Weekend thoughts

No penny for my thoughts

This is a weekly digest of unassociated pictures (graphs mostly) I saw during the week. Not much context is given.

For daily digests: https://no1sdailydigest.substack.com/archive

Gold parabolic trend holding for now:

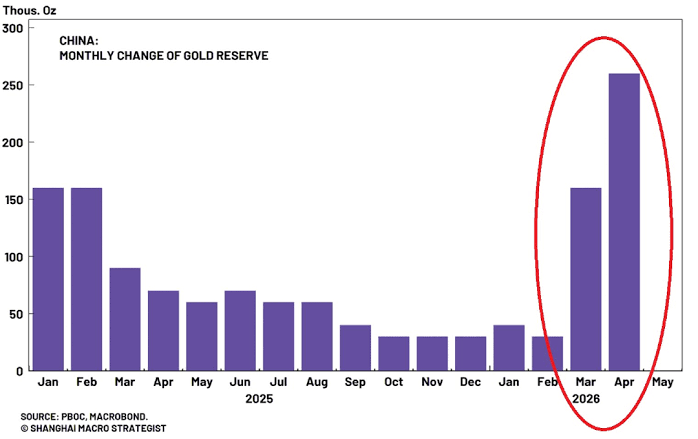

PBOC monthly gold reserve changes:

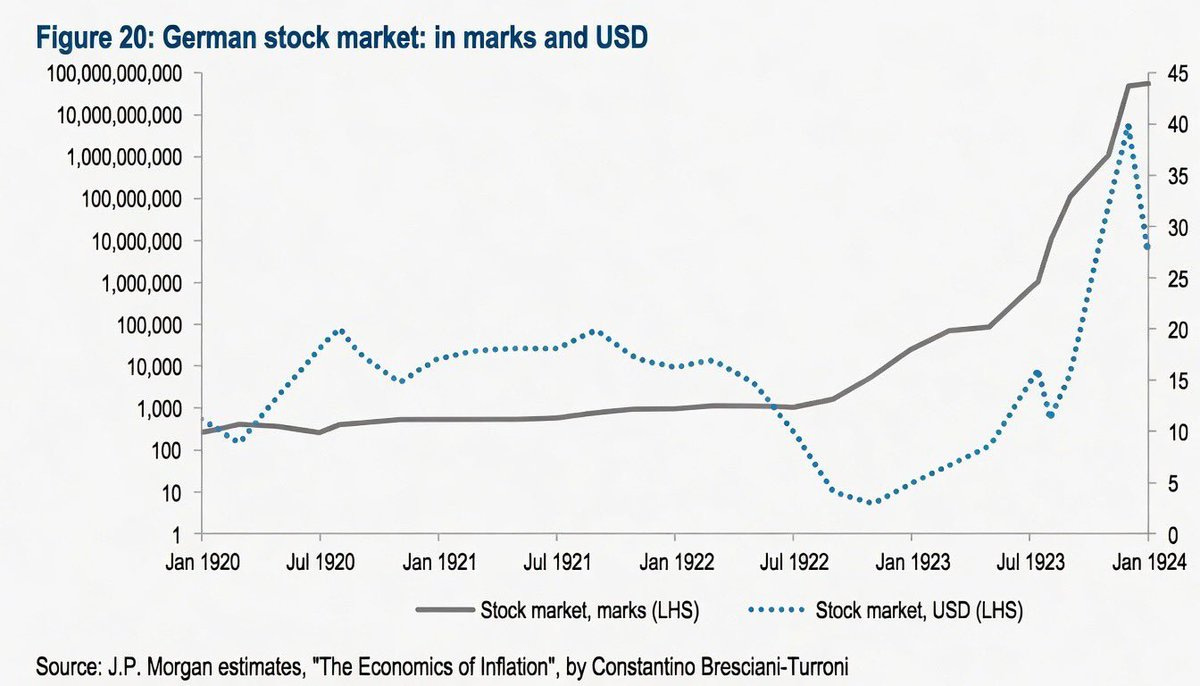

Weimar German stocks in marks vs USD, 1920–1923:

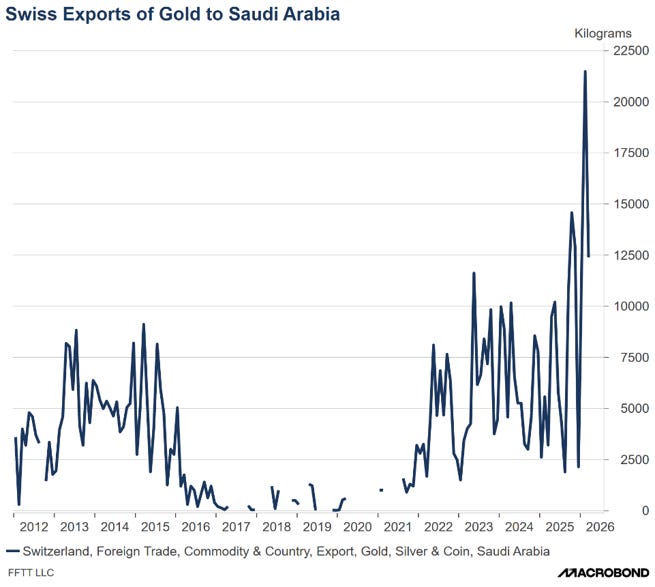

Swiss gold exports to Saudi Arabia 🚀:

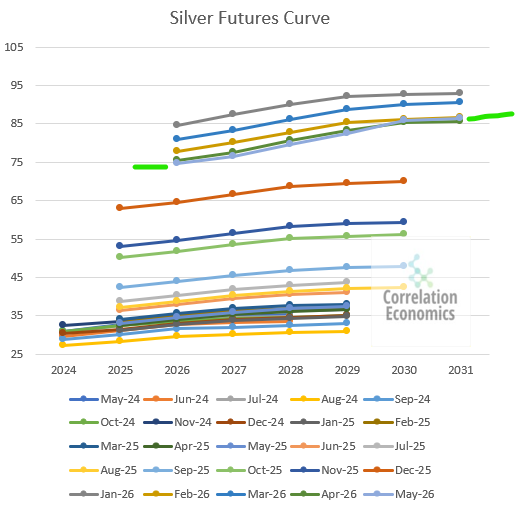

Silver futures curve: paper market perpetually underestimates reality

Silver market structure: COMEX registered, SOFR, lease rates, Shanghai basis:

Chinese gold & silver imports/exports, April 2026:

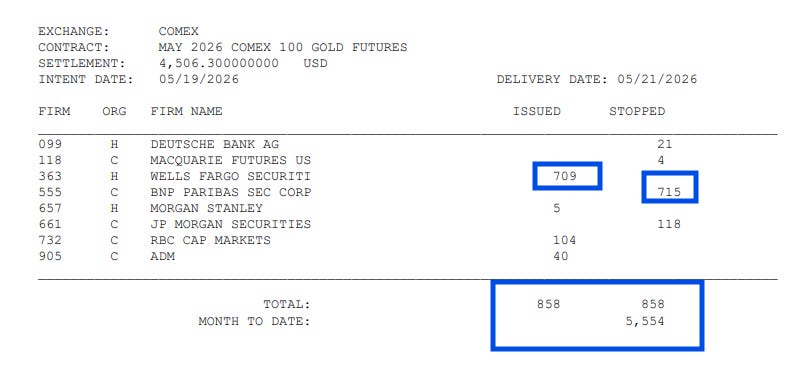

COMEX May gold deliveries: 858 notices Tuesday — 5,554 total:

Platinum ETF (PPLT) borrow fee spike — precursor to a 2025-style run?

