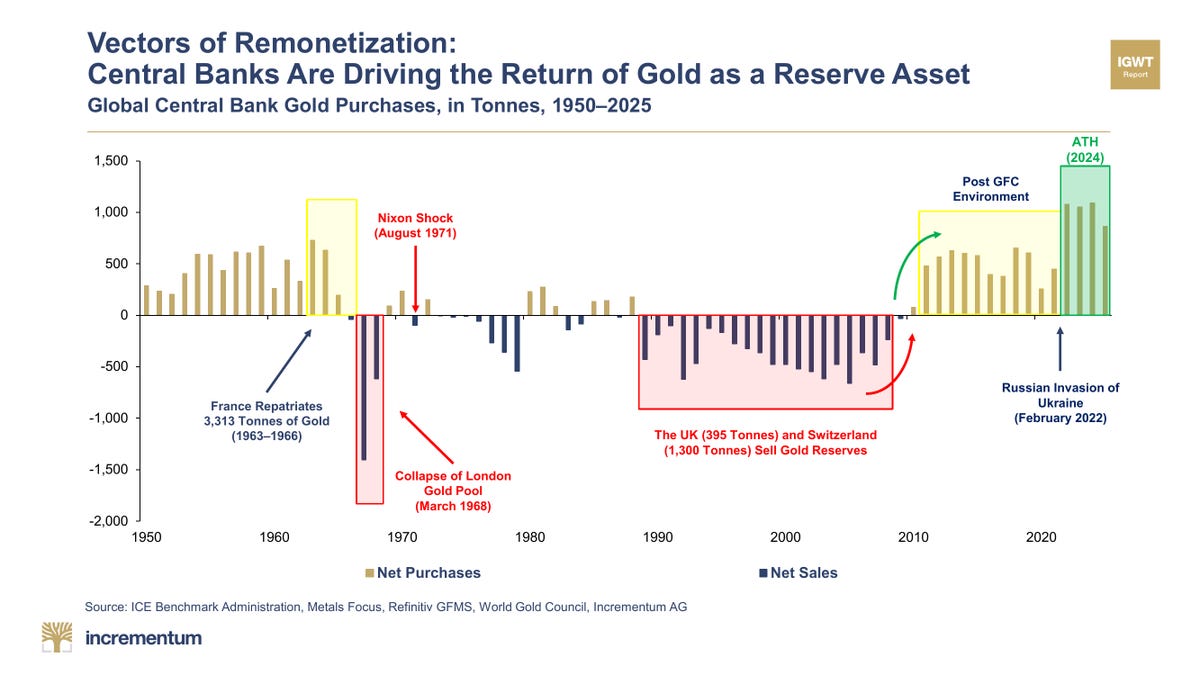

Central bank gold purchases, 1950-2025:

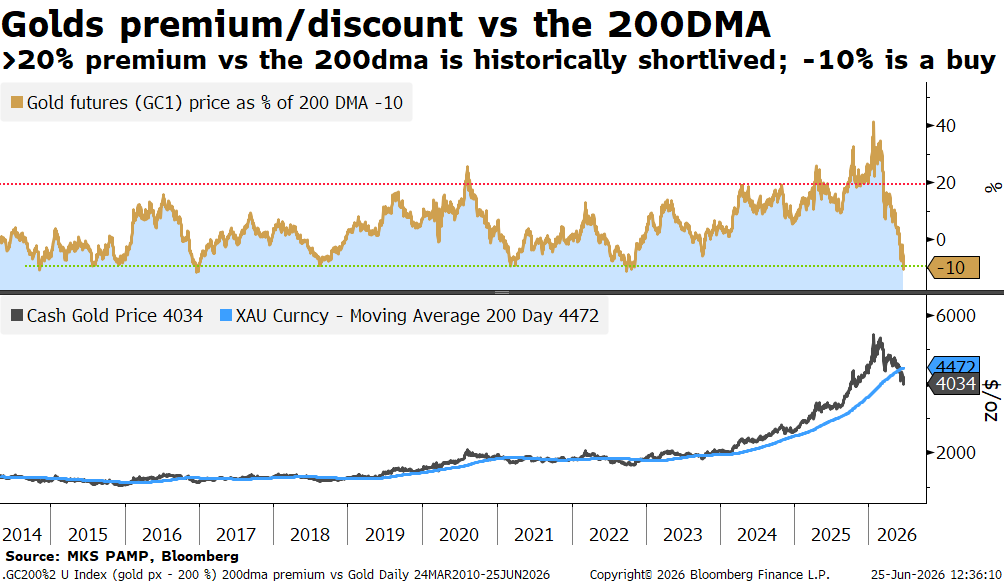

Gold at a 10% discount to its 200-day MA — historically a buy:

