COMEX's credibility problem is getting worse

"Nothing to see here"

Something’s wrong at COMEX. Not wrong like “oops we made a small accounting error” wrong. Wrong like “the foundation is cracking and we’re pretending everything’s fine” wrong.

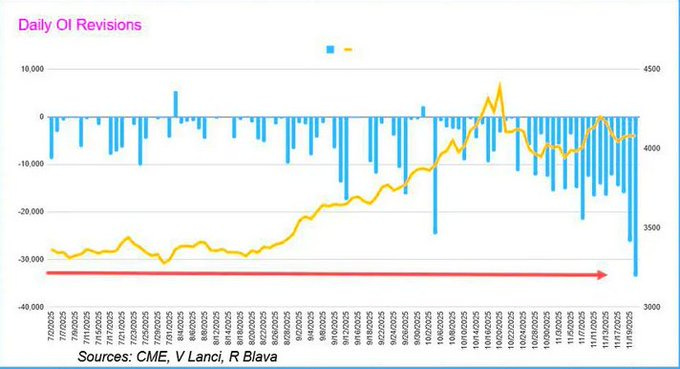

You know that feeling when someone’s lying to you and they keep changing their story slightly each time? That’s what’s happening with COMEX gold open interest data right now. The revisions keep getting bigger.

Here’s what normal looks like: COMEX reports preliminary open interest figures each day. Then they make small adjustments - maybe 200 to 300 contracts - when they finalize the data. Basic housekeeping. Rounding errors. Finding loose change in the couch cushions. But that’s not what’s been happening over the last month. We’re seeing revisions approaching 33,000 contracts. Let me put that in perspective: that’s going from loose change to discovering you “forgot” about $100 million in your other pants.

There’s a pattern too. The biggest corrections happen on Mondays. Friday trades aren’t being fully reported. Someone’s taking the weekend to figure out how to explain what happened. Or taking the weekend to figure out if they need to report it at all.

The timing is another suspicious factor. Almost too perfect. We all know that the US government decided to take an extensive holiday in October. Result? No weekly Commitment of Traders (COT) data. CFTC reports frozen at September 23. No regulatory visibility into who’s doing what. And lo and behold! Right during this all too convenient reporting blackout, open interest revisions spiked. When the cat’s away, the mice will play… When the regulator’s not watching, banks do what banks do.

If you’re like us - retail, you can’t just decide not to report your trades. Just try it and see your broker margin call you into oblivion before you can say “operational delay.”

This kind of delayed reporting requires something special. Like being a major clearing member. A big bank. Someone with institutional house accounts and the operational complexity to credibly claim “systems issues.” Only certain players can create revisions at this scale. The kind who can pick up the phone and have conversations about “timing the disclosure.”

This behavior signals concealing significant trading losses, operational or capital stress, obfuscating trade direction, or delaying compliance reporting to buy time. Pick your favorite. None are good.

Want to know if something’s cracked? Watch where the problems show up first. The LBMA shifted from T+1 settlement to T+8 weeks. Eight weeks.

They’re blaming “shortage of manpower and trucks.”

Right.

The supposed pinnacle of professional gold trading suddenly can’t find trucks for two months.

The physical market is screaming. COMEX can’t rebuild inventory. London’s settlement times blew out. COMEX data revisions keep growing.

These aren’t three problems.

It’s one problem in three places.

For years, gold has operated on a simple premise: paper dominates physical. Approximately 109 ounces of paper gold trade for every ounce of physical on COMEX. The tail wags the dog. Works great until someone asks for delivery.

October 2025 saw massive delivery demand. Biggest October on record. October is supposed to be a minor month where almost nobody takes physical. Except this year they did. And when physical deliveries spike while 1.5-2 million ounces of registered gold supports 50-65 million ounces of open interest, you get strain. Delays. “Revision patterns.” Monday morning meetings where someone explains why Friday’s numbers don’t work anymore.