Silver long-term charts + lots of ratios:

GDX vs. SPX monthly chart: rotation forming:

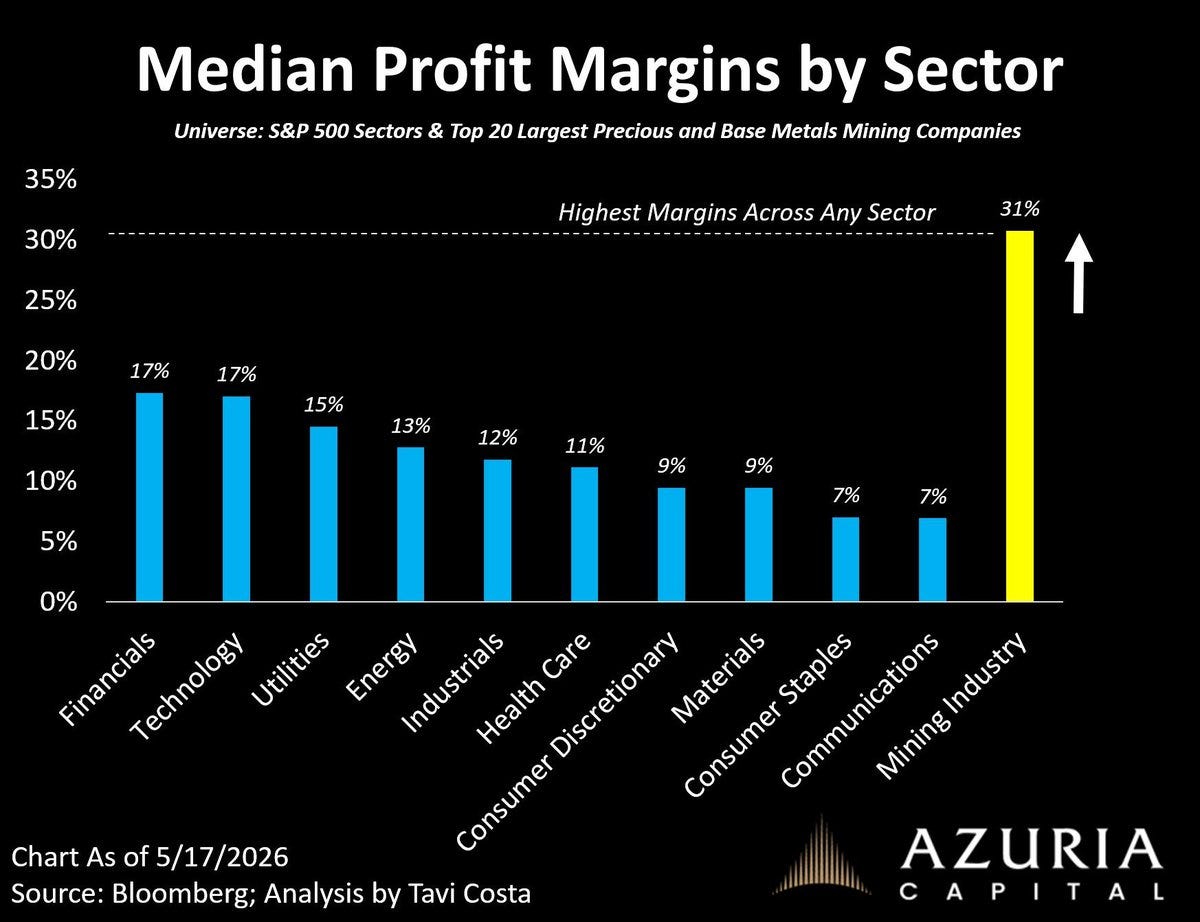

Mining sector profit margins vs S&P 500 sectors (and nobody wants to own them):

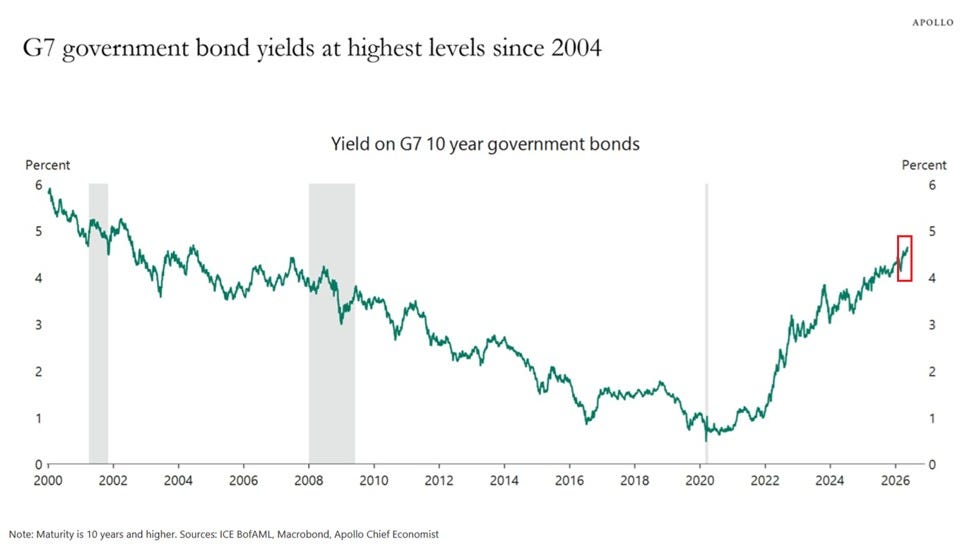

G7 10-year yields: highest since 2004:

Japan 10Y yield above 2.80%: all-time high 🚀:

US 30Y Treasury yield highest since pre-GFC:

Japan 40Y yield above 4.4%: all-time high:

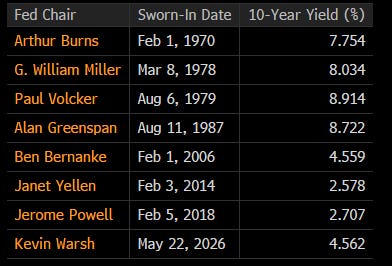

10Y yield at each Fed chair swearing-in since Burns — Warsh inherits 4.562%:

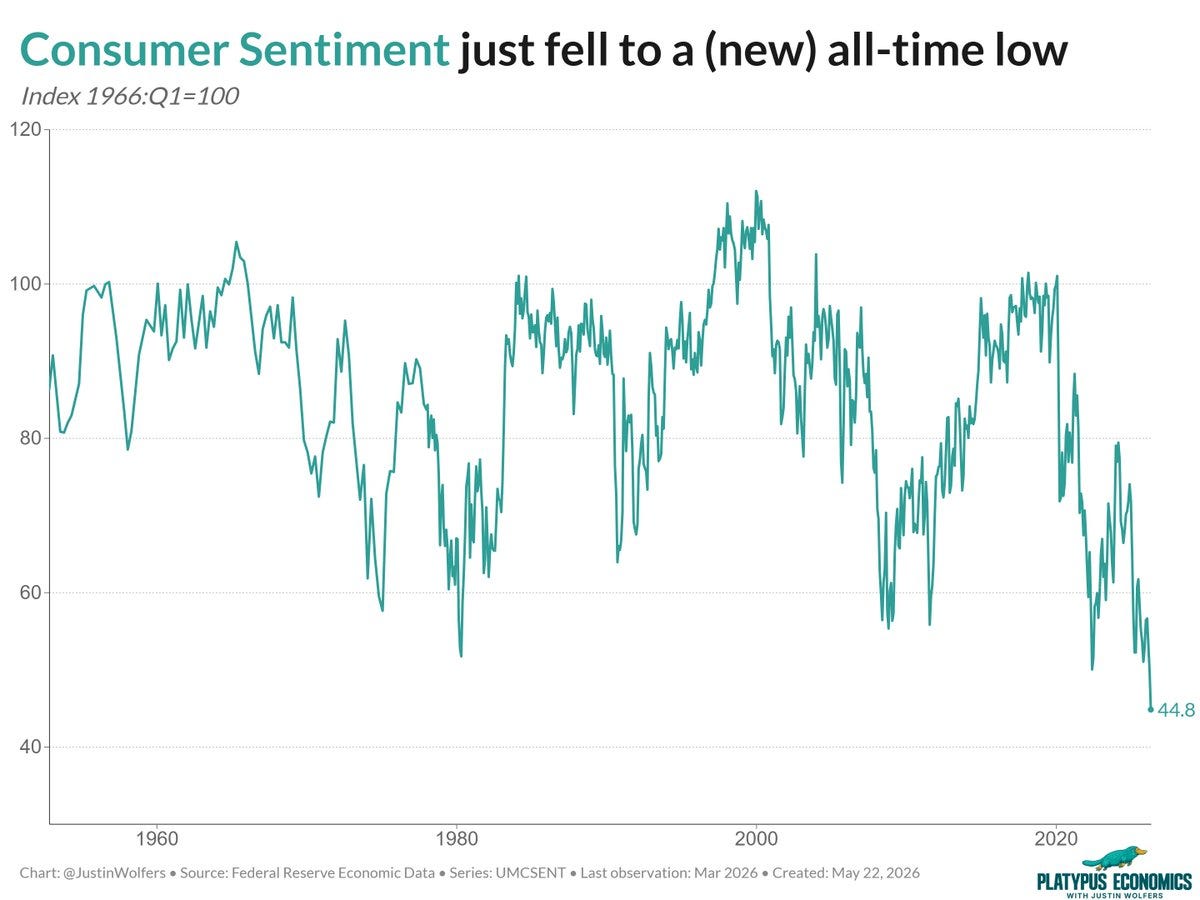

UMich consumer sentiment: 44.8, new all-time low (worse than Nov. 2008):

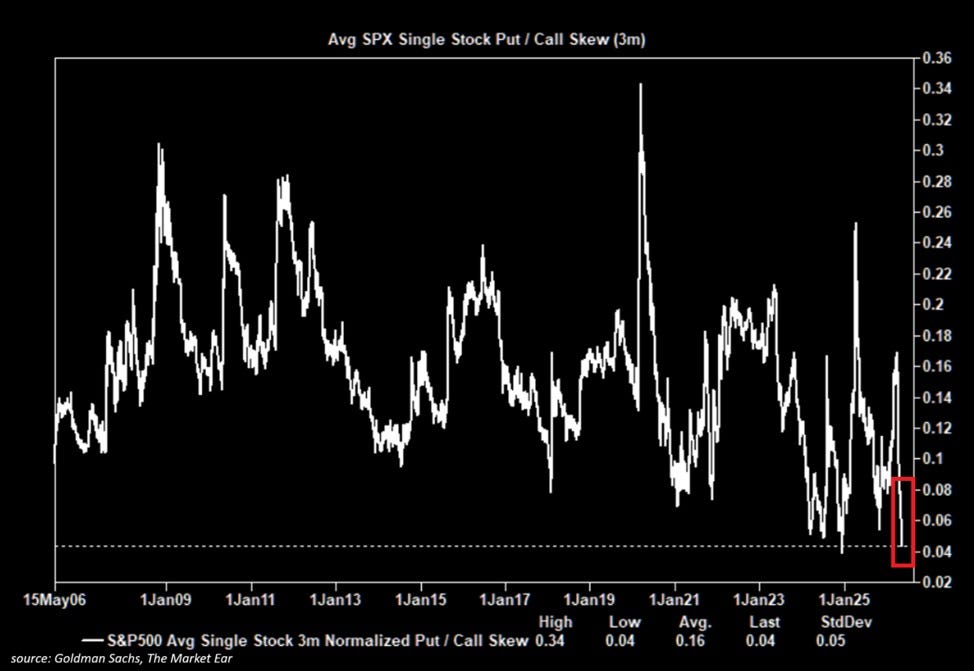

S&P 500 avg single-stock put/call skew: 0.04, 4th-lowest in 20 years:

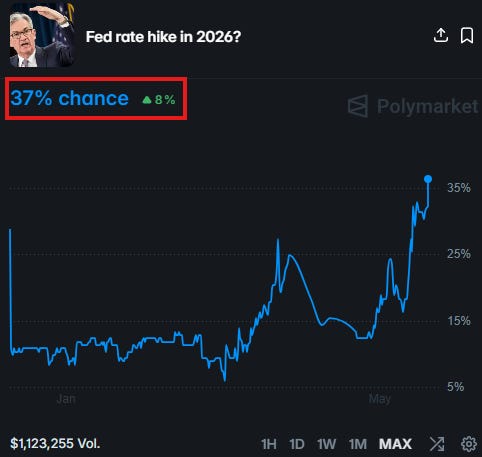

Fed rate hike odds in 2026: 37%:

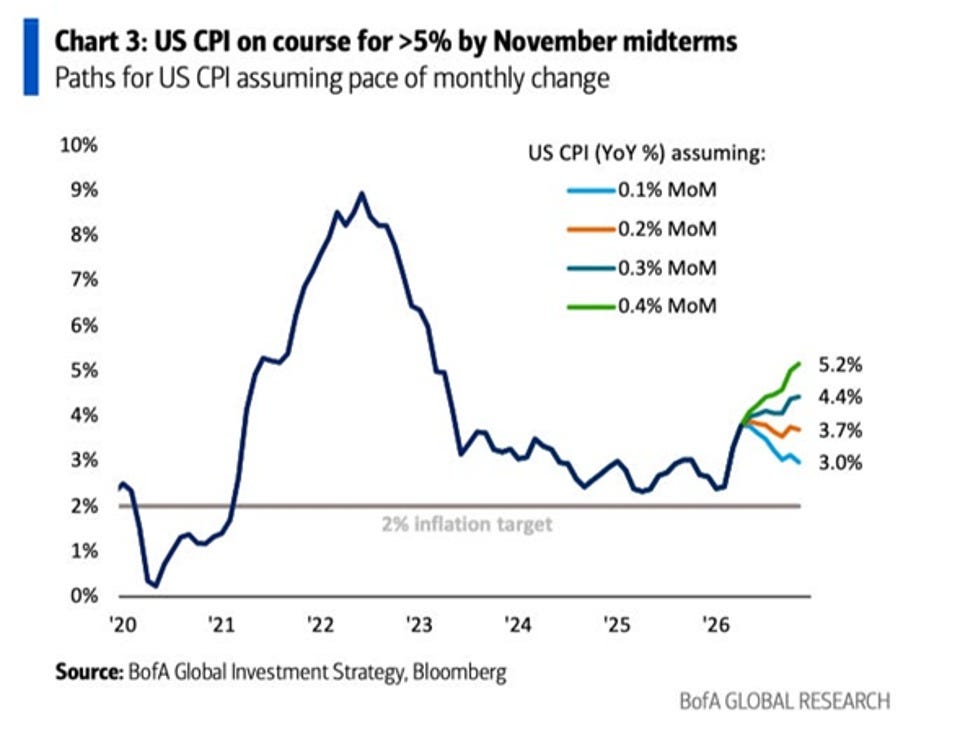

US CPI on track for >5% by November midterms:

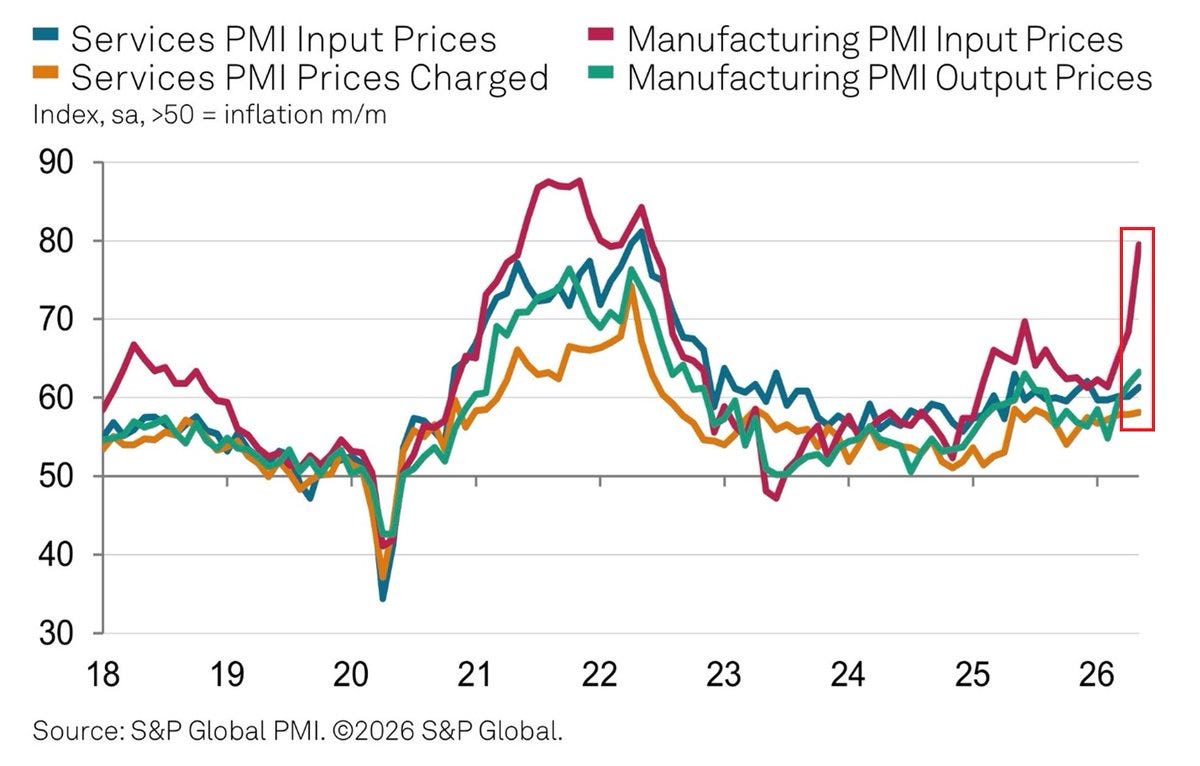

Manufacturing PMI input prices: 80, highest since mid-2022 — stagflation accelerating:

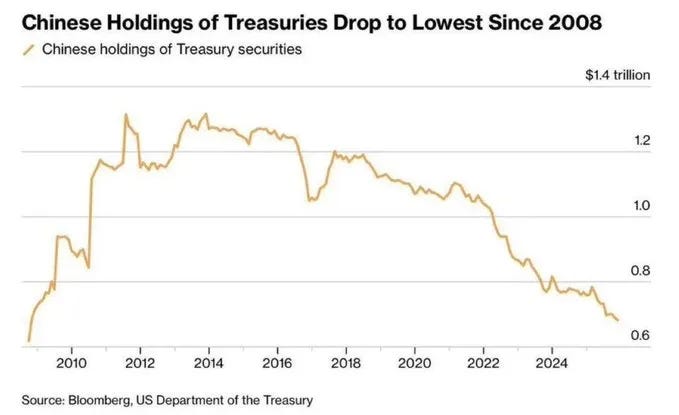

Chinese Treasury holdings: lowest since 2008:

Turkey's US Treasury holdings: dumped in first month of Iran War:

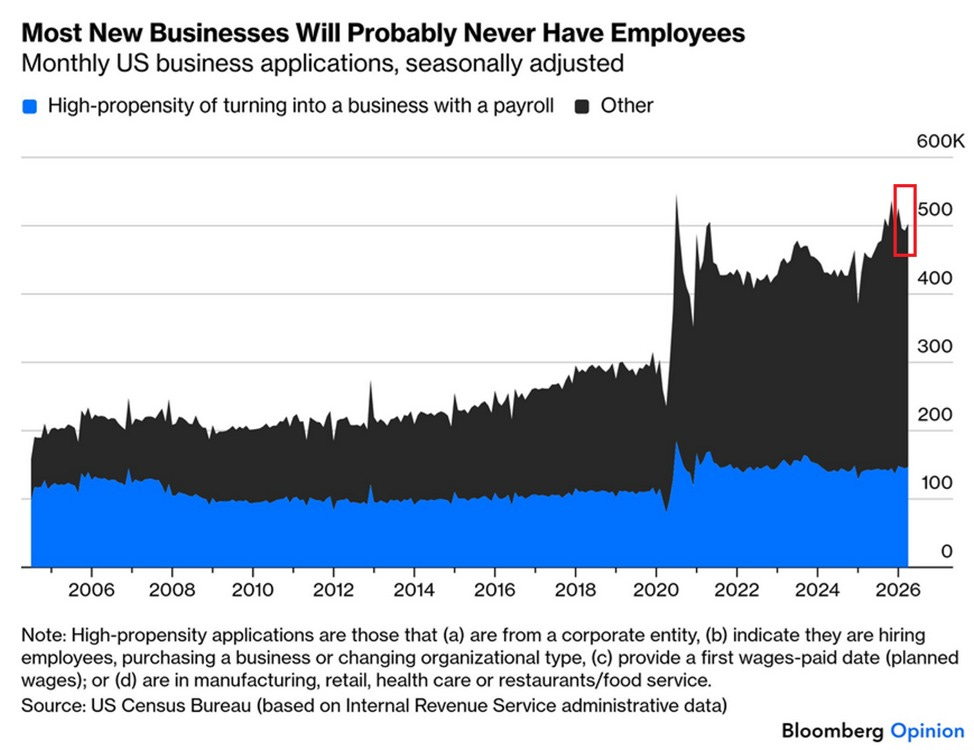

Lots of businesses, less employees so:

PCE inflation decomposition: software contribution vs historical avg, March 2026:

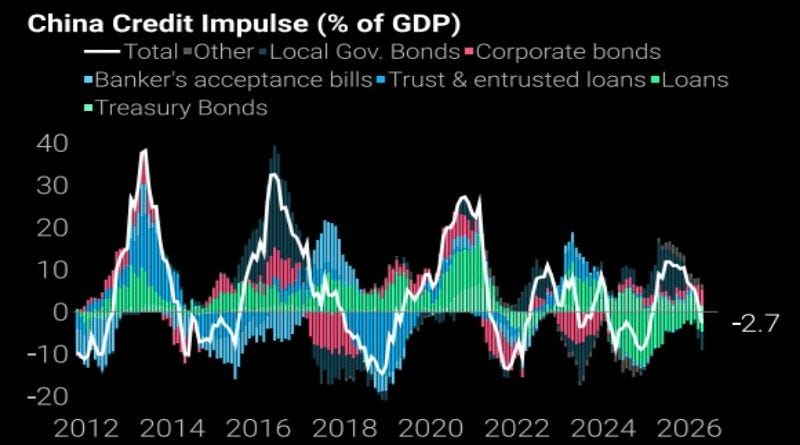

China credit impulse (% of GDP):

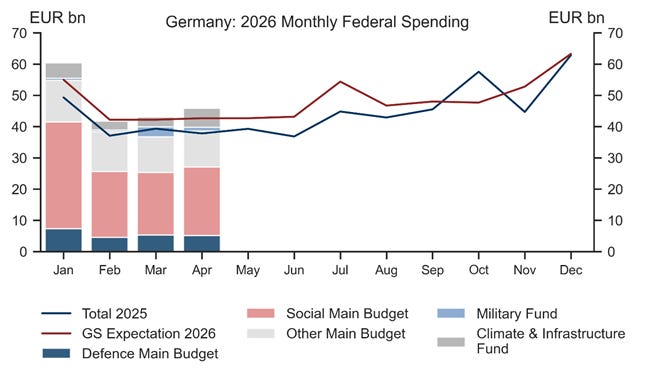

Germany 2026 monthly federal spending: defence, social, military fund:

30Y mortgage (6.75%) + US 30Y note yield (5.184%):