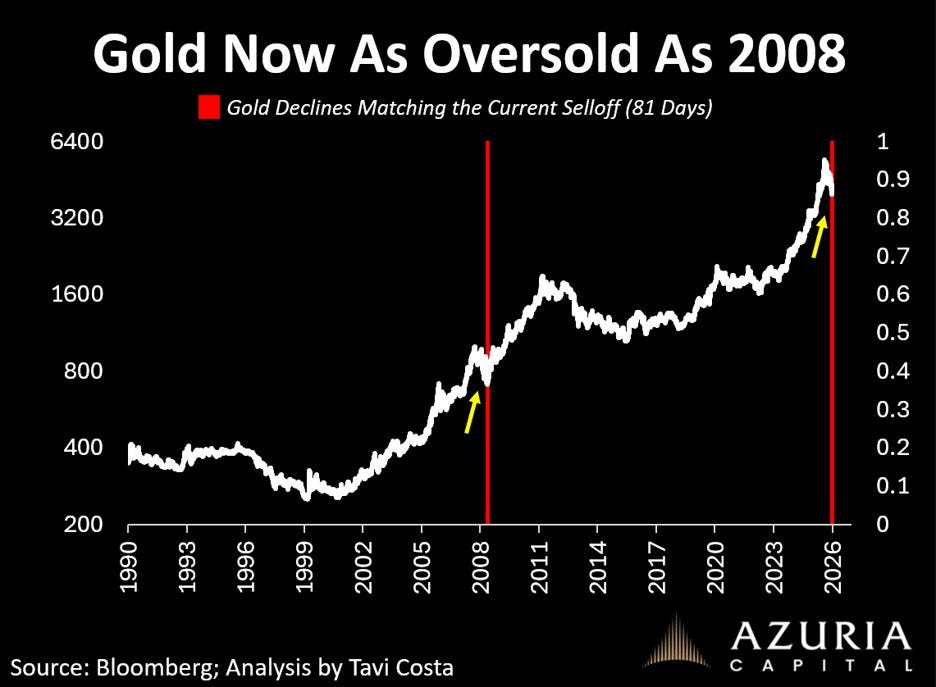

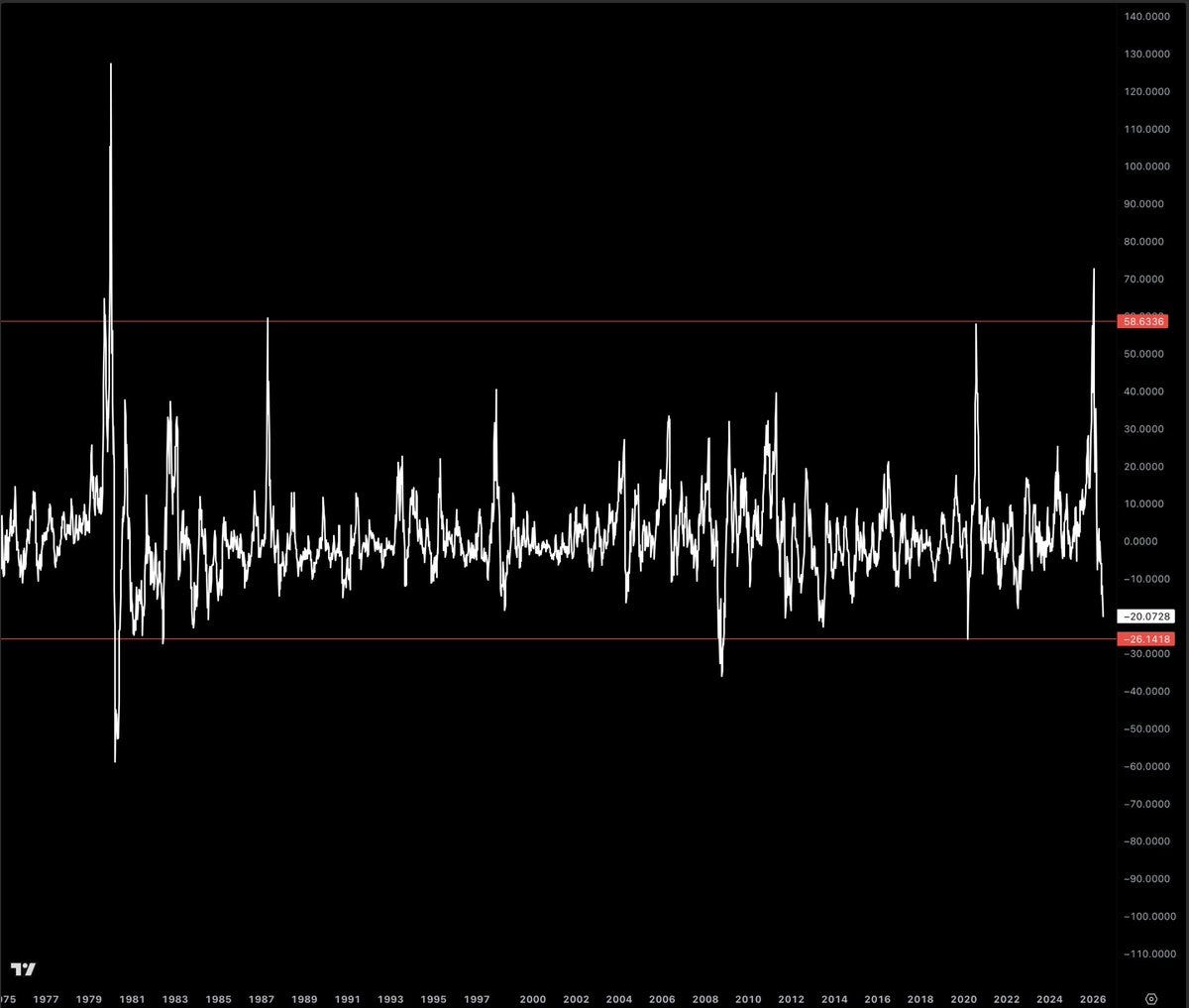

Gold now as oversold as 2008 — an 81-day selloff:

Spot gold below $4,000 vs inverted dollar, Fed funds futures & ETF holdings:

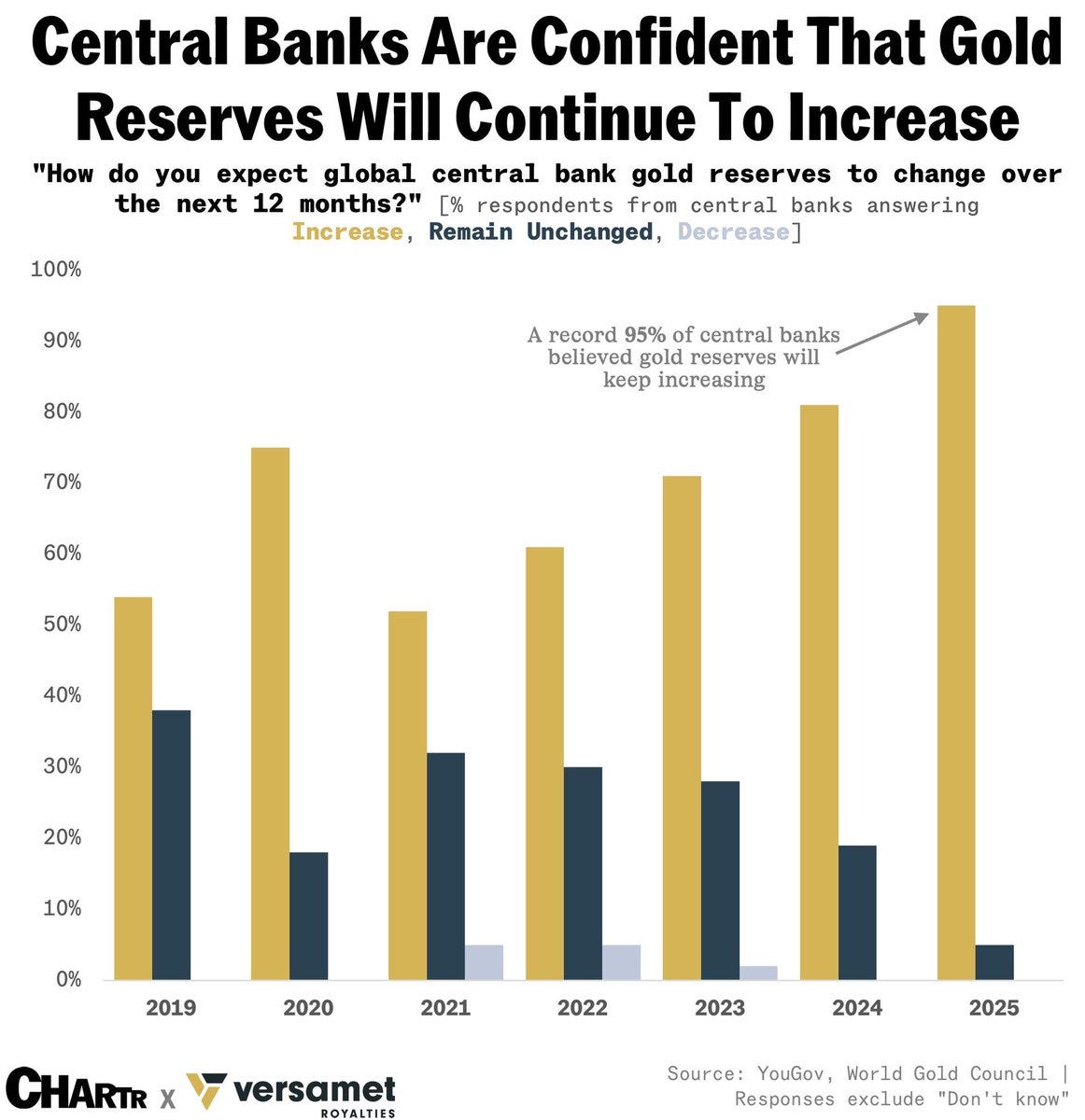

Central banks expecting gold reserves to keep rising (record 95%):

China's gold imports: 162.67 tonnes in May:

Gold $GLD on the brink of a death cross, first since October 2023:

Silver mining cost $12.21/oz vs $58 spot — miners printing money 🤑:

Silver has been here only four times since 1975:

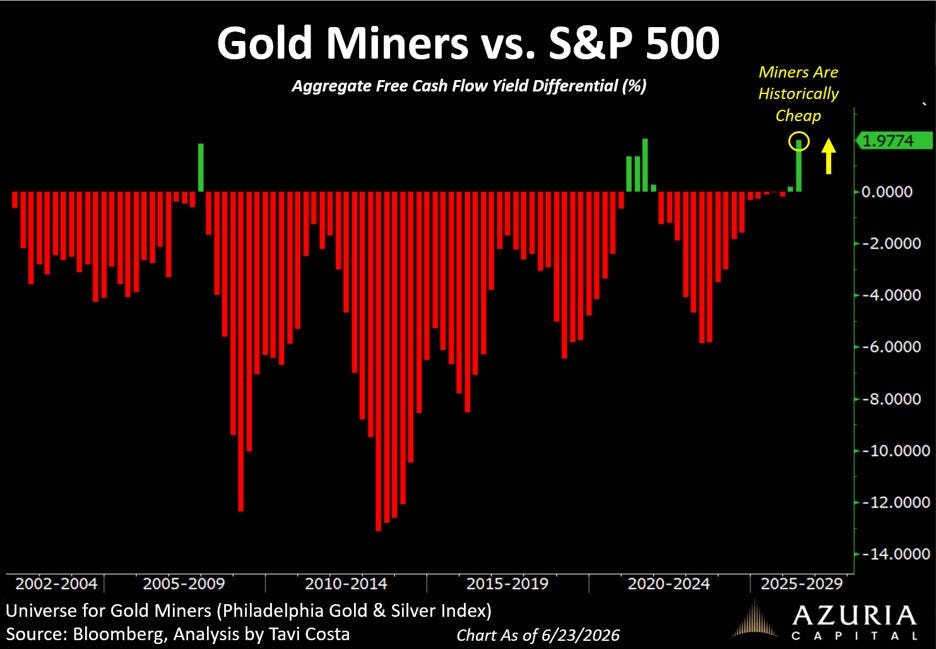

Gold miners' free-cash-flow yield vs S&P 500 — historically cheap:

US debt priced in silver: 604.79B oz, bouncing off the 1980-2011 trendline:

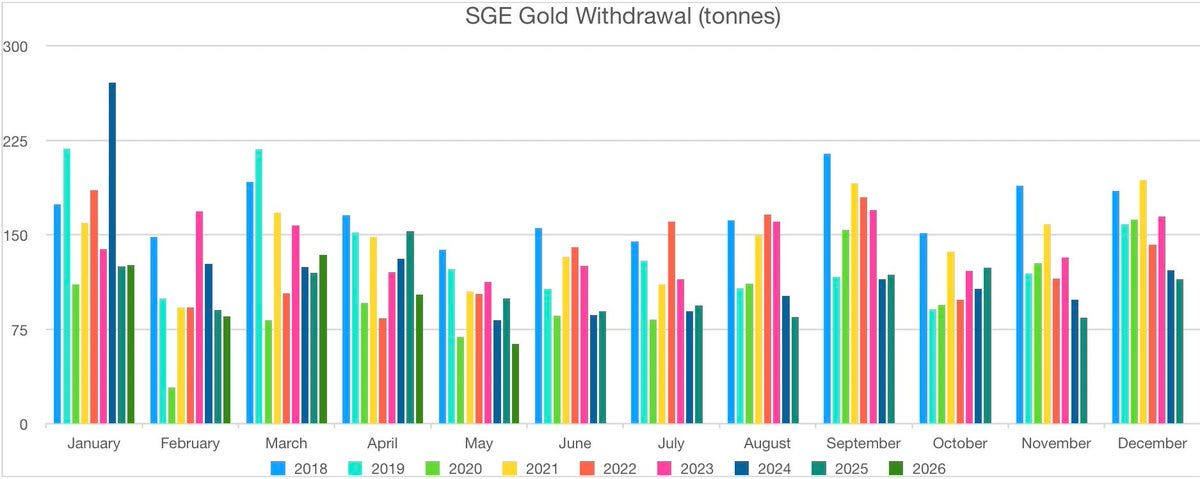

China SGE gold withdrawals by month (lowest since Feb 2020):