Markets run on trust. The cold, hard “I believe you’ll deliver what you promised” kind. COMEX built that trust over decades. You buy a contract, you can take delivery. The metal’s there. That’s why COMEX gold sets the global price.

But trust is like a bridge. Handles a lot of weight until it doesn’t.

These revisions undermine COMEX data reliability. If Monday’s number consistently differs from Friday’s by amounts that keep growing, what does that do to price discovery? Risk management?

When your data integrity becomes a rolling question mark, you’re not the world’s price-setting mechanism anymore. You’re just another venue with credibility problems.

Gold bugs care. Of course we do. However, why should everyone else?

Gold is the embarrassing truth-teller about fiat currencies. When gold goes up, it says your money printing isn’t working. When gold goes up a lot, it says your money printing is failing catastrophically. Central banks know this. They’ve known it for decades. There’s documented evidence that since 2018, central bank Financial Stability Desks have followed BIS instructions to manage gold market perception through derivatives trading.

But suppression only works if the derivatives market maintains credibility. If participants start doubting COMEX data integrity, they’ll price in uncertainty premiums.

Or they’ll go elsewhere.

Shanghai’s waiting.

Hong Kong too.

They’d love to take over gold price discovery from New York. Once that shift happens, it won’t reverse. Just ask London about its role in oil pricing after NYMEX took over. Just ask the London Metal Exchange about nickel after March 2022.

Leadership isn’t guaranteed. It’s earned. Daily. And COMEX is stumbling.

COMEX open interest has been declining to levels not seen in years while gold keeps rallying. That’s abnormal. When price rises with falling open interest over extended periods, it suggests the dominant players - the bank swap desks that normally short - are covering, not adding. They’re backing away. This means that the usual mechanisms aren’t working. Bank swap desk shorts historically dominated, but what’s happening now is different.

And nobody’s talking about these revisions. No CME press releases. No CFTC statements about enhanced monitoring. Just silence. The silence itself is screaming louder than any information they could put out.

So where does this go?

Best case: some clearing bank screwed up reporting during the shutdown. Gets sorted. Revisions stop. Life goes on. Probability? Not very high.

Middle case: (more likely) Some clearing members took losses they couldn’t immediately report without triggering margin calls or scrutiny. They’re managing the unwinding very carefully. The system let them handle it but overall confidence takes a hit.

Worst case: (as I’m expecting) physical delivery pressure exposed some structural problems in the COMEX operations when people wanted their metal instead of some cash settlement. The clearing members doing revisions are managing a slow-motion squeeze, trying to avoid a violent unwind that breaks price discovery.

What we’re looking at, is strain. Stress. Maybe a crisis?

“We’ll get you metal eventually, probably.”

COMEX is on the same path.

These data revisions are the first reported, visible crack.

The foundation is breaking. How long until someone acknowledges it?

And what happens to gold when they do?

1st Jan 2026. Gold 4,5 k. Silver 75.

2026 yields 40% as a conservative estimation. There will be room for daily traders to play their game, with ups and downs allover the year. The good news is that the commercial banks are going full into stable coins, at least here in Europe, and I assume in the US too. This was inevitable if you think about it. It's their only way to prevent capitals from investing in commodities. They see a fiat dollar linked to crypto, stable coins, tokens and AI, so there will be Ponzi gains there, but with a multiplied volatility factor. This is going to be as a poker game, where the players try to bluff each other from the let go. But this is maybe the reason gold will not be totally supressed, with 40 - 50 % yields being allowed for the next I would say 5 - 7 years. Make your calculations. That is Gold 15 k by 2030.

You're way too good for some idiot to nitpick, but wolves howl and lions roar. For a general rule for the general public: The sure sign of an idiot is that he's a nitpicker. I hope I'm not a nitpicker, but you're rather good at figurative language and this was an exception that I couldn't bring myself to ignore. Am I an idiot too ?