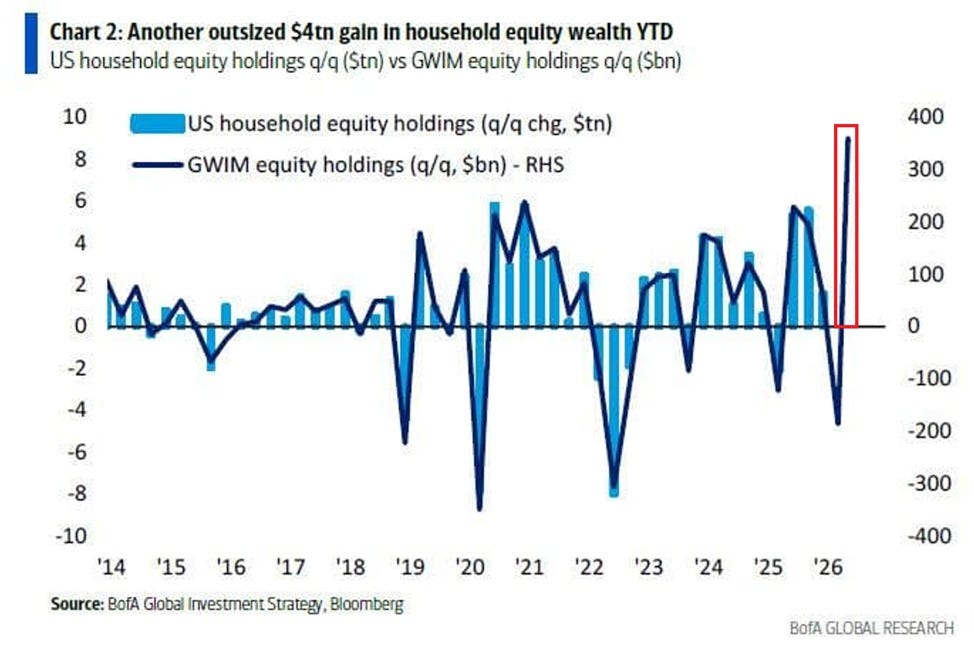

US household equity holdings: +$4T YTD, +$31T since 2023: This is going to end well…

Berkshire cash pile: $397B all-time high:

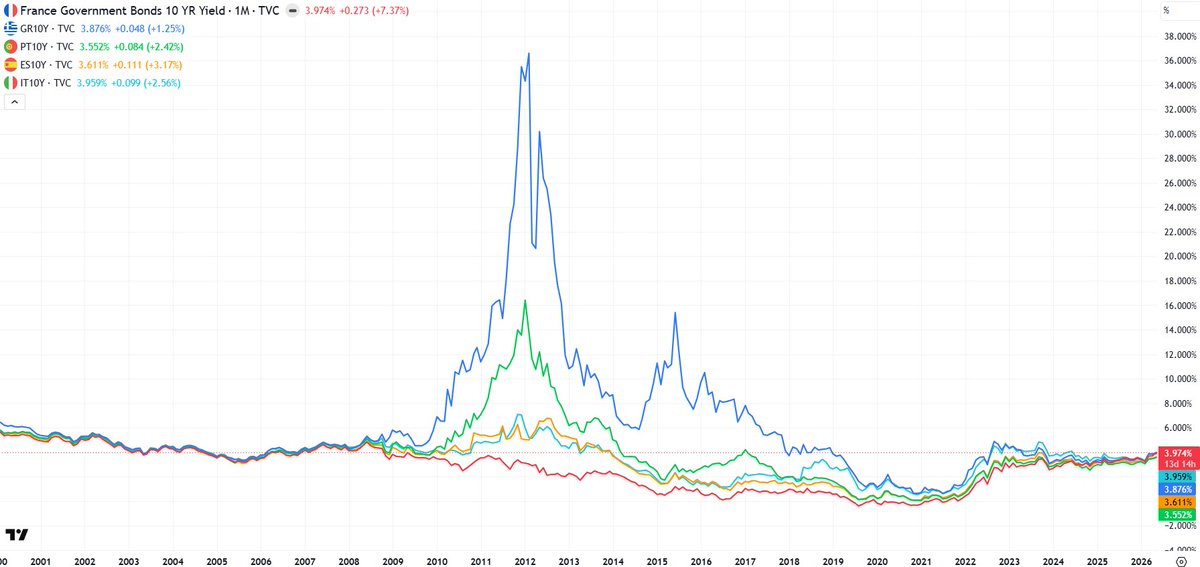

France 10Y yield now higher than Portugal, Italy, Greece, and Spain:

Treasury futures block sales:

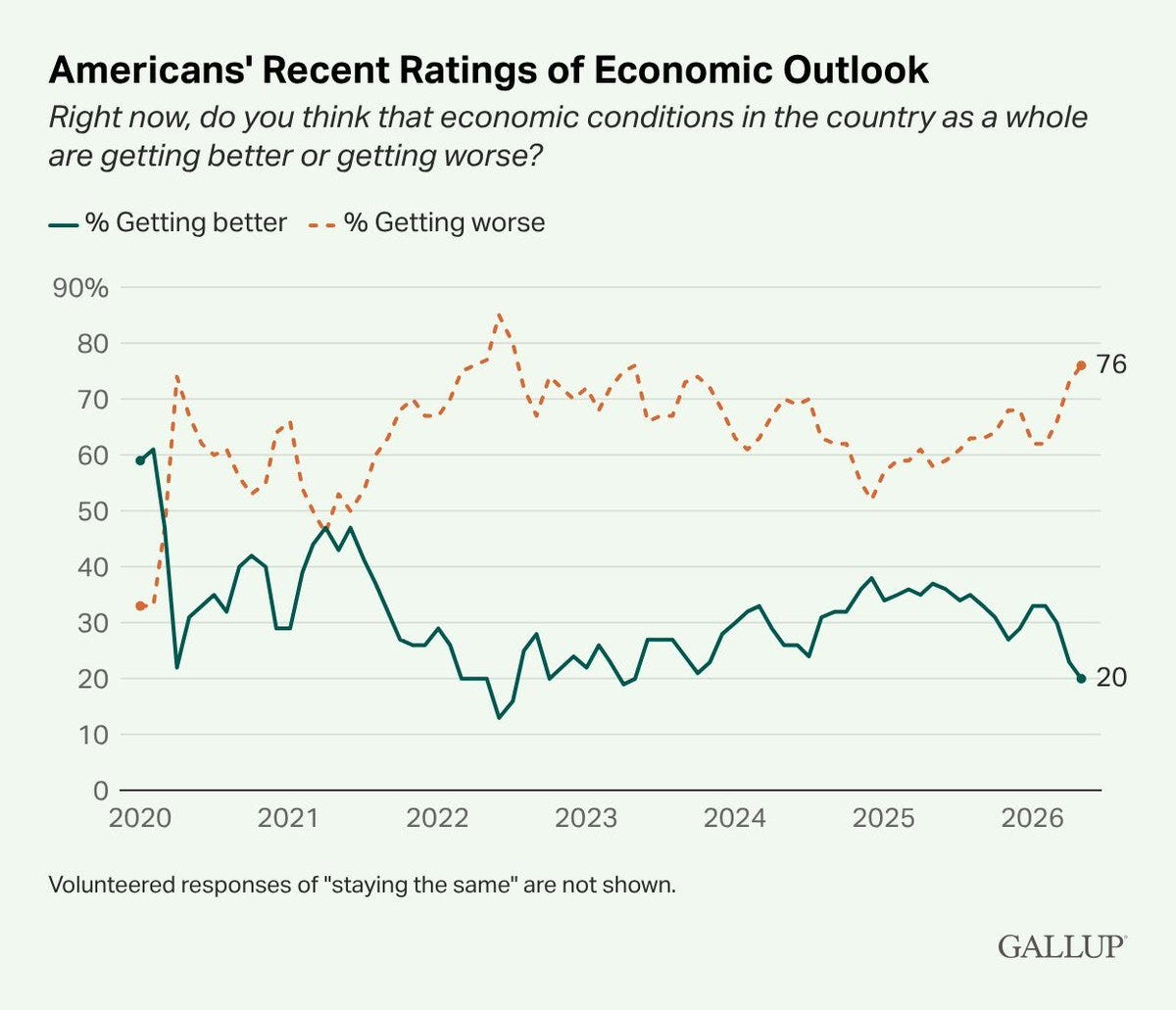

Gallup: 75% of Americans say economic conditions getting worse:

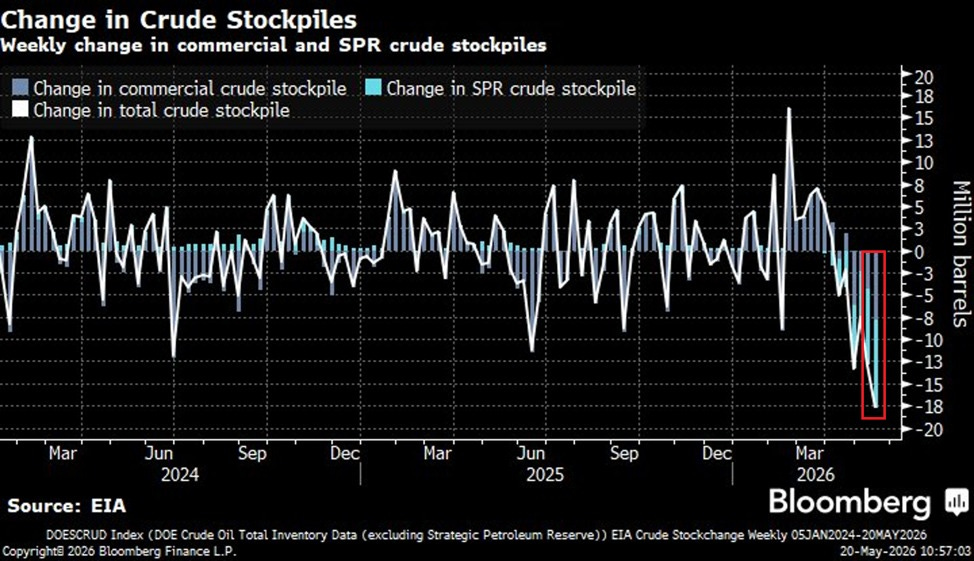

US crude inventory drawdown: -17.8M bbls/week, largest in history:

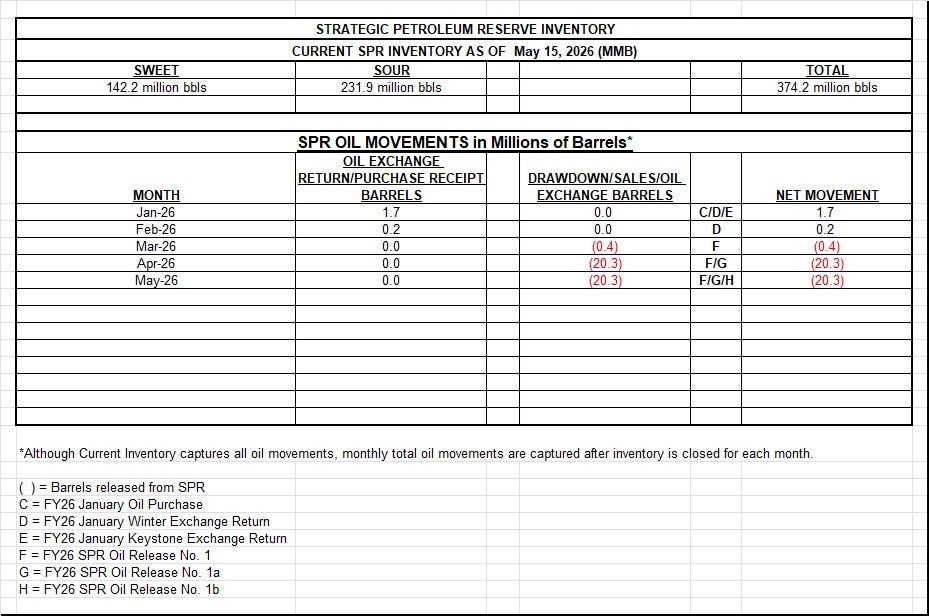

US SPR inventory: 374.2M bbls — record weekly drain of 9.9M bbls:

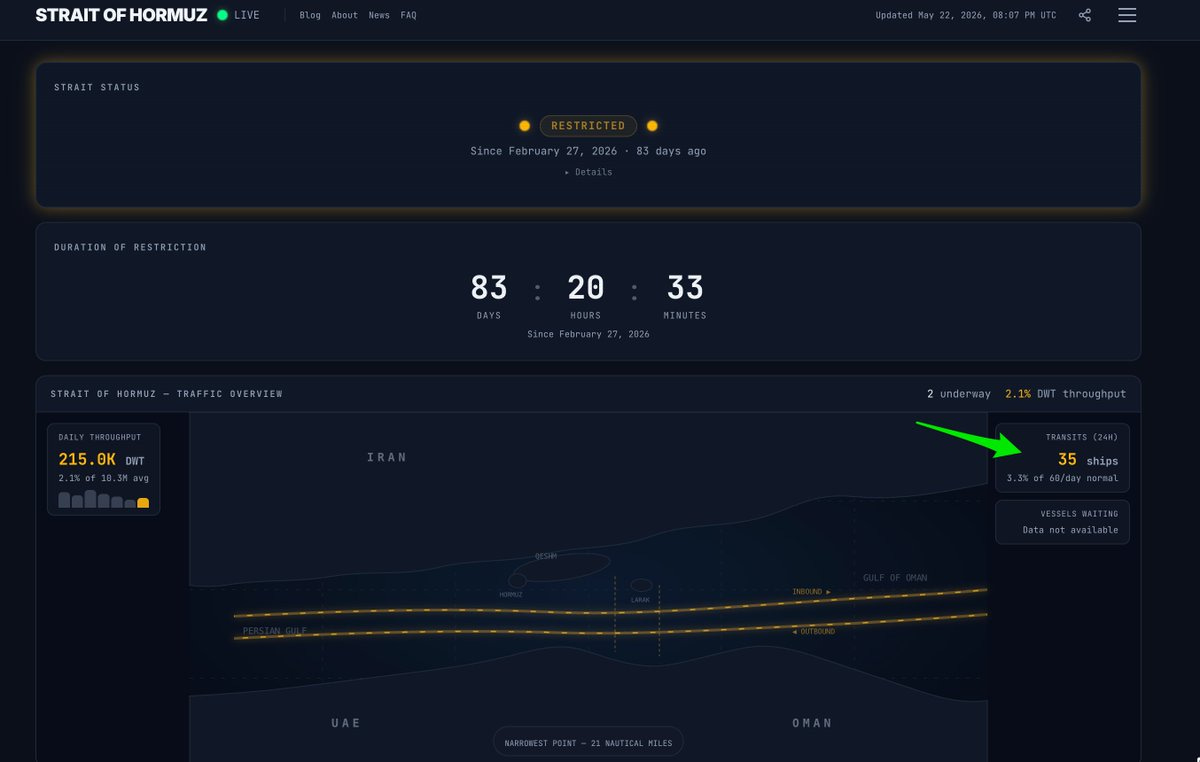

Strait of Hormuz: 83 days restricted, 31% chance open by May 31:

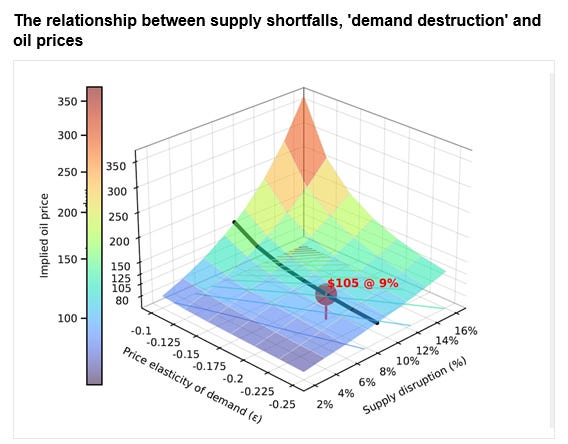

Supply shortfalls, demand destruction & implied oil prices (to $350):