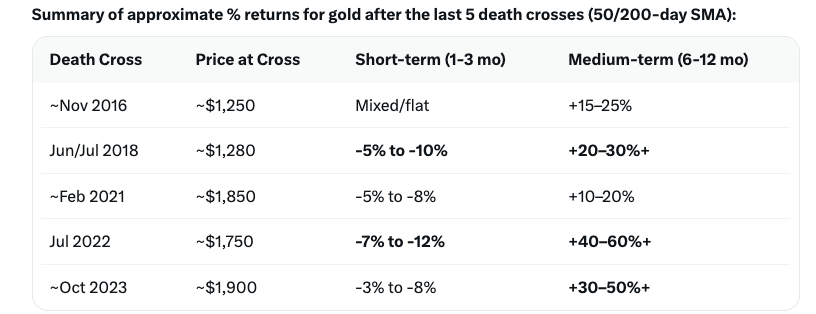

Gold's path after the last 5 death crosses: short dip, then +15-60% in 6-12mo:

Gold post-major-breakout corrections: 1973 vs 2006 vs 2026:

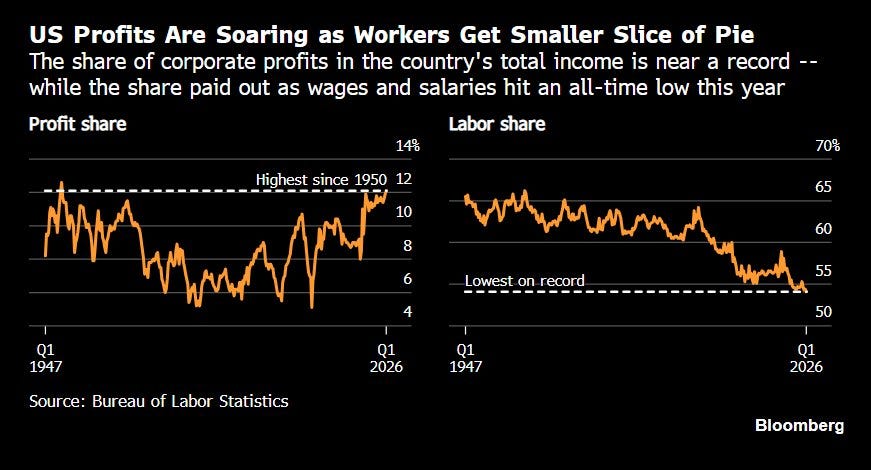

K-shaped economy: corporate profit share near record, labor share at an all-time low:

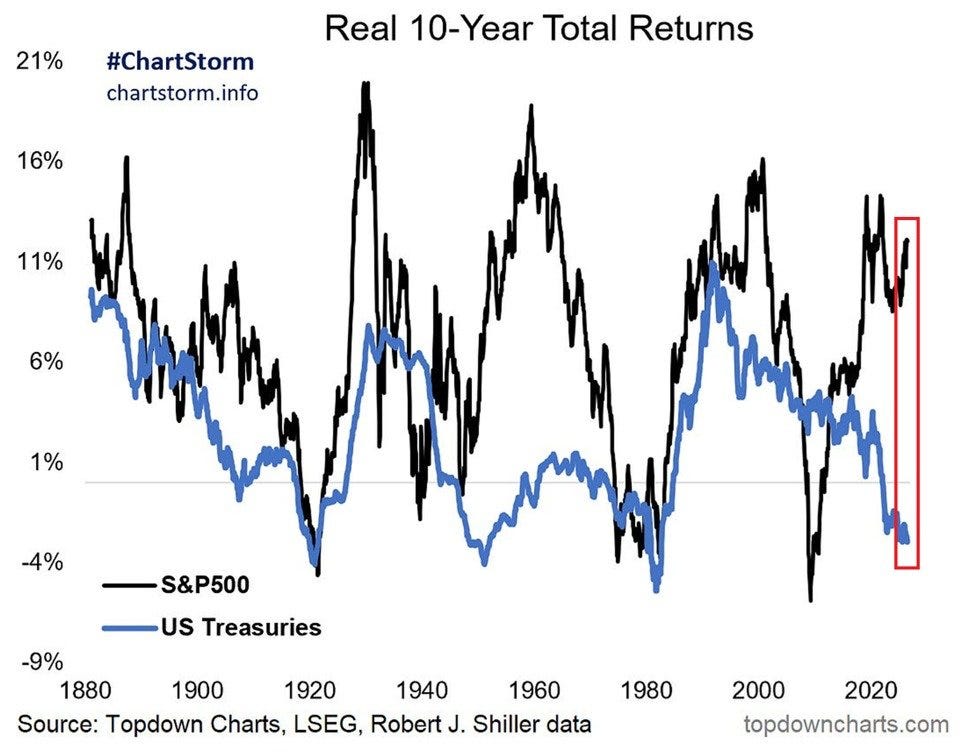

Real 10-year Treasury returns at -3%, worst since the 1980s:

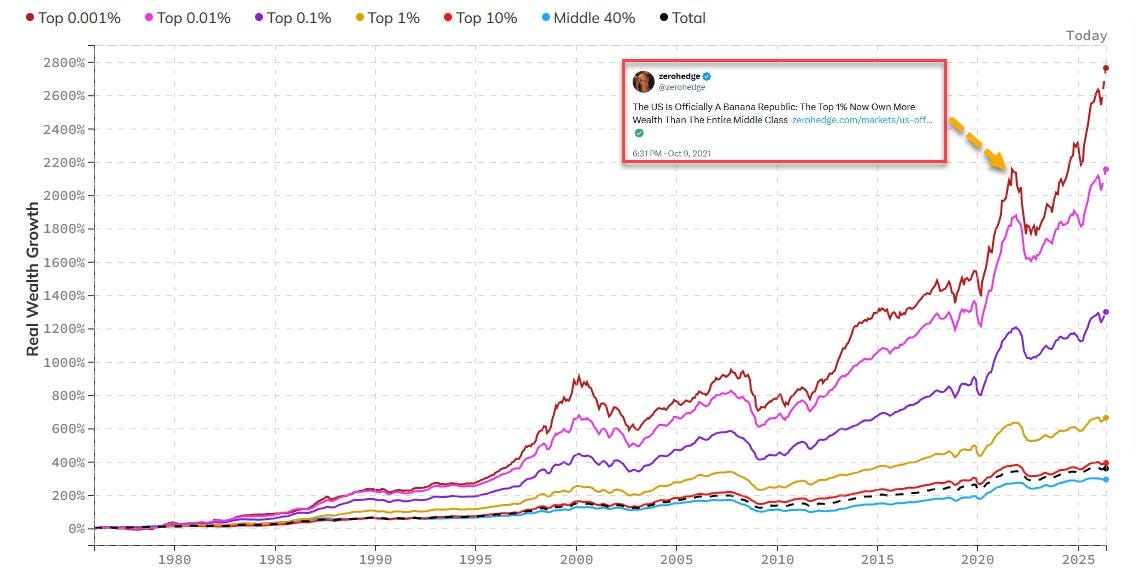

US real wealth growth: Top 0.001% +2,800%:

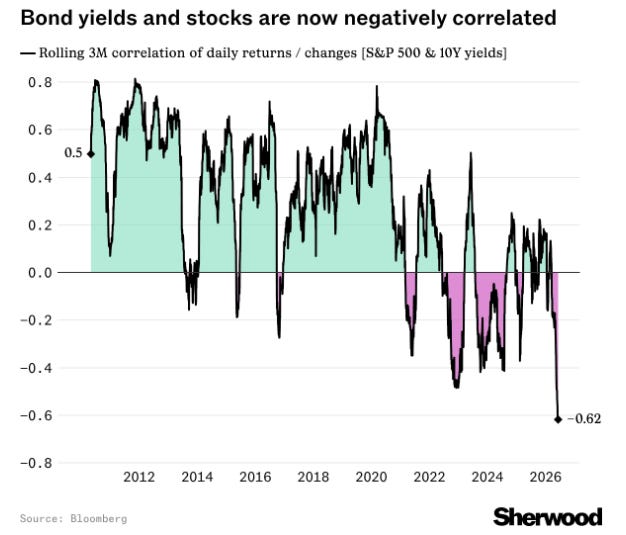

Stocks & 10Y yields most negatively correlated in 16 years (-0.62):