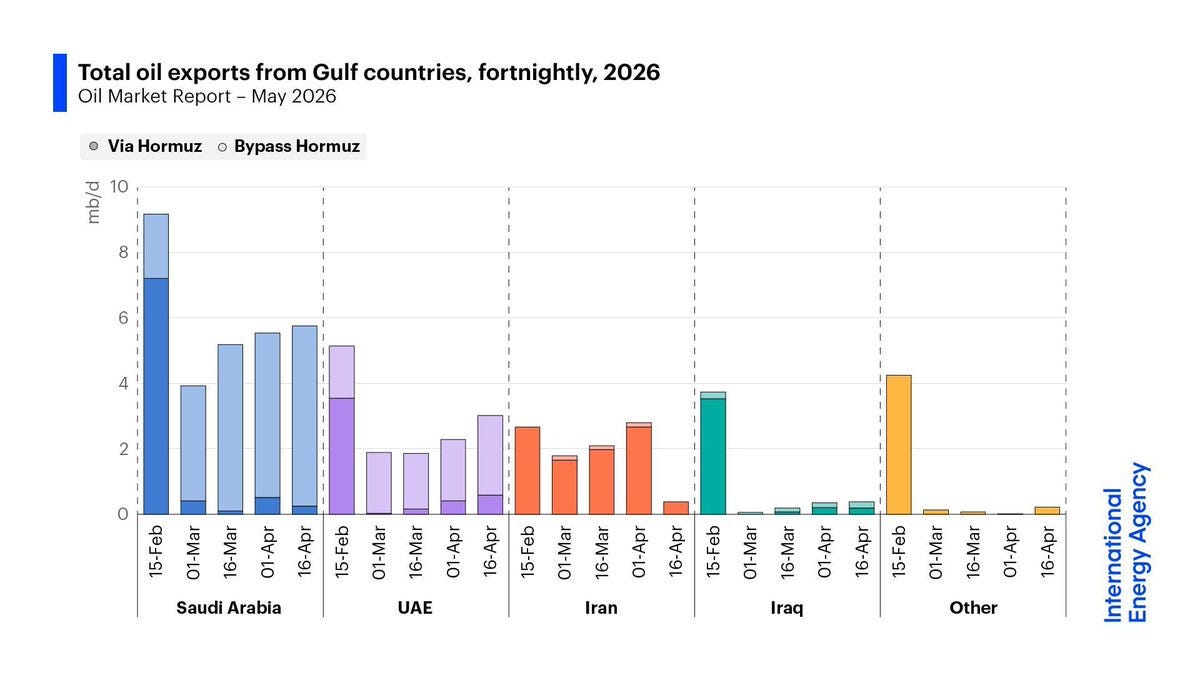

Gulf oil exports: Hormuz vs bypass routes, May 2026:

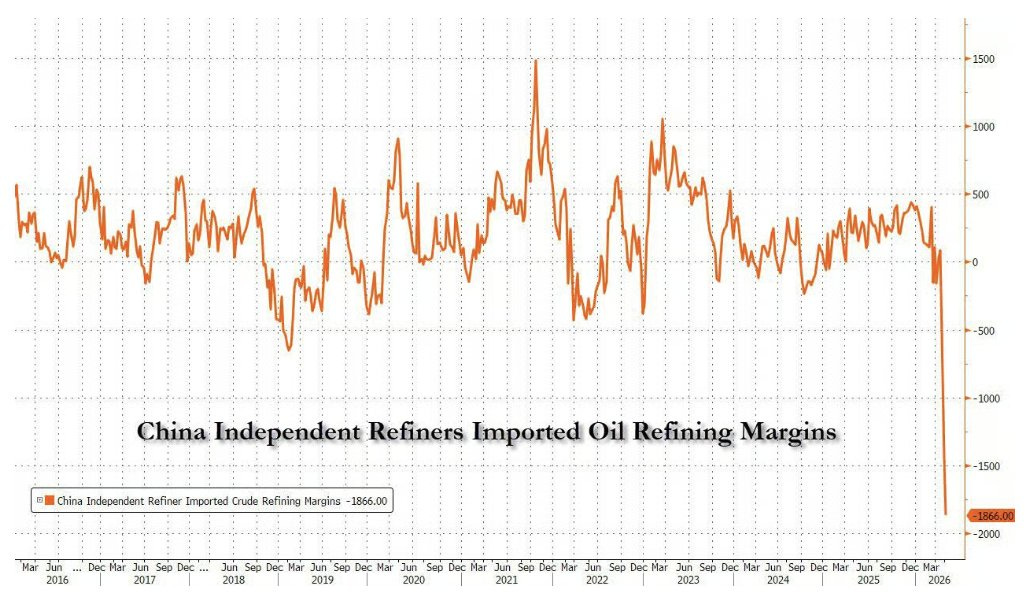

China independent refiner margins: most negative in history:

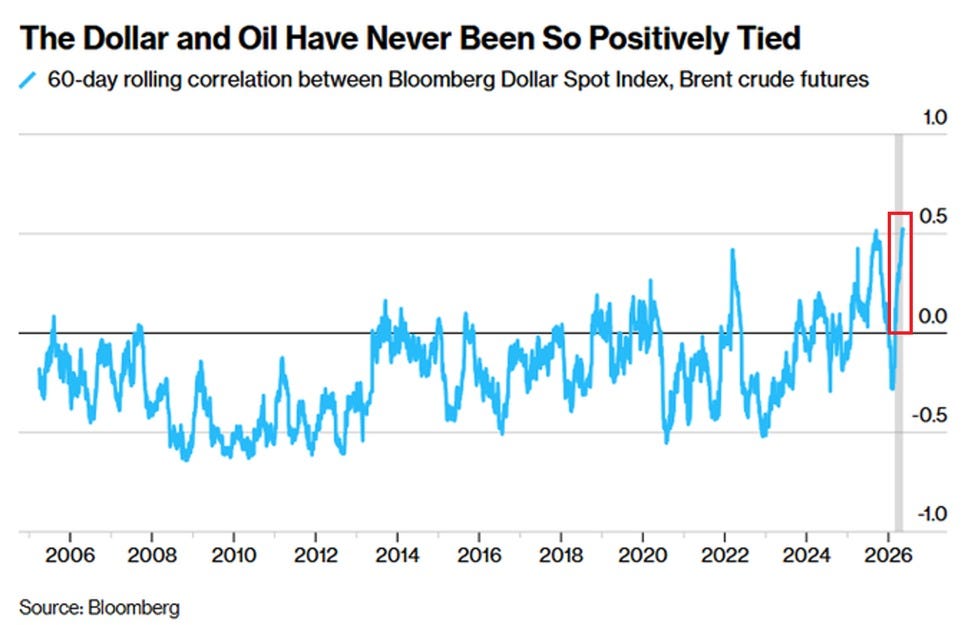

USD/Brent correlation: 0.55, highest since Bloomberg Dollar index launched in 2005:

Sulfur prices going parabolic 🚀:

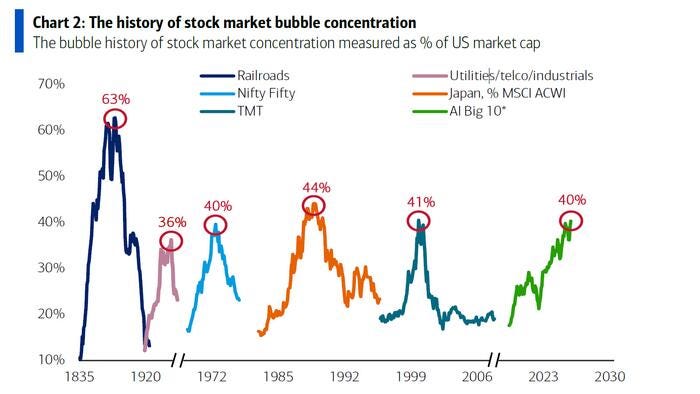

Stock market bubble concentration history: railroads → utilities → Japan → AI (60%):