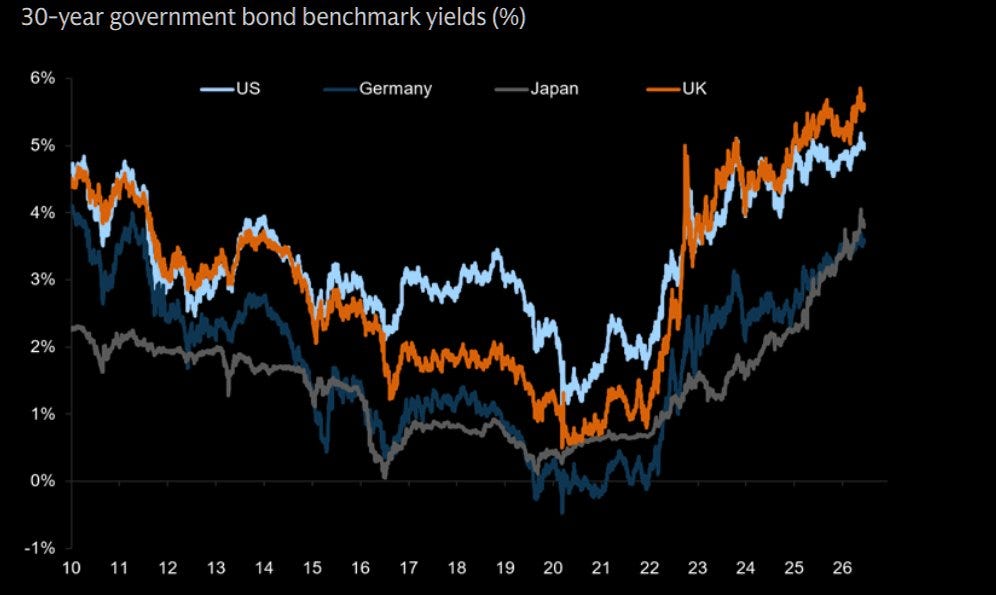

30-year government yields, US/Germany/Japan/UK — from ~zero to nearly 4%:

10-2 yield curve peaked exactly as metals topped:

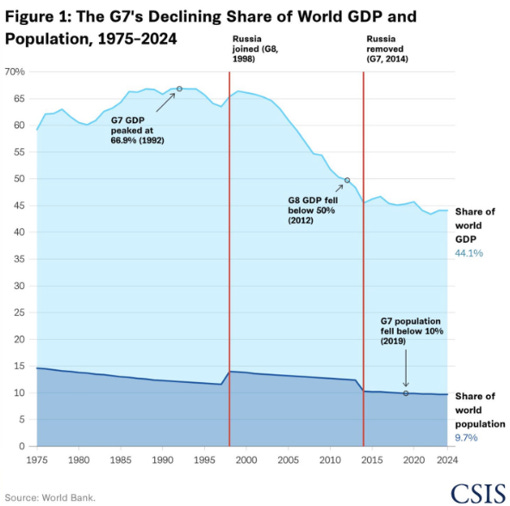

G7 share of world GDP: 60.5% (1980) → 44.1% (2024):

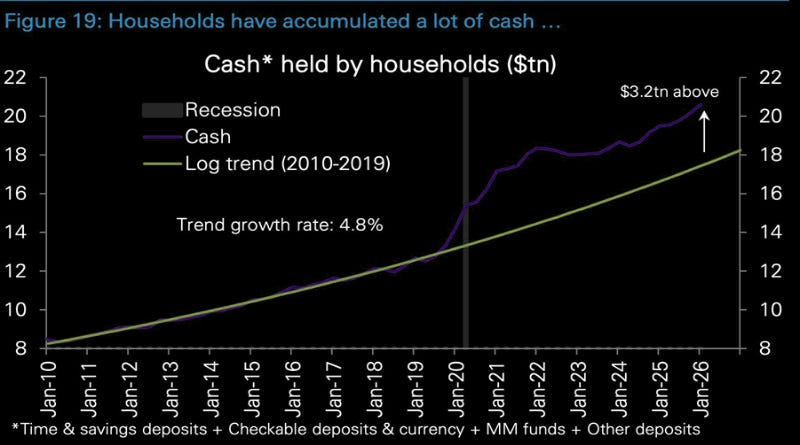

US households sitting on $3.2tn cash above trend:

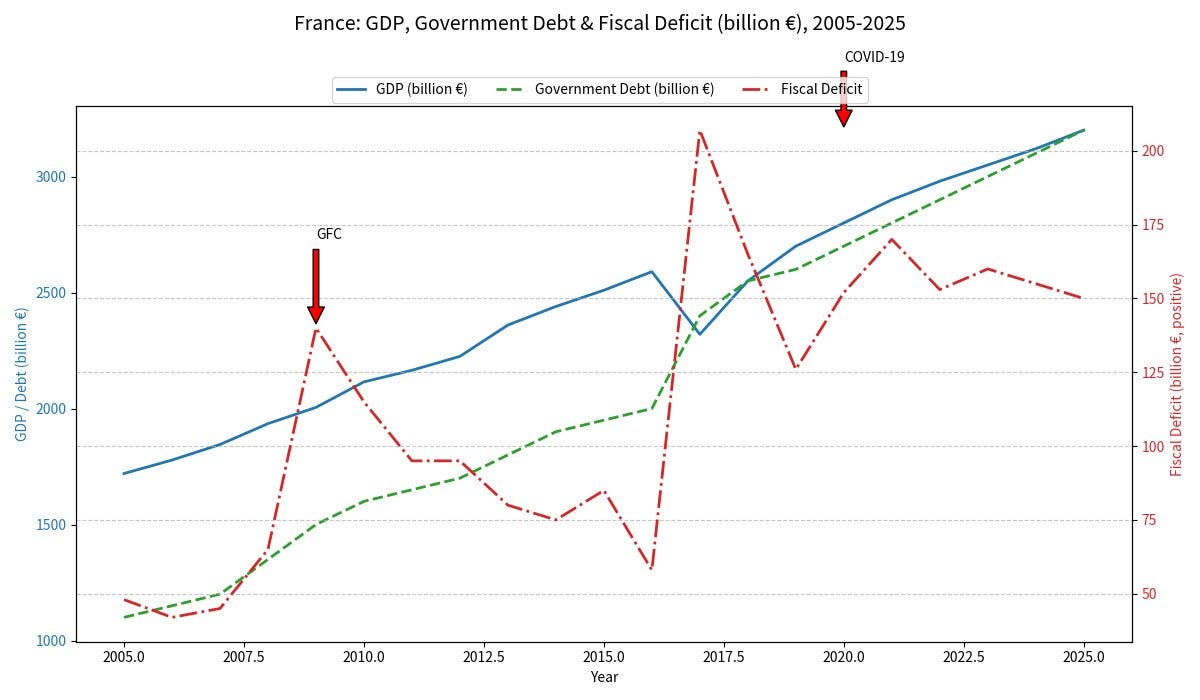

France GDP, government debt & fiscal deficit, 2005-2025:

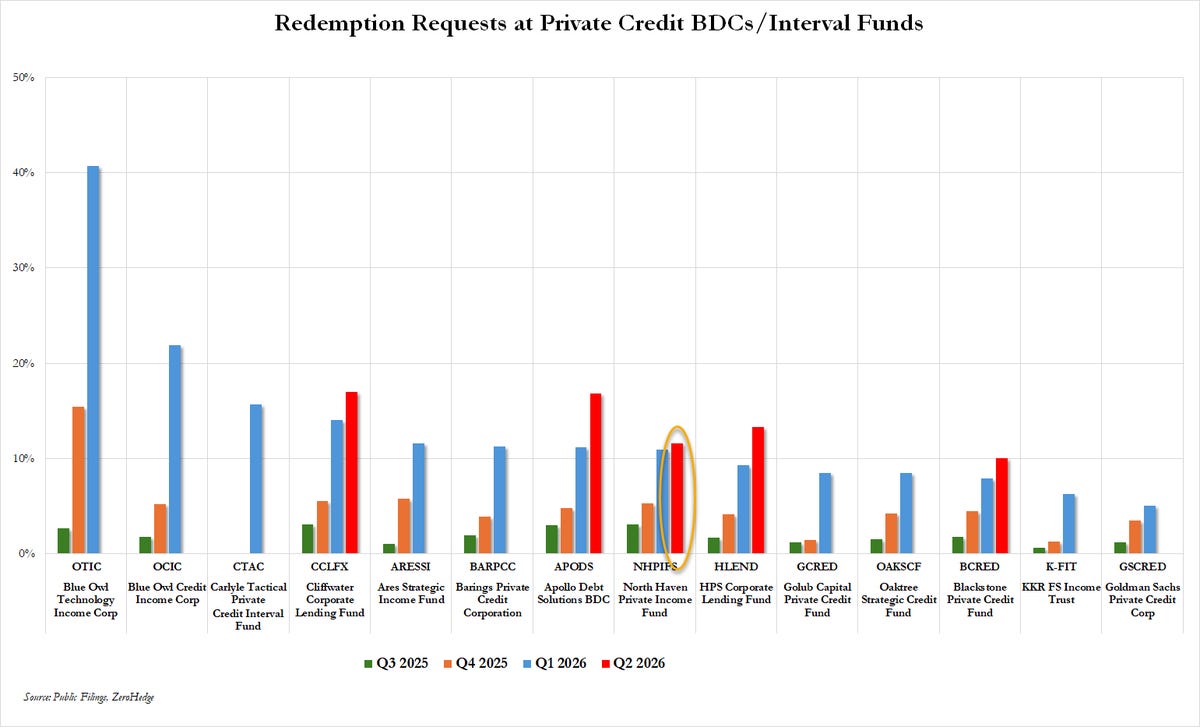

Private credit redemption requests surging — one BDC gated at 11.6%:

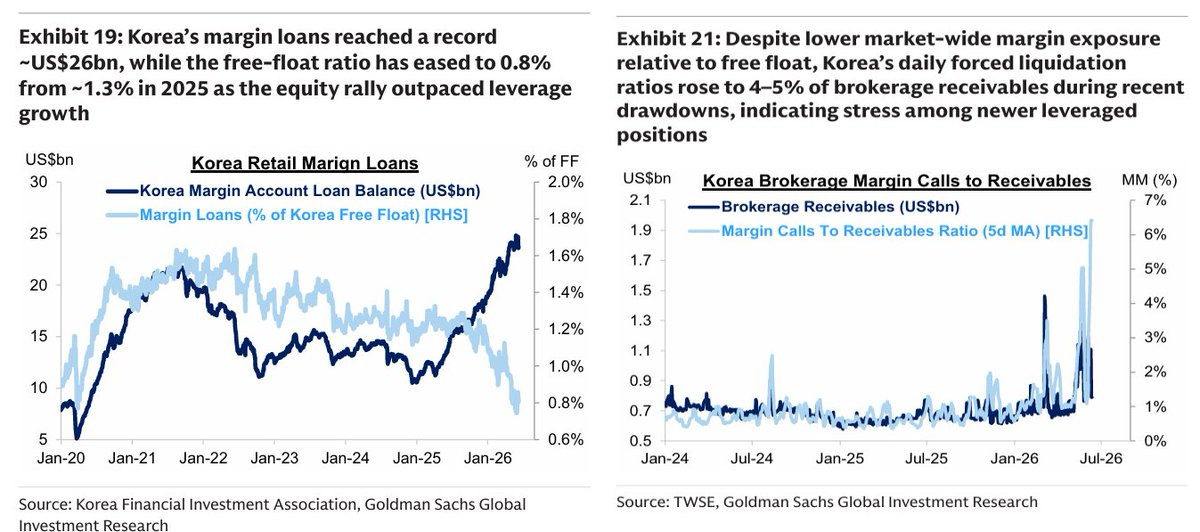

Korea retail margin loans at a record ~$26bn, forced liquidations spiking:

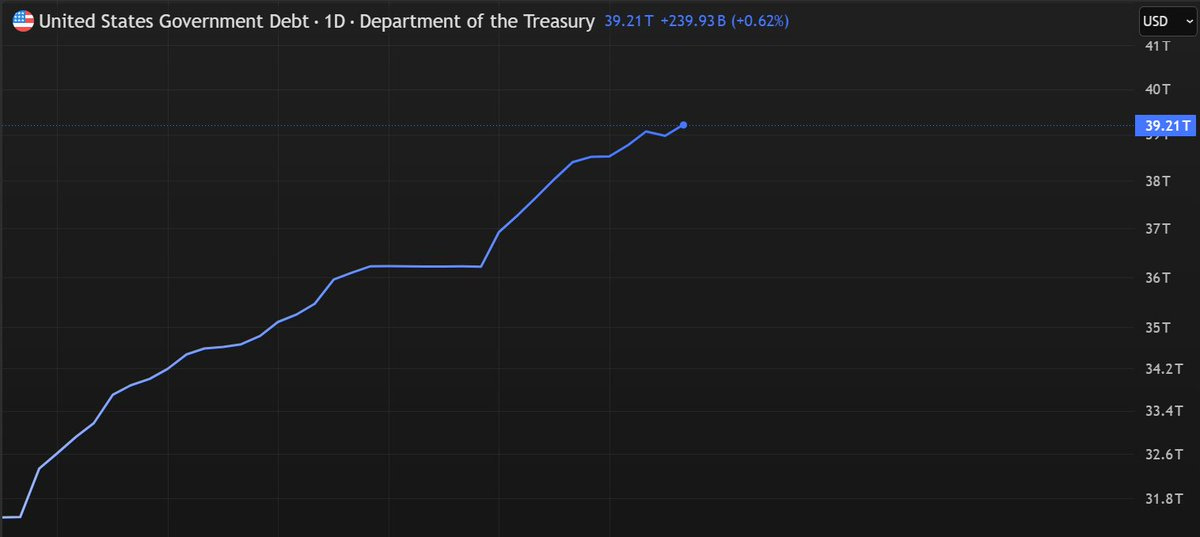

US government debt $39.2T, +$240B in a day:

Excess liquidity goes negative, first time since 2021:

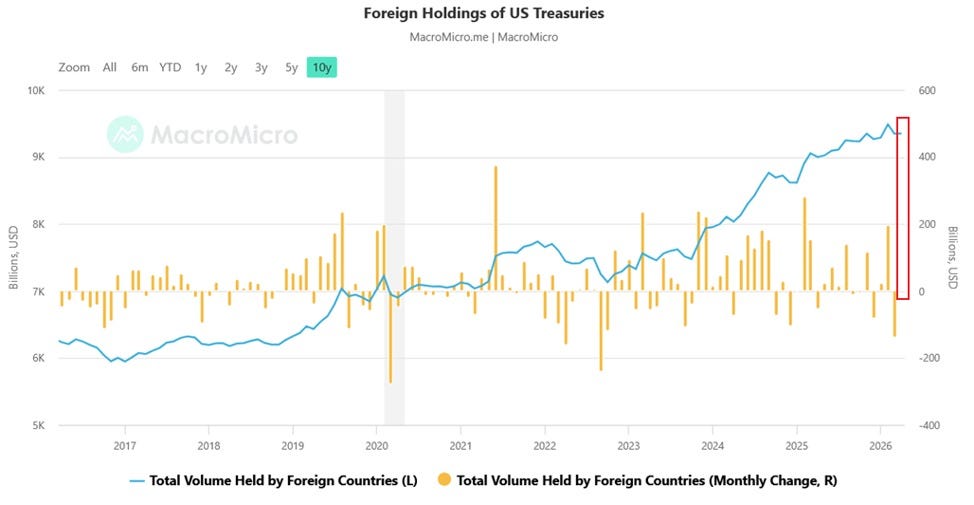

Foreign holdings of US Treasuries near record $9.35T:

Strait of Hormuz vessel crossings collapse vs Brent:

German power prices surged >€700/MWh on collapsing wind despite record solar:

Crude WTI below its 200-day MA for 4 straight days, first since January:

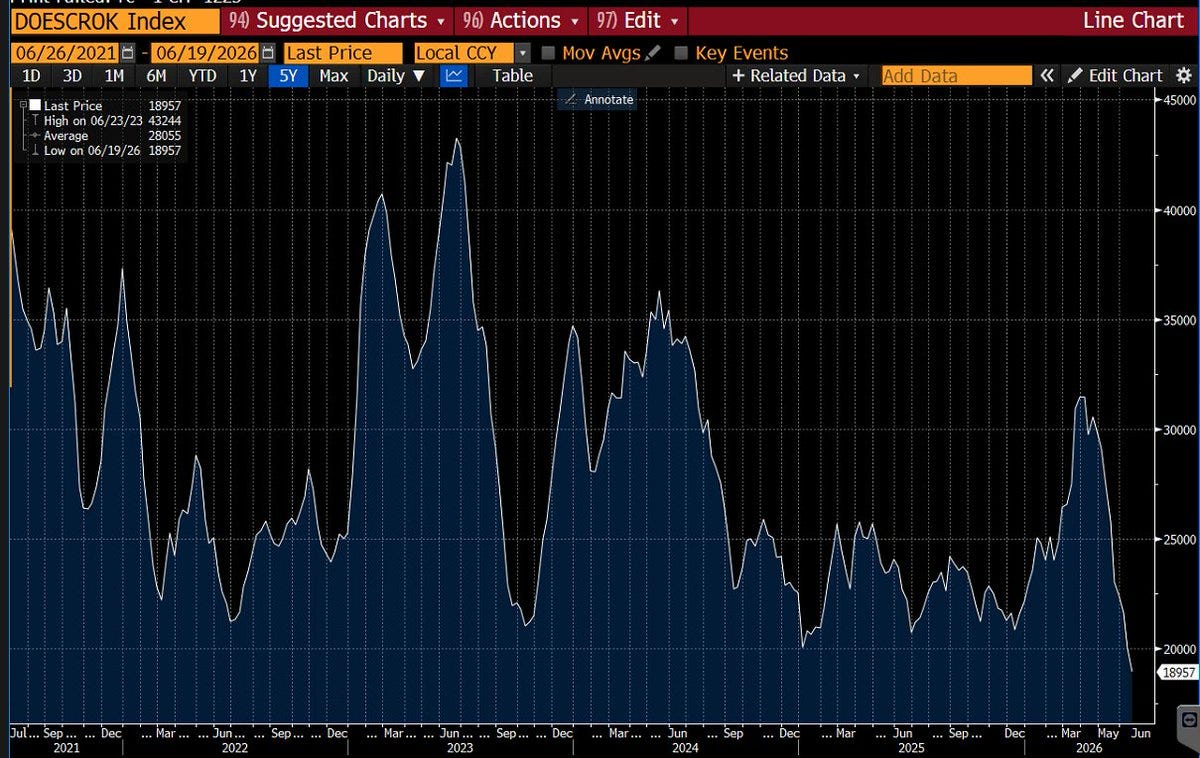

Cushing crude inventories at tank bottom (18,957):