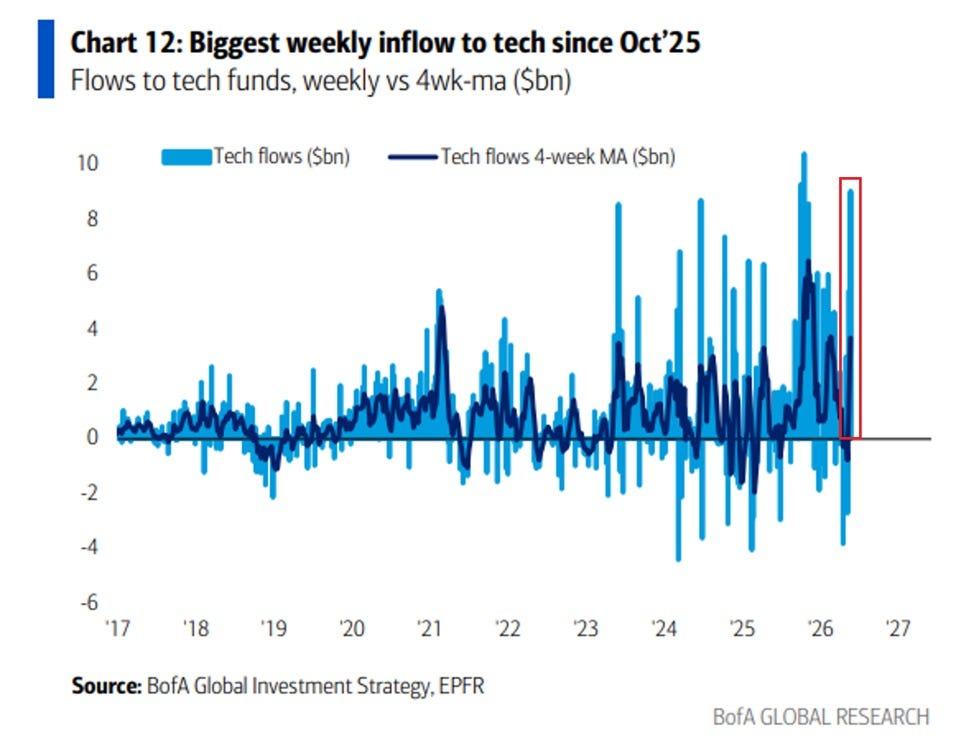

Tech fund inflows: +$9B last week, 3rd-largest weekly inflow on record:

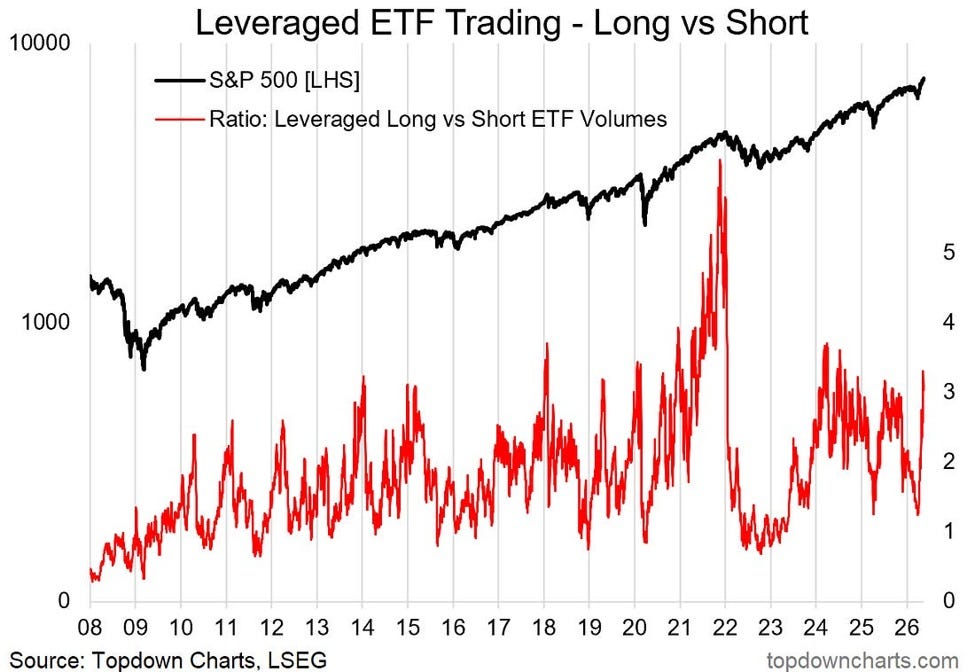

Leveraged long vs short ETF ratio: 3.3x, highest since July 2024:

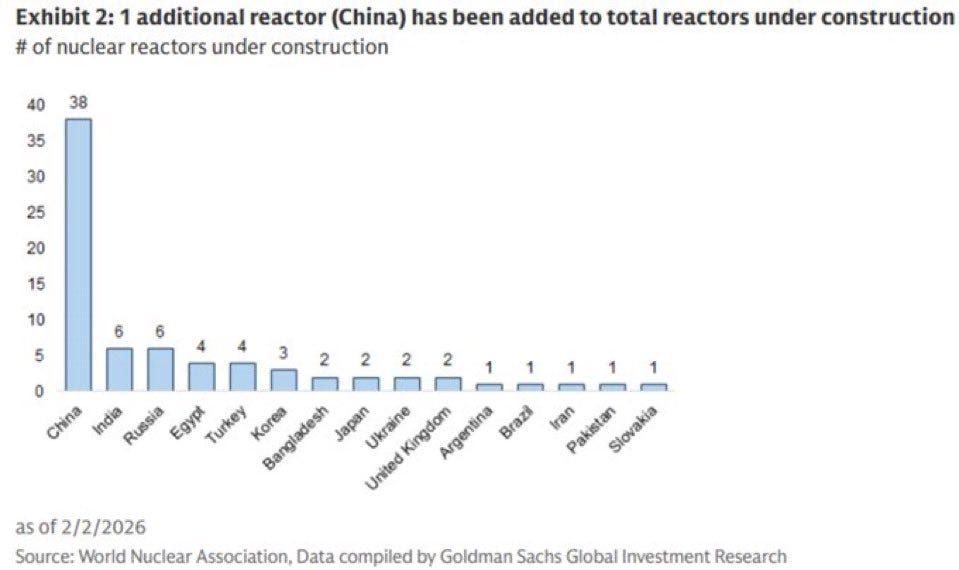

Nuclear reactors under construction: China 38, US 0:

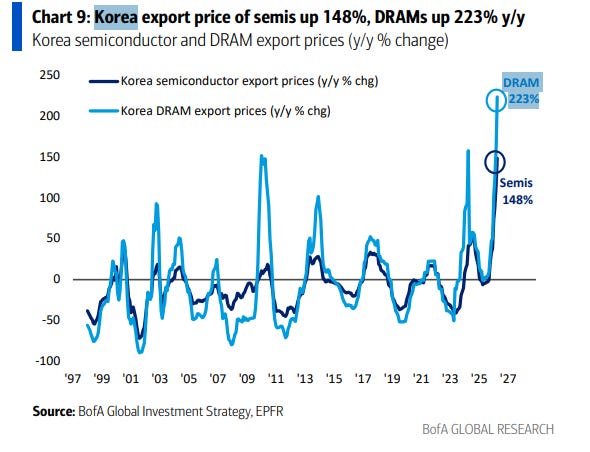

South Korea exports: +52.6% YoY (first 20 days of May), strongest on record:

Korea semiconductor export prices: +148% YoY; DRAMs +223% YoY:

Holy Crap - I got a new name for you - "number 1" -

"charthead"

~~

gracious me - is this your life - living in charts and such - I mean I like em - but jeepers that was a lot of em

Thanks No1. For anyone interested, here are my Apr PCE Inflation estimates for the data that will drop on Thu: https://arkominaresearch.substack.com/p/april-2026-pce-forecast-my-1-bp-accurate