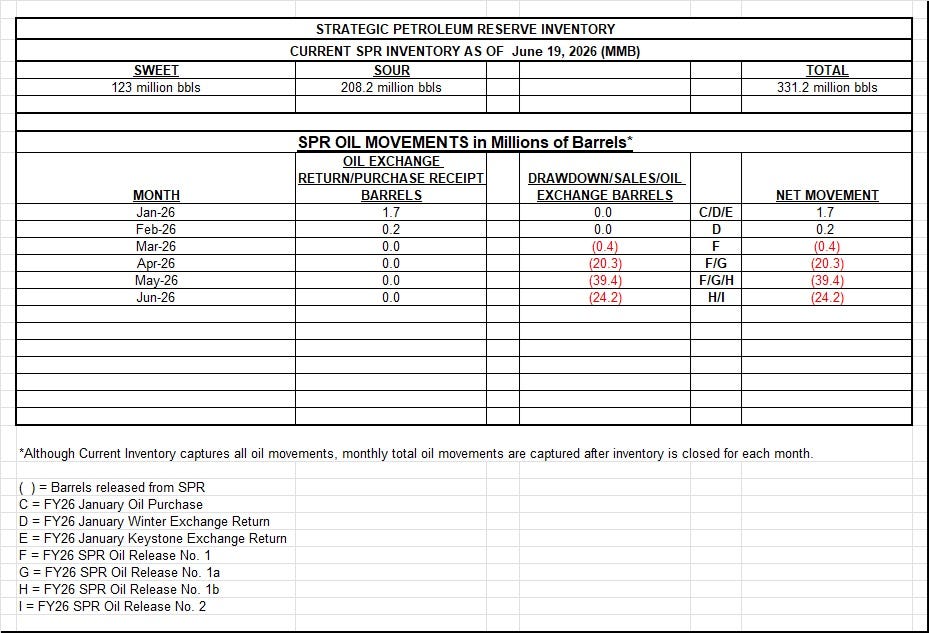

US SPR crude stocks down to 331.2mb, lowest since 1983:

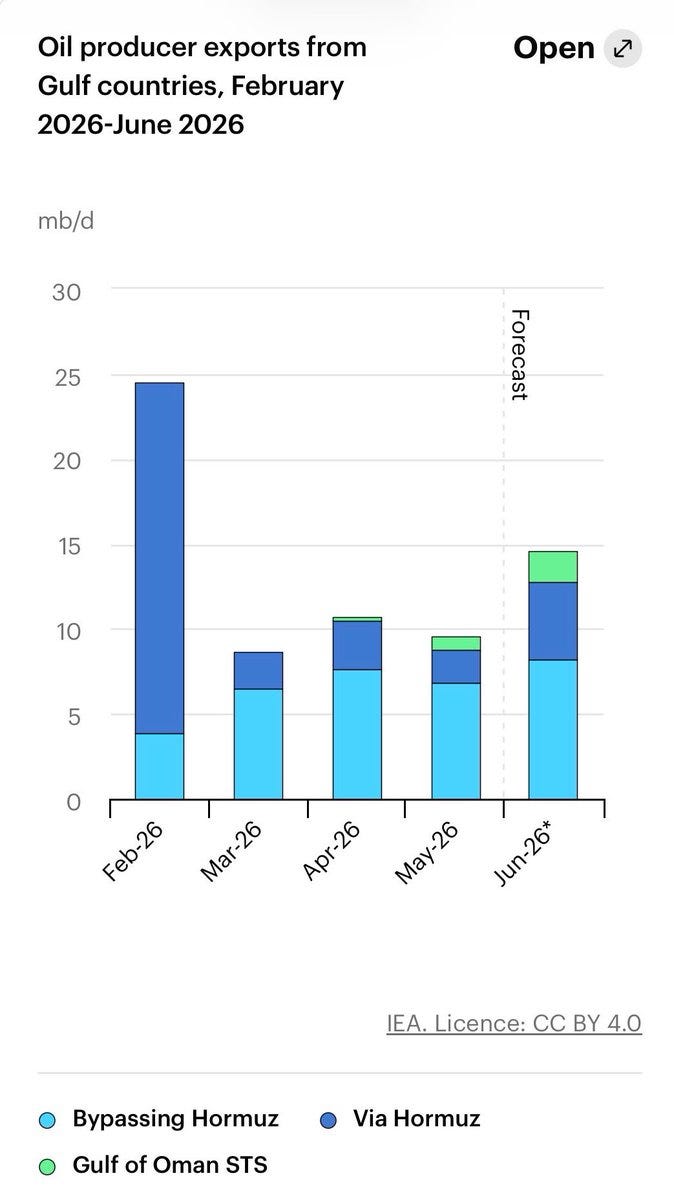

Gulf oil exports recovering, UAE bypassing Hormuz to 4.3m b/d:

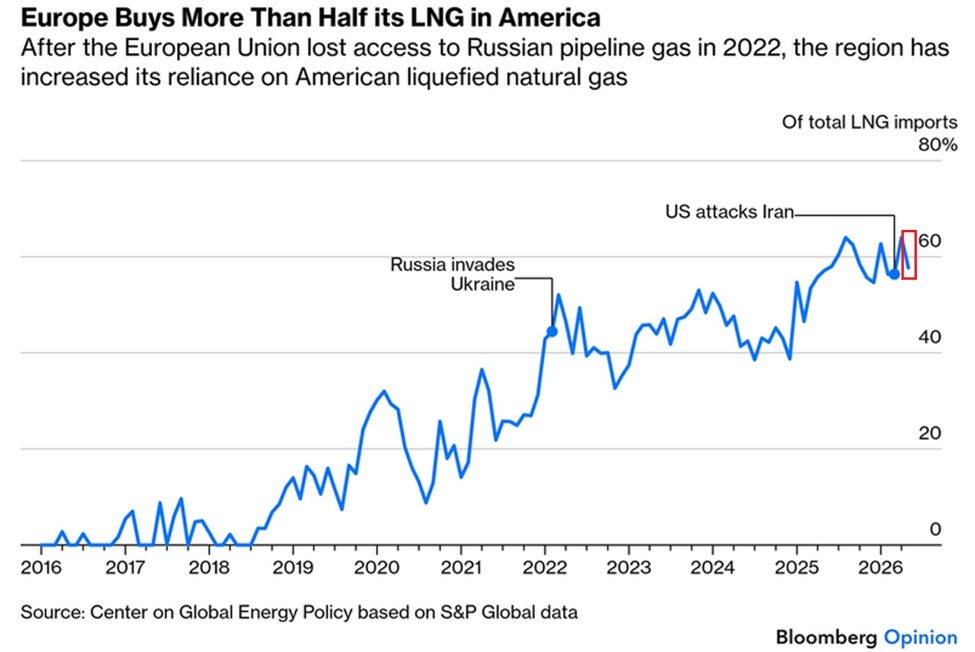

US now ~60% of Europe's LNG imports, near an all-time high:

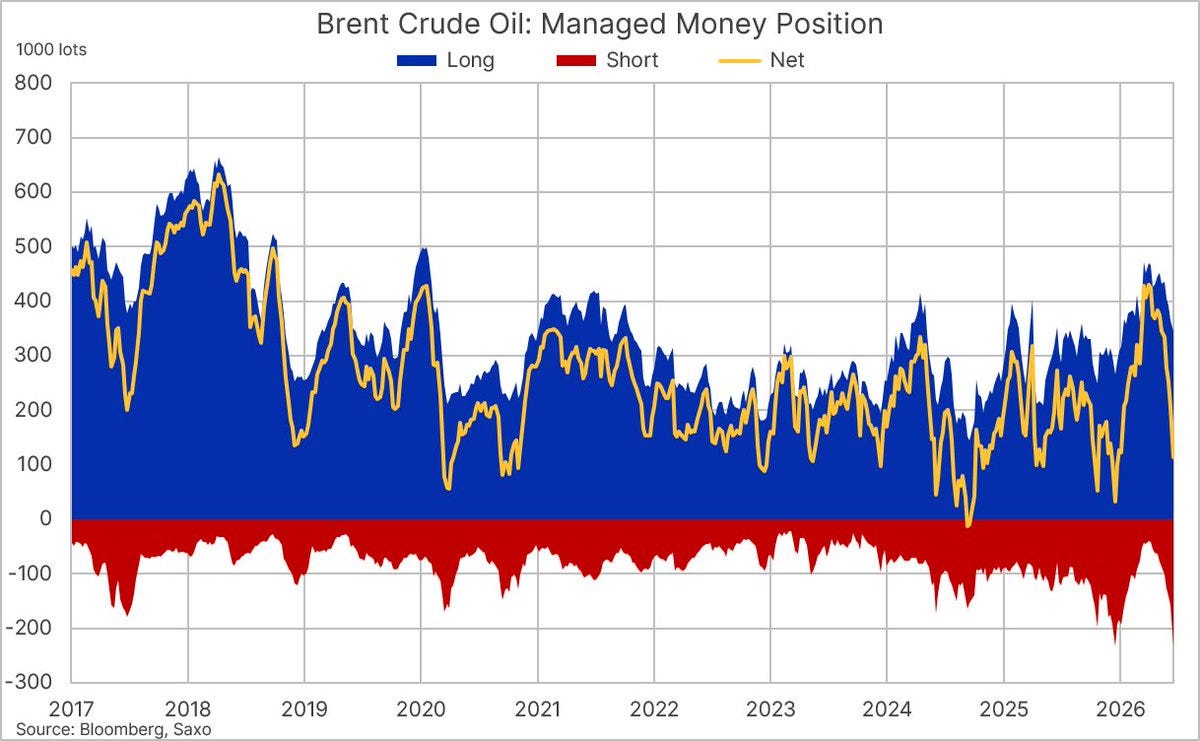

Brent managed-money net long collapses; gross shorts highest since pandemic:

Taiwan now the world's fifth-largest stock market, up 100% in a year:

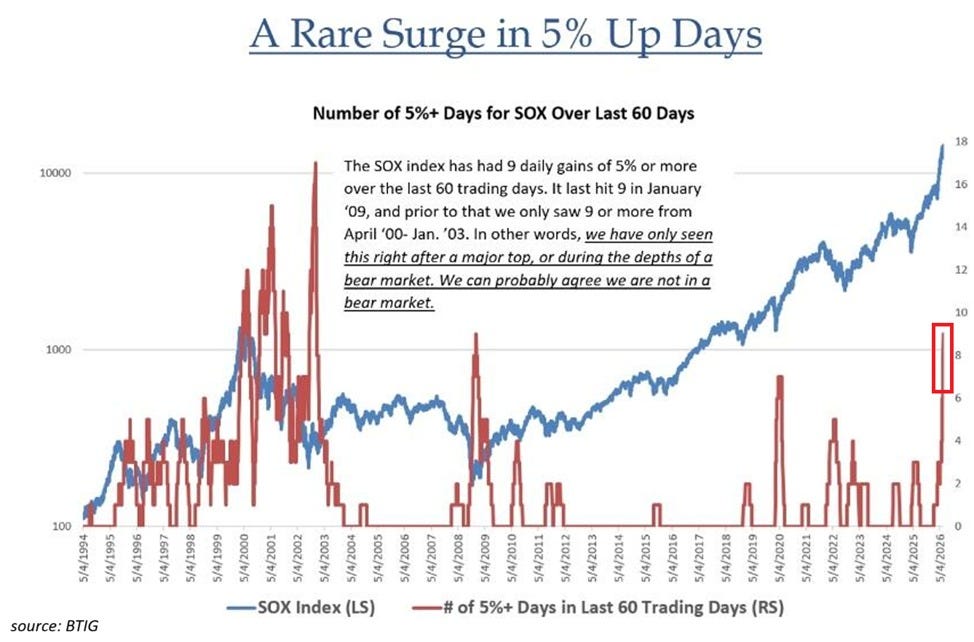

SOX 5%+ up days hit 9 in 60 sessions, last seen Jan 2009:

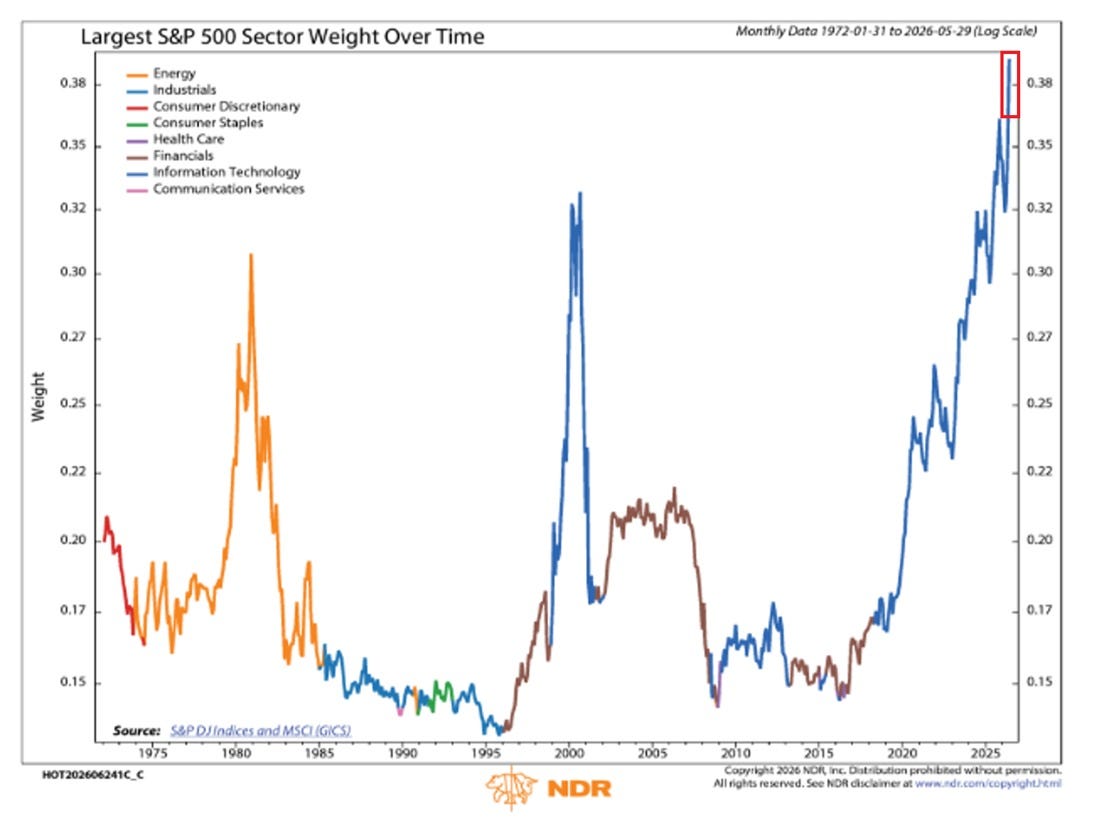

Info Tech a record 39% of S&P 500, above the Dot-Com peak:

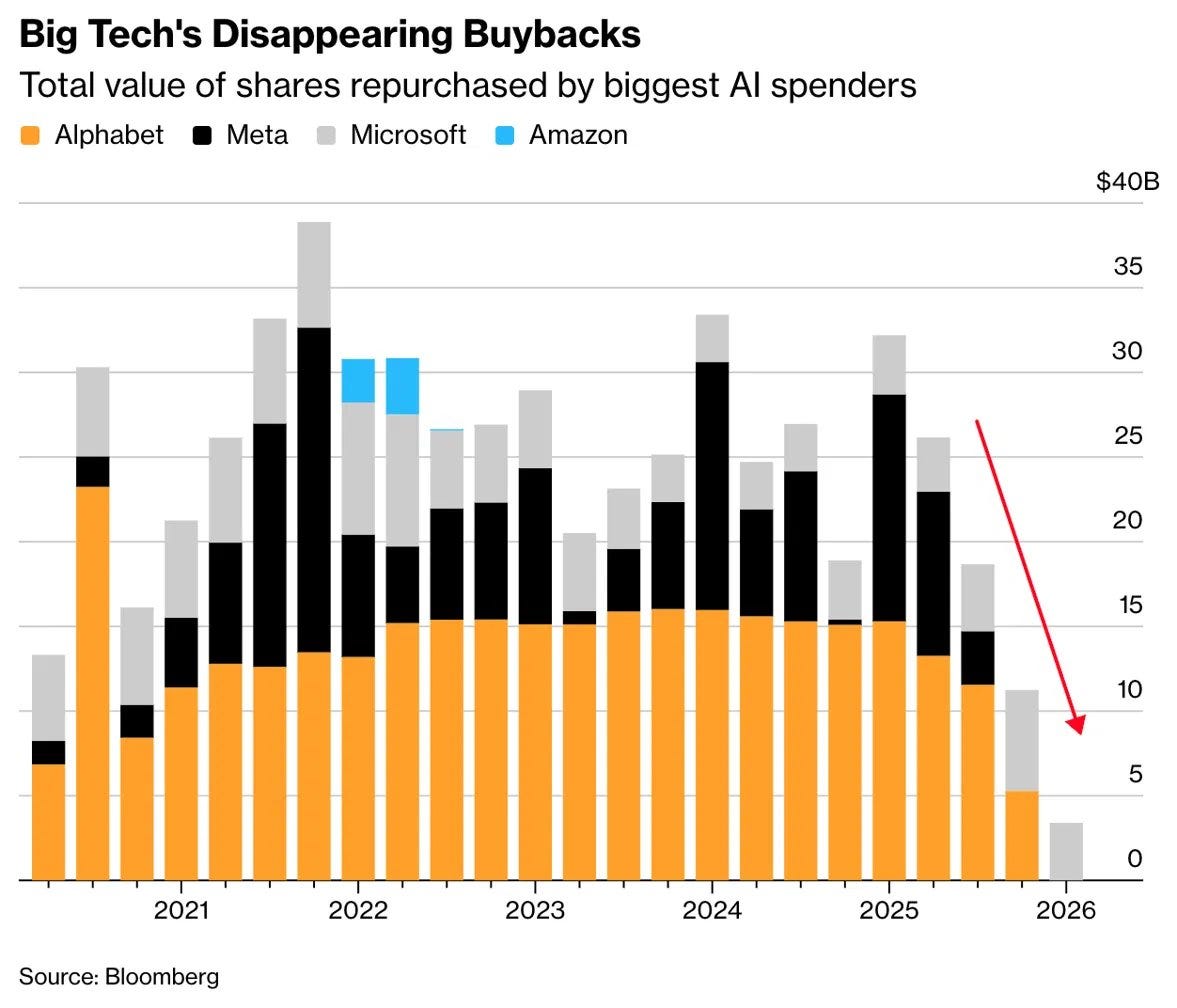

Big Tech buybacks collapsing as AI capex eats the cash:

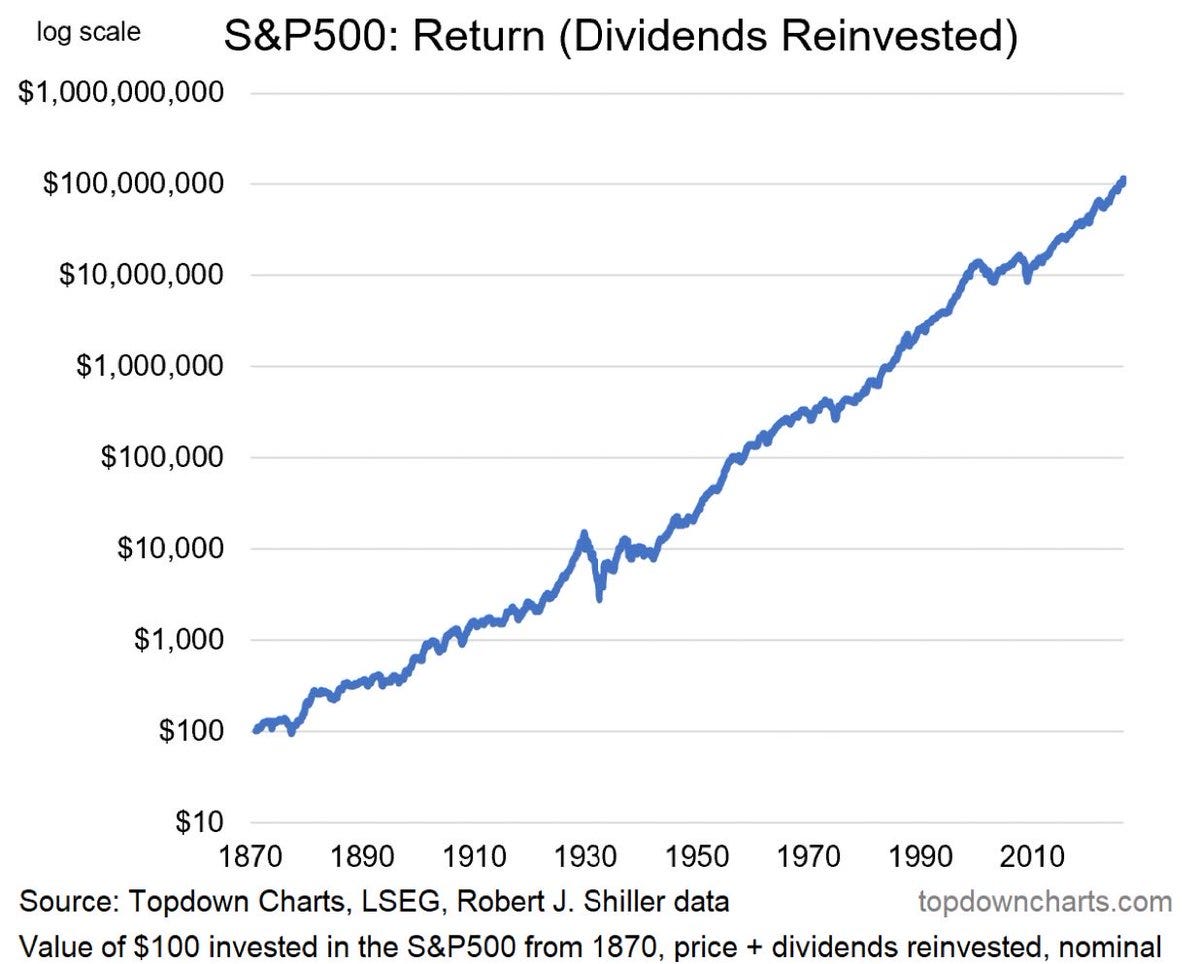

$100 in the S&P 500 since 1870 → over $100M (log scale):

Rare earth supply chain, ore to magnet — China's grip at every stage:

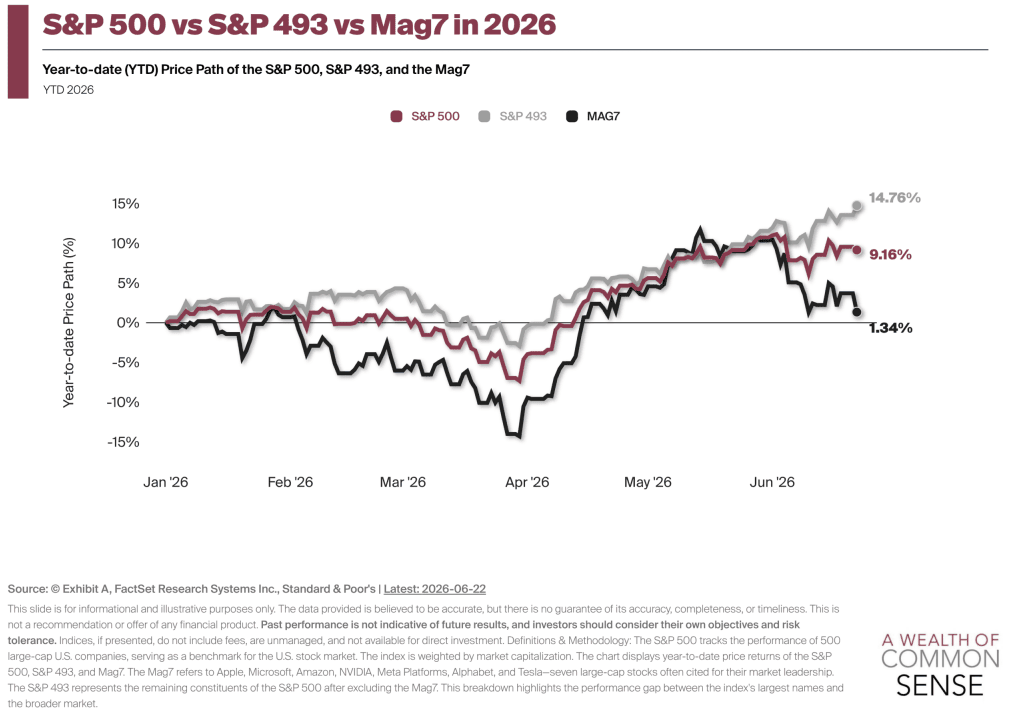

S&P 500 vs S&P 493 vs Mag 7 in 2026:

Someone’s calling Saylor:

Thanks No1...Always look forward to your posts landing.

Regarding the Chinese gold hoarding, for some context the Agnico Eagle mine in Meadowbank poured 5.1 million ounces of gold from 2010-2024.

1 metric tonne = 32150.7 troy ounces

32150.7 * 162.67 = 5.23+ million ounces.

Give or take... in one month they whoarded as much gold as a single mine operating for 14 years with men equipment diesel fuel the likes.

That says a shit tonne.

I'm a mineral exploration geologist, and so cannot effortlessly decode what's going on with the ins-and-outs of the current rapid (or rabid) central banks ingestion of already mined metallic gold. For example, China is busy vacuuming up as much as the marketable stuff as it can -- and at the same time it is producing as much as they can out of the ground (https://www.linkedin.com/pulse/reprise-stark-comparison-larry-turner-jrdsc/). In the long-run, what macroeconomic and microeconomic advantage, if any, do countries like China hope to obtain by this precious metal hording? Likewise, what advantage would North and South American countries obtain by ramping up their exploration success rate and mining production rate to level comparable to that of China?